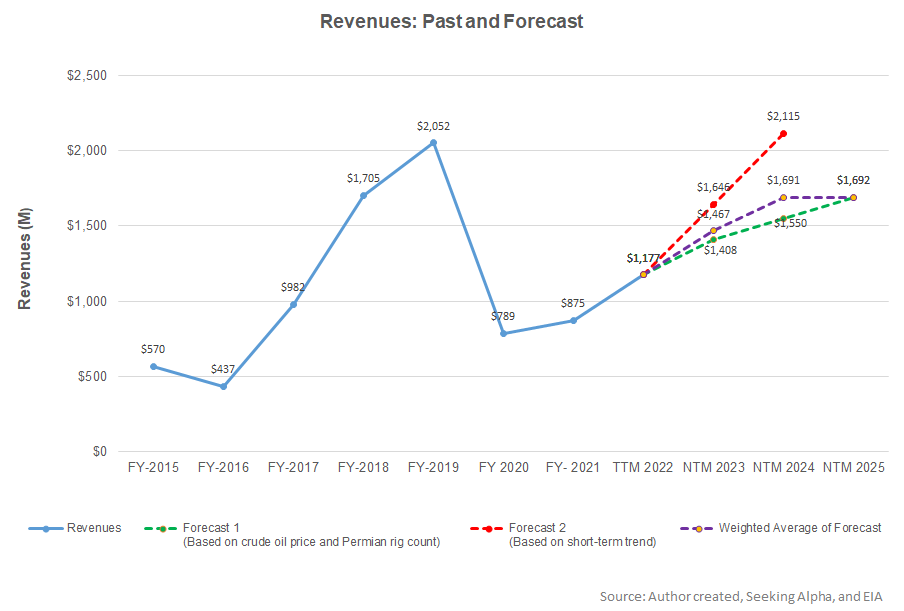

- The regression equation suggests steady revenue growth for PUMP in the next couple of years.

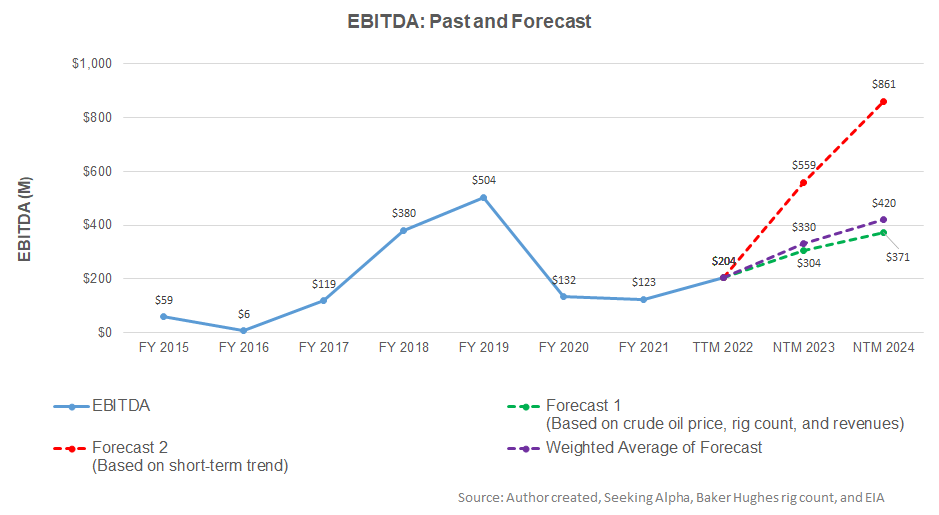

- EBITDA can increase sharply in NTM 2023 but decelerate in NTM 2024.

