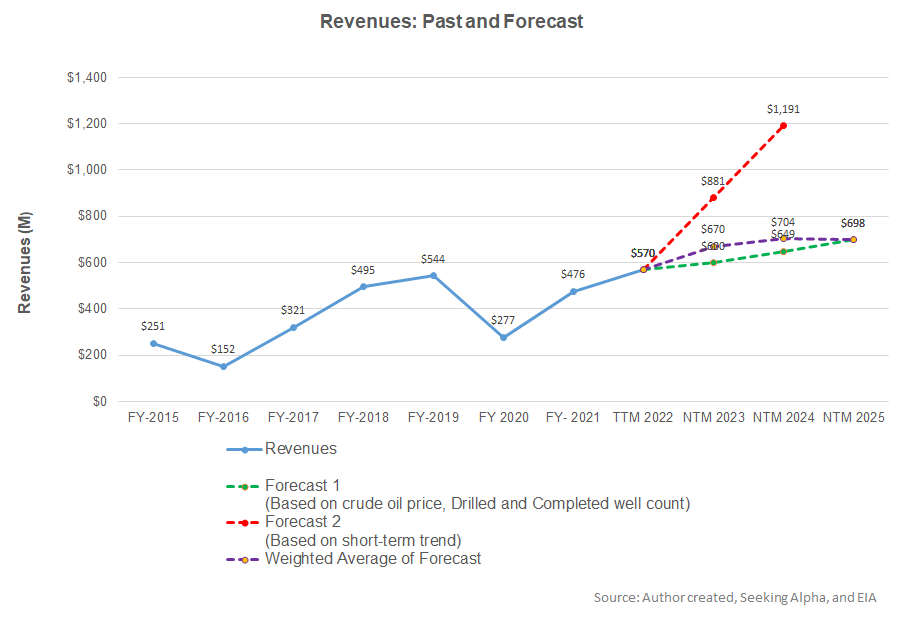

- The linear regression model suggests steady revenue growth in NTM 2023, but the rate can decelerate in NTM 2024 and NTM 2025

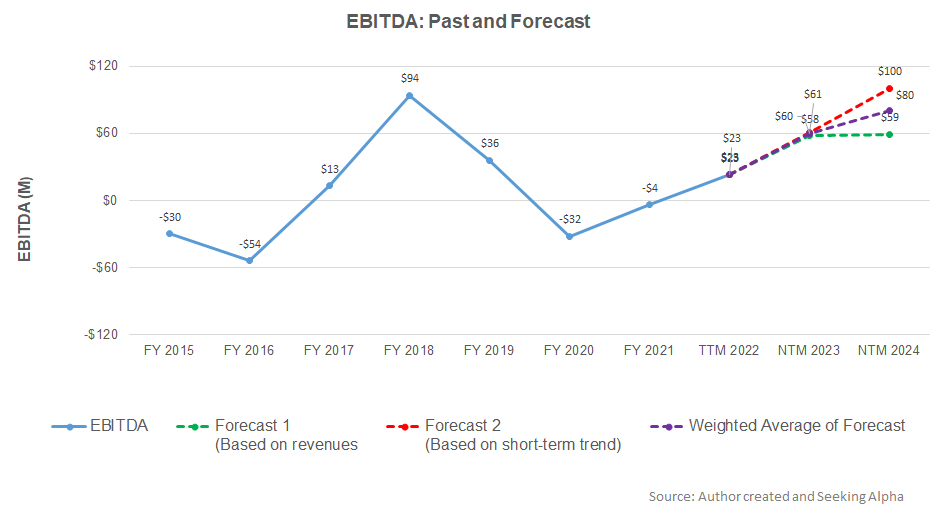

- EBITDA growth rate can fall in NTM 2024 after a steep hike in NTM 2023

- The model suggests wide variability in the expected returns.

Part 1 of this article discussed the KLX Energy Services’ (KLXE) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Revenue Forecast

Based on a regression equation between the key industry indicators (crude oil price, and the US drilled well count and completed well count) and KLXE’s reported revenues for the past seven years and the previous four quarters, we expect its revenues to increase by 18% in the next 12 months (or NTM) in 2023. The growth rate can decelerate in NTM 2024 and decline in NTM 2025.

Based on the same regression models and the forecast revenues, we expect the company’s EBITDA to more than double in NTM 2023. The EBITDA growth rate can subdue in NTM 2024.

