Iran’s parliament has just voted to shut the Strait of Hormuz – there have been reports. This comes right after U.S. hit three nuclear sites in Iran: Forodow, Natanz and Isfahan. Tehran retaliated with drones and missiles, and now it’s going after the region’s biggest chokepoint. This is serious — it’s not just symbolic. Oil prices jumped immediately – but so far it looks the impact on prices will be temporary. Washington is still weighing whether to get involved. Meanwhile, markets are bracing for what comes next. Many people are talking about how China will suffer the most if Hormuz is closed. This explainer explains that why that might not be the case.

What is the Strait of Hormuz

It’s a narrow but critical waterway between Iran and Oman. It connects the Persian Gulf with the Gulf of Oman and the Arabian Sea. Most of the oil exported from Gulf countries has to go through this strait. It’s also deep and wide enough to handle the biggest oil tankers in the world. So when Hormuz is in play, the entire global oil market reacts. So far the passageway remains open.

How much oil and gas passes through it

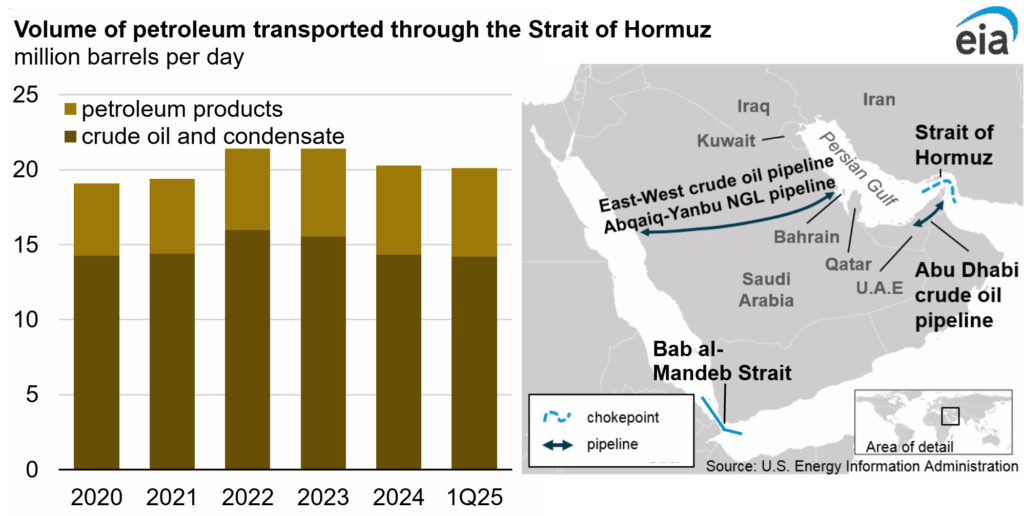

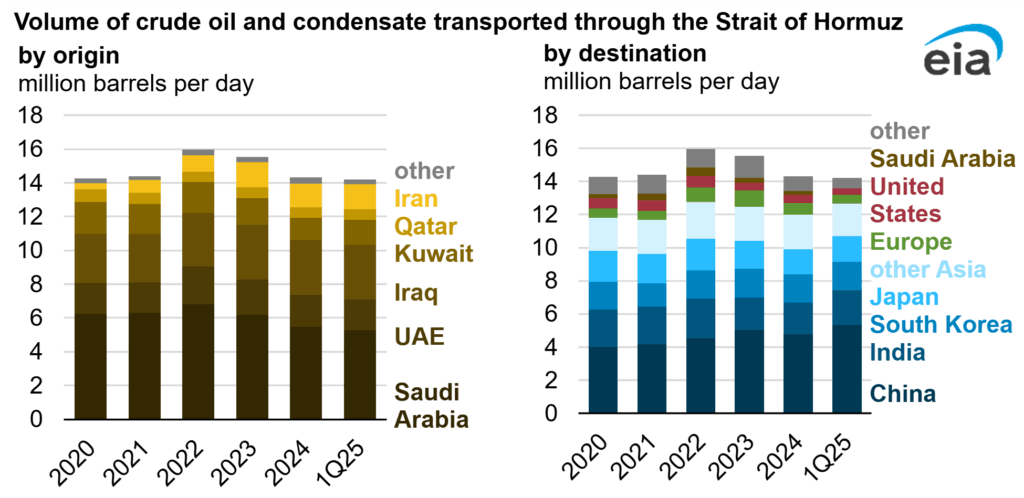

In 2024, about 20 million barrels of oil per day passed through Hormuz. That’s 20% of global oil consumption. Of that, crude oil and condensate flows made up 15.7 million b/d, and petroleum products another 4.3 million b/d. It’s not just oil — Hormuz also carried one-fifth of global LNG trade, mainly from Qatar. The biggest users of that oil are in Asia. In 2024, 84% of the crude and condensate through Hormuz went to Asia. China, India, Japan, and South Korea together accounted for about 69% of all Hormuz oil flows. China alone was a top buyer of Iranian crude — estimates suggest it was importing up to 1.5 million barrels per day from Iran.

Are there any alternative routes

Yes, but they’re limited and already stretched.