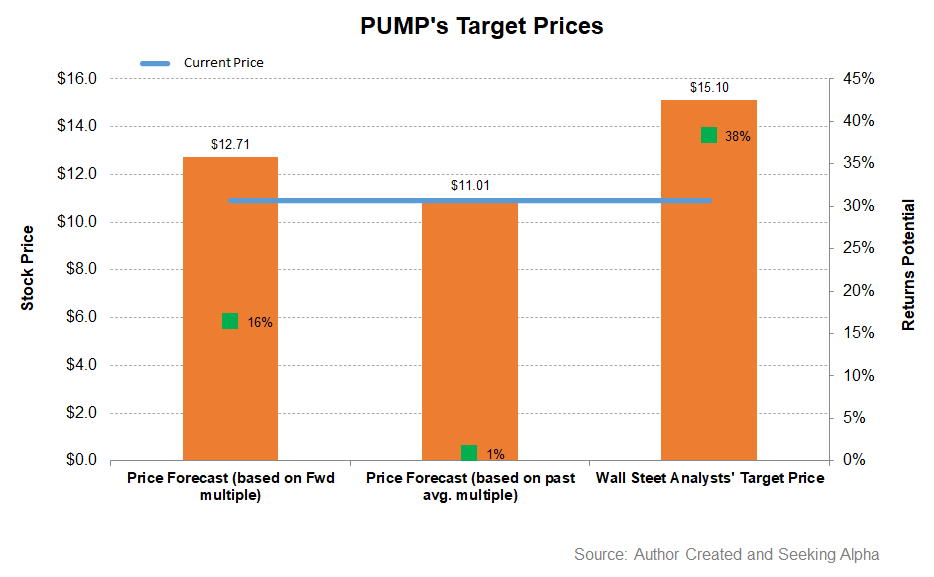

- On a relative basis, the stock is undervalued, with a positive bias.

Part 1 of this article discussed ProPetro Holding’s (PUMP) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Forecast

Based on a regression equation between the key industry indicators (crude oil price and Permian rig count) and PUMP’s reported revenues for the past seven years and the previous four quarters, we expect revenues to increase by 25% in the next 12 months (or NTM 2023). In NTM 2024, it can expand further by 15%, and its revenues can stagnate in NTM 2025.

Based on the regression model, we expect the company’s EBITDA to increase 62% in NTM 2023 and 24% in NTM 2024.

Target Price And Relative Valuation

We have calculated the EV using the forward multiple and the past average multiple. Returns potential (16% upside) using the forward EV/EBITDA multiple (3.8x) is higher than the past average (1% returns potential) but lower than Wall Street’s sell-side analyst expectations (38% upside) from the stock.

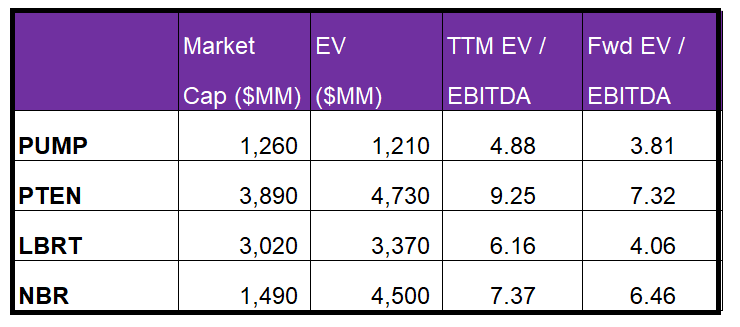

PUMP’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is in line with its peers, which indicates an at-par EBITDA growth versus its peers in the next four quarters. This typically results in a similar EV/EBITDA multiple compared to peers. The company’s EV/EBITDA multiple (4.9x) is lower than its peers’ (PTEN, LBRT, and NBR) average (7.6x). So, the stock is undervalued, with a positive bias, compared to its peers at this level.

The sell-side analysts’ target price for PUMP is $15.1, which, at the current price, has a return potential of 38%. Out of ten, six sell-side analysts rated PUMP a “buy” or a “strong buy,” three rated it a “hold,” and only one a “sell.”

What’s The Take On PUMP?

PUMP, predominantly Permian-centric, focuses on converting its legacy Tier II pressure pumping fleets to Tier IV capacity. Its DGB conversion count can reach seven by mid-2023. It is also working on deploying a couple of electric fleets in 2023. Higher demand, stable utilization, and increased prices for ESG-compliant equipment should produce a healthy return in the coming quarters. In November 2022, it acquired Silvertip, which re-establishes its position as the leading completions-focused oilfield service company.

While negative free cash flow in 9M 2022 can be concerning to the investors, the acquisition is expected to boost the operating profit, double the adjusted EBITDA to free cash flow conversion to 80%. However, given the loss of demand in some international geographies, the economic uncertainty can cast a shadow on PUMP’s outlook. So, the stock underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. Nonetheless, given the relative undervaluation, we think the stock has sufficient catalysts to warrant a buy in the medium term.