Target Price

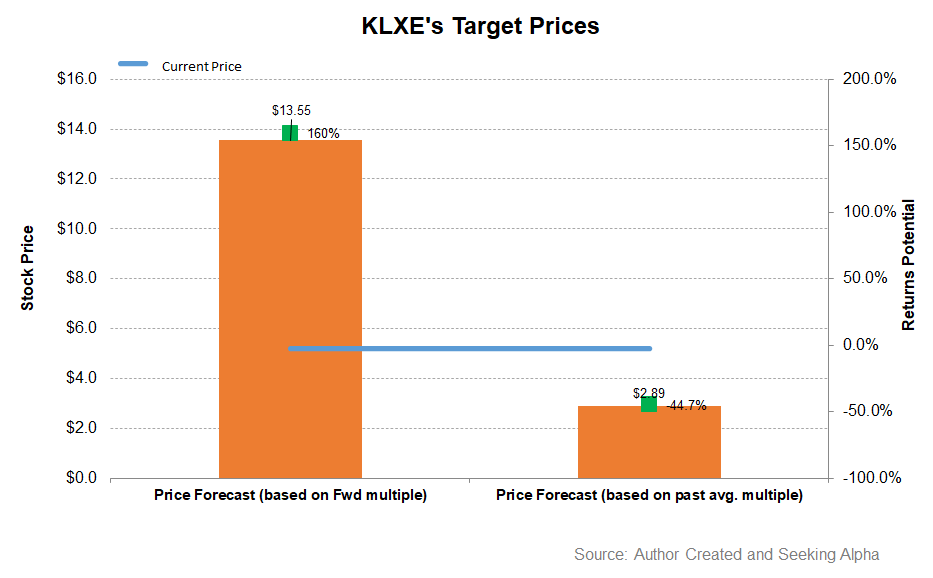

Returns potential using the forward EV/Revenue multiple (0.62x) is higher (160% upside) compared to the expected returns (45% downside) using the past average EV/Revenue multiple (0.77x).

What’s The Take On KLXE?

The oilfield services market will continue to increase prices because a tight labor market will check supply while equipment demand remains high. KLXE, on its part, has increased pricing as it added capacity in coiled tubing, frac rentals, and wireline operations. Its asset utilization remained improved, adding to the rapid pricing recovery. So, its gross and EBITDA margins attained multi-quarter highs in Q2 2022.

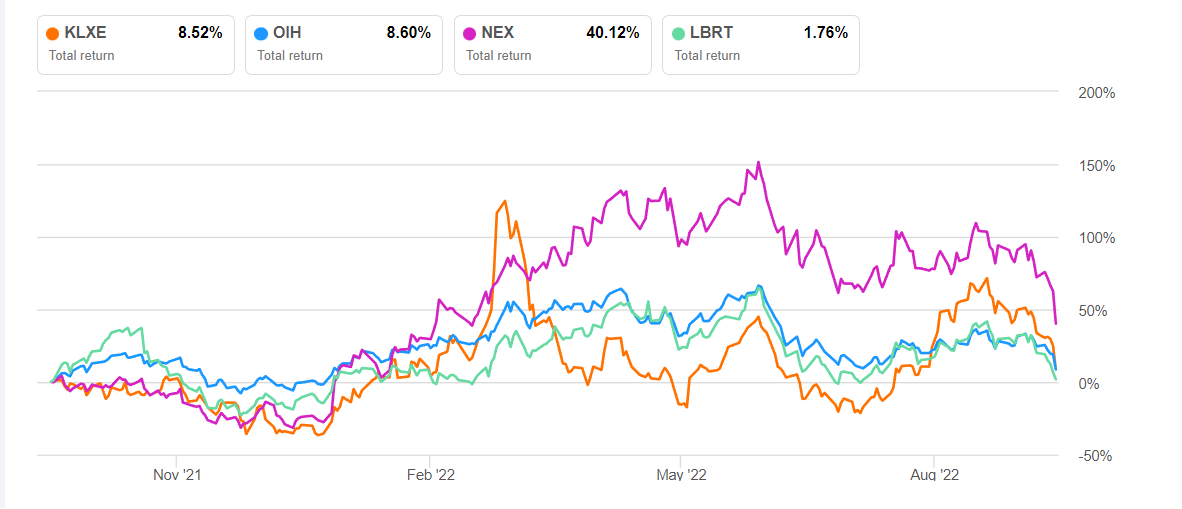

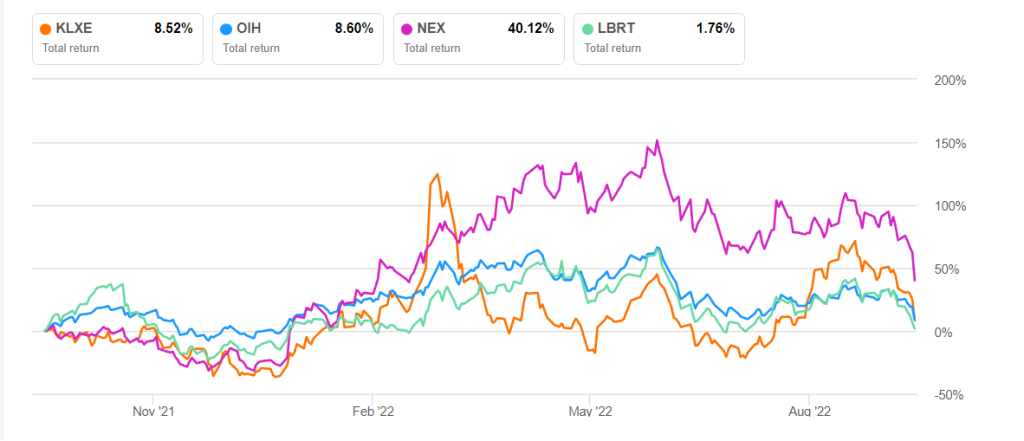

Nonetheless, its cash flows continued to drag. Negative cash flows combined with negative shareholders’ equity pose significant threats to its financial security. The stock performed in line with the VanEck Vectors Oil Services ETF (OIH) in the past year. The management has recently taken a few steps to reduce the balance sheet size, including lowering the borrowings under the ABL facility and refinancing its revolving credit facility. The rise in capex in 2H 2022 will challenge its objective of generating positive FCF in 2022. We do not see much upside as the stock remains volatile.