Welcome everyone to a new year! While it presents multiple challenges it also offers some room for improvement and we should strive for it anyways.

In this article I am going to primarily talk about Pakistan and also present some trends that we should be wathcing in 2023.

Why am I focusing on Pakistan? Firstly, there are many importand developments happening in the 25th largest economy with the 5th largest population (and a nuclear power as well, residing in of the most geopolitically hot flashpoint of the world) and secondly, because I believe most of these will be repeated in other low and middle income countries (LMICs) across the world.

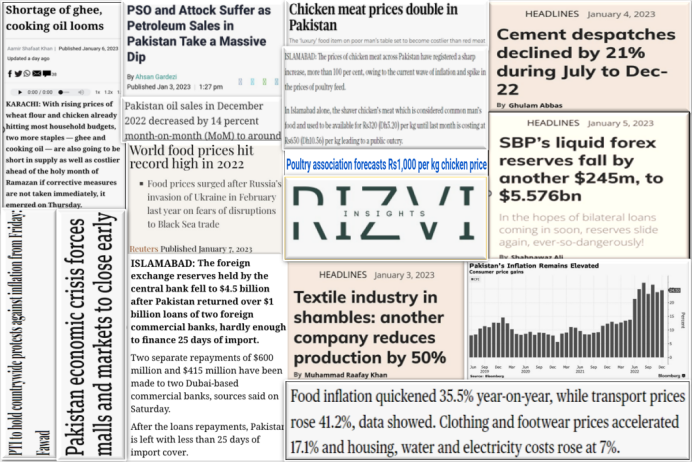

I recently covered this issue in detail in our Monday Macro View (you can watch the show here). One of the most important things that I had no pleasure in making was the following collage (that I realistically termed The Collage of Chaos). You can see that it constitutes mainly of recent headlines coming out of or related to Pakistan and none of it is good.

