Q3 Order Booking Summary: BKR’s total book-to-bill ratio deteriorated to 1.0x in Q3 2024 compared to 1.1x in Q2. During Q3, its Gas Technology Equipment secured orders to supply ten units of Integrated Compressor Line to Dubai Petroleum Establishment to support gas infrastructure. It received a contract to supply advanced compression solutions to Saipem. It also secured a multi-decade agreement for an LNG facility in the Middle East for its Gas Technology Services. The OFSE segment secured orders to supply flexible pipe systems in Brazil’s Santos Basin. It won a MAS (mature assets solutions) award to supply Santos Energy’s Cooper Basin Development in Australia.

BKR’s intelligent automated field production digital solution saw increased adoption in the Permian Basin. In decarbonization, it launched CarbonEdge, an end-to-end, risk-based digital solution for real-time data and alerts on carbon dioxide flows across CCUS infrastructure.

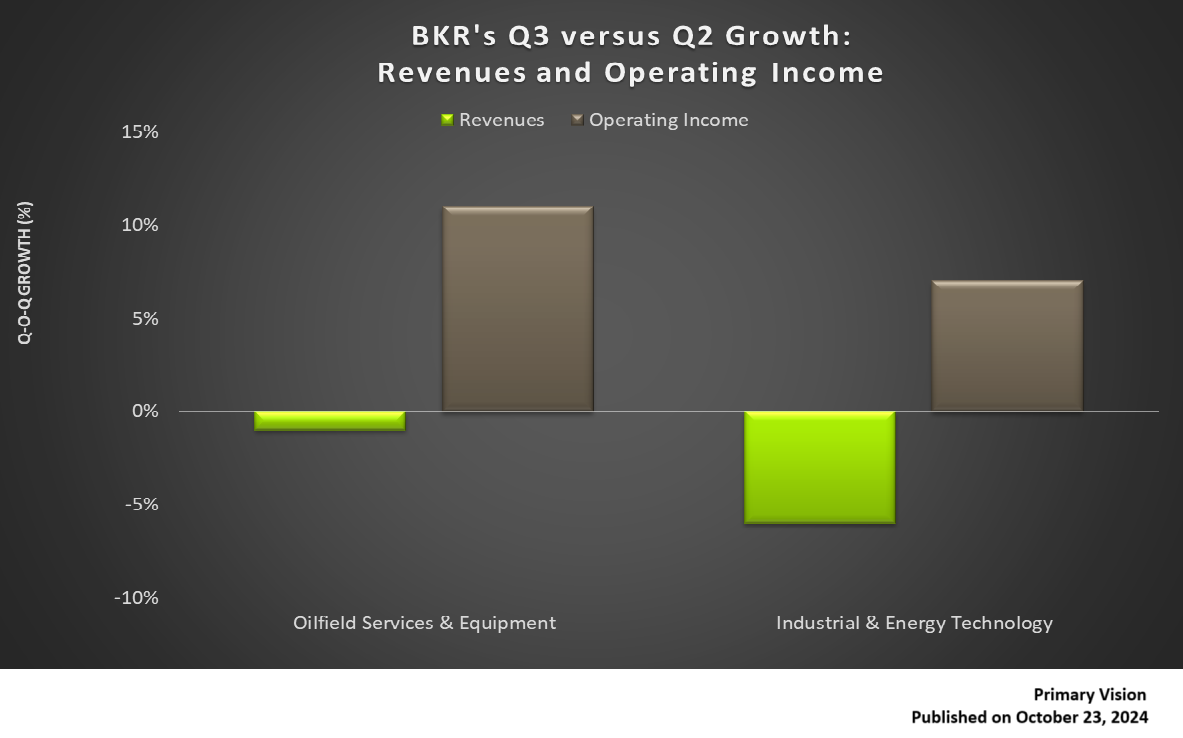

Revenue Weakened But Income Strengthened In Q3: In the Industrial & Energy Technology segment, revenues decreased by 6% quarter-over-quarter, while operating profit went up by 7%. Despite lower sales, better pricing and productivity impacted the operating margin positively in Q3. The revenue visibility was also discouraging, as order booking decreased by 17% in this segment due to lower GTE orders in Q3. Revenues in the Oilfield Services & Equipment segment were relatively steady in Q3. Europe, CIS, and Sub-Saharan Africa produced higher sales, offset by lower North American turnover in Q3.

On the other hand, positive price and productivity boosted operating income by 11% quarter-over-quarter. However, order booking deflated (6% down) in this segment. Lower orders in Subsea and Surface Pressure Systems contributed to the OFSE order decline in Q3.

During Q3, BKR’s EBITDA margins increased to 17.5%, and the company’s management maintained its midpoint EBITDA guidance. It is also expected to become “less cyclical and capable of generating more durable earnings” with strong recurring IET service revenue, production-levered businesses, and an improved cost structure.

Cash Flow Steadied; Leverage Improved: BKR’s cash flow from operations remained nearly unchanged in 9M 2024 compared to a year ago. Its FCF decreased by 4% during this period. Debt-to-equity (0.37x) improved slightly compared to December 31, 2023. It repurchased shares worth $152 million in Q3. You may read more about the company in our previous article here.

Thanks for reading the BKR Take Three, designed to give you three critical takeaways from BKR’s earnings report. Soon, we will present a second update on BKR earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.

Premium/Monthly

————————————————————————————————————-