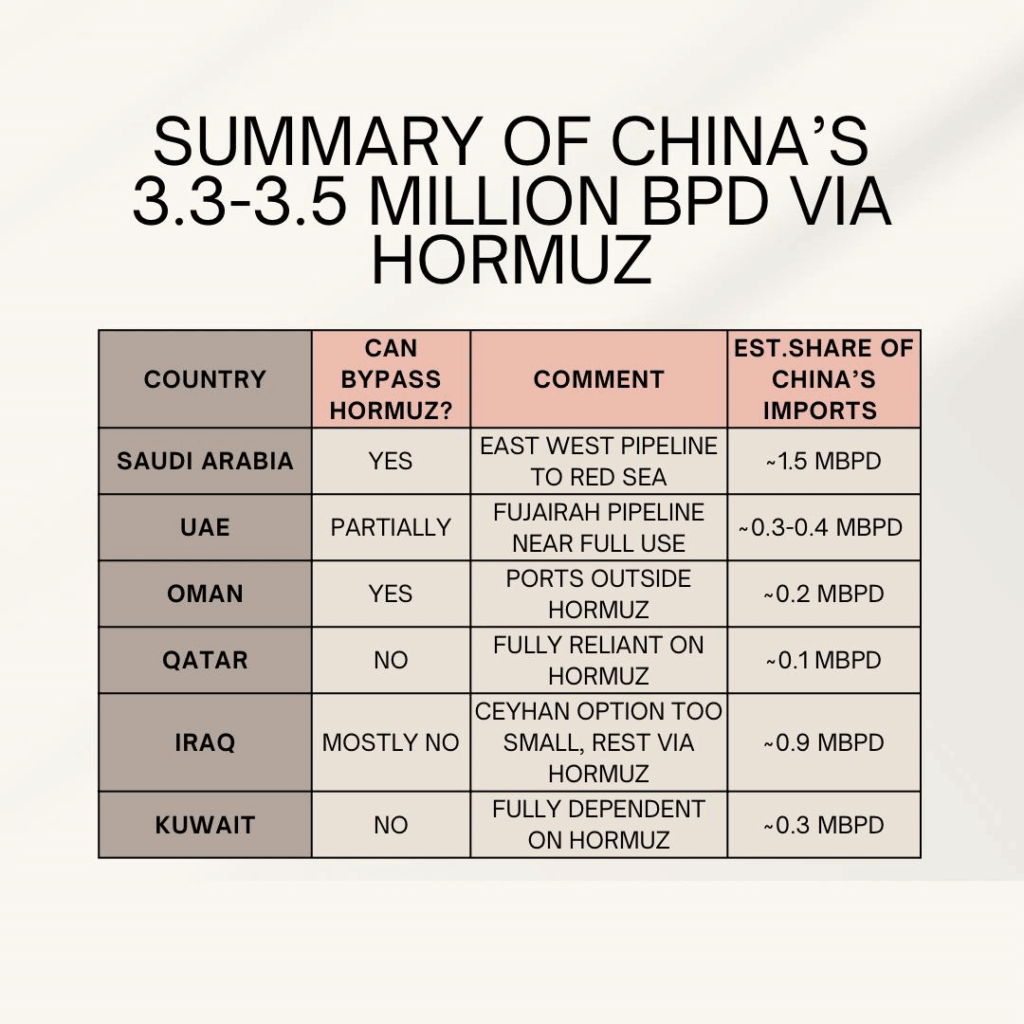

- Saudi Arabia has the East-West pipeline that can handle up to 7 million b/d, though in 2024 it was mostly running below capacity.

- The UAE has a pipeline to Fujairah with a max of 1.8 million b/d. It has been using more of this line lately for regular flows, leaving less spare capacity.

- Iran has the Goreh-Jask pipeline, which technically avoids Hormuz. But in reality, Iran was exporting less than 70,000 b/d through it in mid-2024, and it stopped shipping altogether by September that year.

So yes, there are workarounds — but not enough. The combined bypass capacity from Saudi and UAE pipelines is around 2.6 million b/d, far below the 20 million b/d that normally moves through Hormu

China won’t be impacted the way people think

People expect China to be the most vulnerable — it’s the world’s biggest oil importer and a top customer of Iranian crude. And yes, around 45% of China’s oil imports — about 3.3 to 3.5 million barrels per day — come through the Strait of Hormuz. But that’s not the whole story.

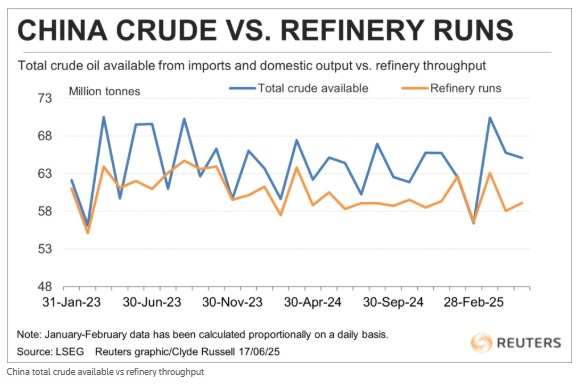

Since March 2025, China has been quietly stockpiling crude. In May alone, it added 1.4 million barrels per day to reserves – this is the third month that the country has added more than 1 mbpd to its inventories. The five-month average surplus was around 990,000 bpd. That means China has been importing far more than it’s refining — and storing the excess.

Now we know how much has built up. According to Kayrros, total Chinese onshore crude inventories hit a record 1.18 billion barrels — the highest ever. Shandong province alone holds 355 million barrels, thanks to new tank capacity and upgraded refineries. This gives China serious breathing room. Its independent refiners — the “teapots” — are already slowing down, running at just 45% utilization, the lowest in months. So demand pressure is already light.

Let’s look at exposure. Of the 3.3–3.5 million bpd China gets through Hormuz (excluding Iran):

If China lost 1.5 million bpd from Iran, and relied only on its 1.18 billion barrels in stock, it could cover that loss for about 785 days — that’s more than two years. But if broader Hormuz flows are hit and China faces an even bigger shortfall — say 2.5 to 3 million bpd — the buffer could still last 3 to 6 months even with zero alternative supply.

In that time, China can maneuver: it could reduce refinery runs further, draw on Russian and West African supplies, or lean harder on its teapots to cut back. Some are already doing that — demand for Iranian light crude has slowed, despite it trading at $2–3 per barrel below Brent, and a few July delivery deals have even been cancelled.

So yes, China is exposed — but thanks to its massive reserves, pipeline access, and slower refining, it’s in a much stronger position than most.