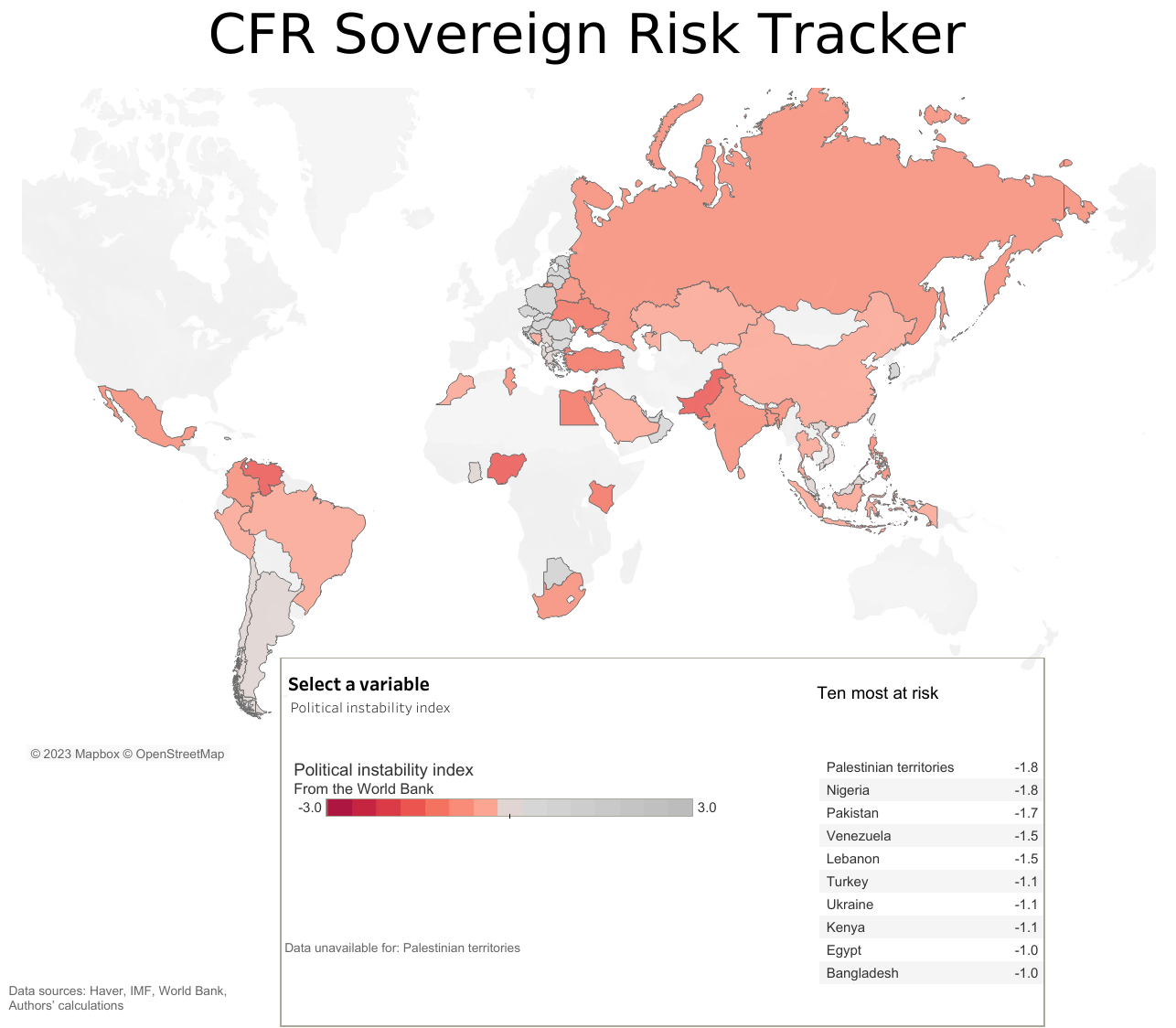

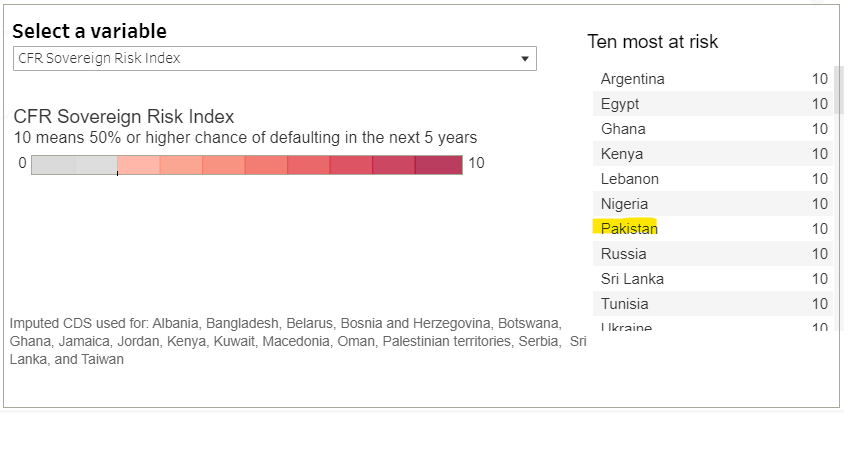

Pakistan’s official inflation figures are 24.5 percent in December that showed a slight improvement from 26.6 percent last month. However, the food inflation has surged 35 percent as compared to last year. Within that basket of food items there are items that have increased more than 100 percent such as onions that registered an increase of 415 percent! While wheat rose 57.3 percent, eggs 54.4 percent, and rice 47 percent. Food price inflation hasbeen worsened by the recent floods that drowned one-third of the country in water destroying 4 million acres of crops across Pakistan. Overall, the economic toll of this recent calamity is estimated to be $35 bn. Moreover, the political instability of the country will continue to haunt economic growth. Cfr’s Sovereign Risk Tracker ranks Pakistan at 10 – meaning it is at the highest risk of instability.

Such trends will be mimicked across the Global South as rising interest rates and cost of debt servicing makes it difficult for countries to finance their day to day operations. Pakistan’s reserves are down to $4.8 billion not enough to cover even 1 month of imports whereas by international standards the benchmark is to have a 3 month import cover bill.

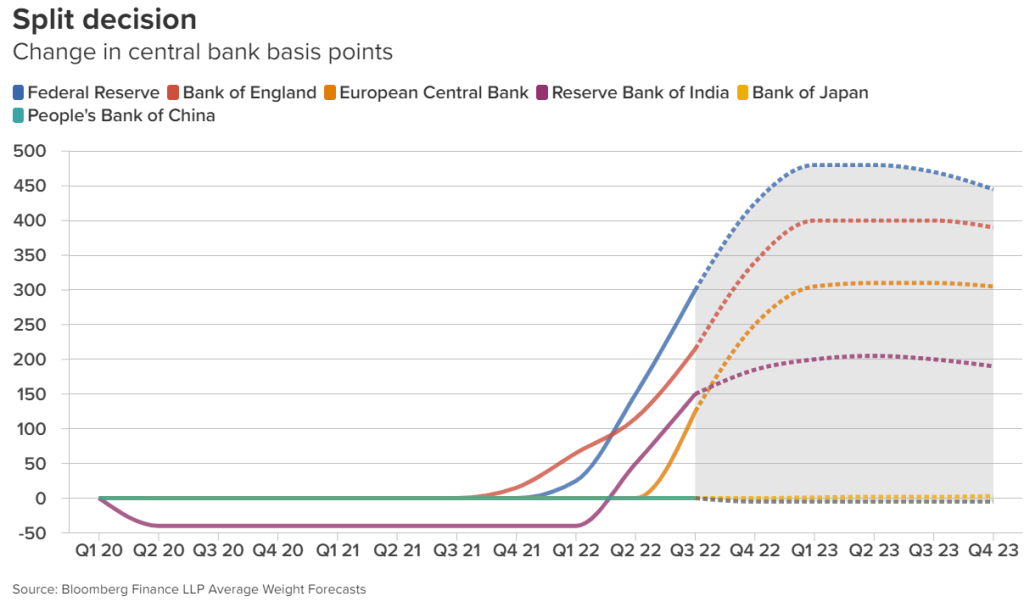

Coming to the global trends we should be looking at firstly the interest rate patterns major central banks across the world. Look at the chart below:

The above chart clearly shows that there is no unanimous direction of major central banks when it comes to their interest rate policy. This will continue to increase noise in the markets and we should expect panic stricken swings and overly optimisitc gains moving forward.

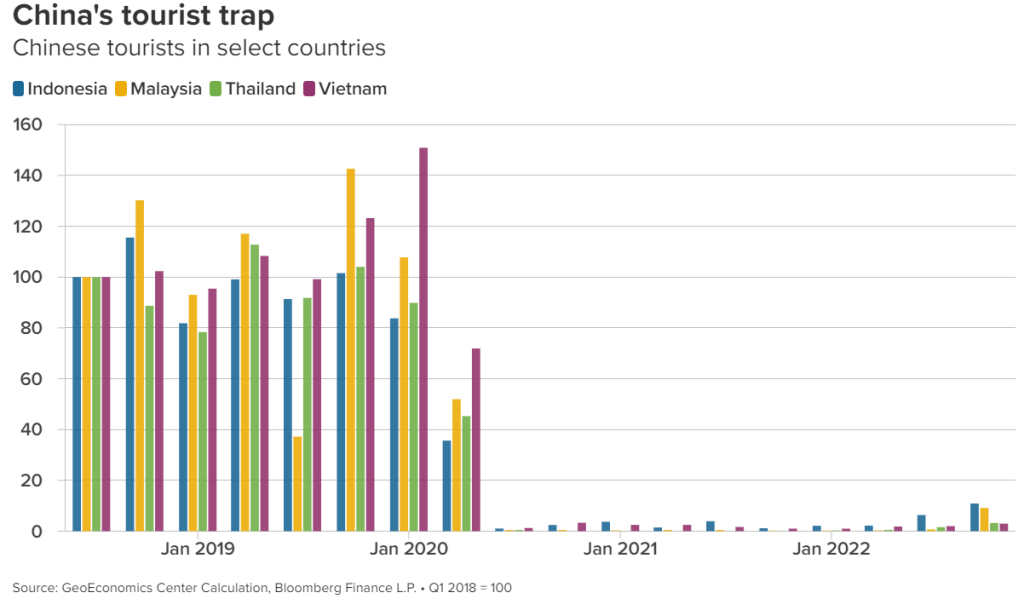

China’s reopening will of course play an important role – one of the ways it will do that is through its impact on tourism industry:

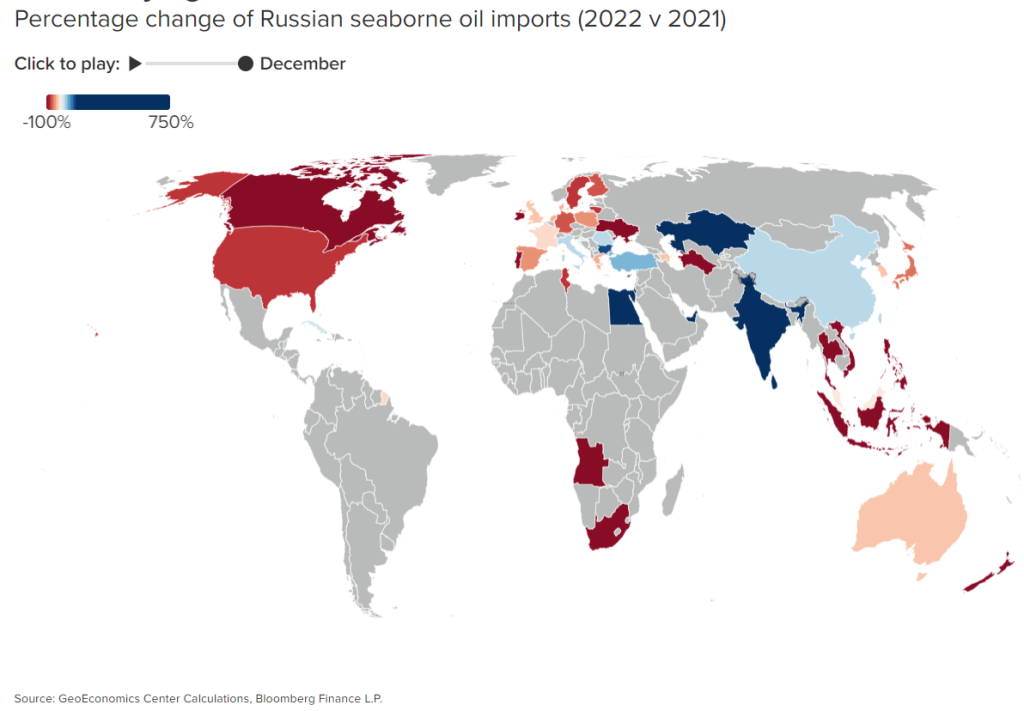

Most importantly, the flow of oil from Russia, its total production and then the countries receiving that oil also need to be followed very closely.

See you all next week!