Eurozone Market Sentiment Tracker

Bullish sentiment in the Eurozone is supported by the European Central Bank’s aggressive monetary easing. Five consecutive rate cuts have lowered the deposit rate to 2.75%, a move that is expected to stimulate borrowing, consumption, and investment. In addition, the manufacturing sector is showing early signs of stabilization: the Purchasing Managers’ Index improved from 45.1 in December to 46.6 in January, indicating that contraction is slowing and that growth might soon emerge. Complementing these factors is a resilient labor market—with historically low unemployment and a gradual recovery in private consumption—which helps underpin a modest economic rebound across the bloc.

However, bearish factors weigh on sentiment as well. Headline inflation has risen to 2.5% in January, driven by a surge in energy prices, and remains above the ECB’s 2% target, which continues to generate uncertainty about the inflation trajectory. GDP data reveal divergent performance among major economies; for instance, Germany and France recorded contractions of –0.2% and –0.1% respectively in Q4 2024. Moreover, services growth in the Eurozone has cooled to some of the weakest rates seen over the past year. Heightened trade policy uncertainty—including the potential for further US tariffs on European goods—and ongoing geopolitical risks could depress both investment and export demand, adding to overall caution.

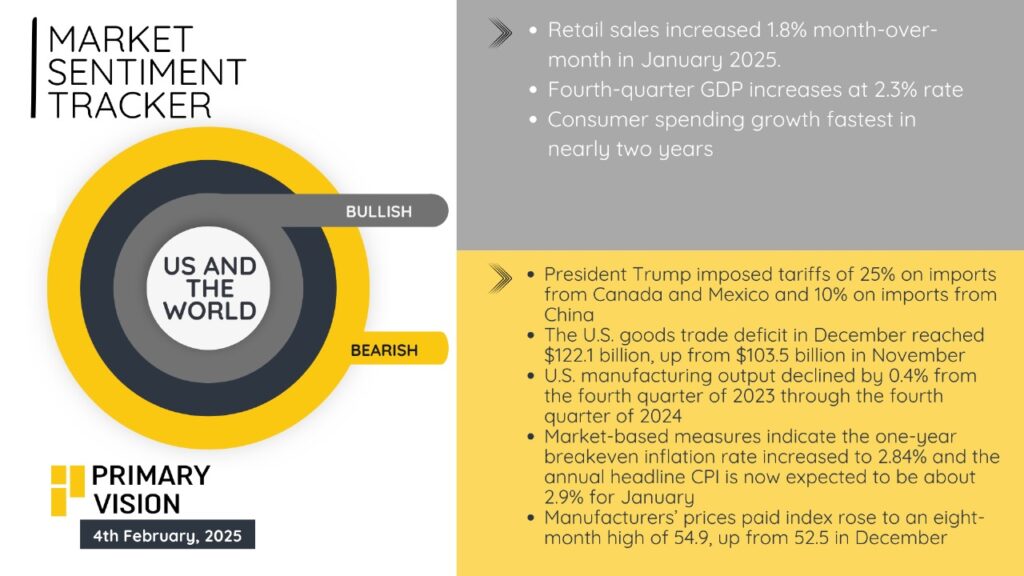

US Market Sentiment Tracker

US market sentiment is characterized by a mixed outlook, where robust domestic activity contrasts with significant external headwinds. On the bullish side, retail sales in January 2025 rose by 1.8% month‐over‐month, reflecting strong consumer demand, while fixed investment expanded by 5.0% year‐over‐year, signaling increased business confidence. Consumer inflation remained subdued at 1.7% year‐over‐year, and official urban unemployment held steady at 5.0%, reinforcing a solid labor market that supports overall economic resilience. These indicators suggest that domestic consumption and investment are providing a strong foundation for growth.

In contrast, bearish factors stem primarily from trade and manufacturing challenges. President Trump’s imposition of tariffs—25% on imports from Canada and Mexico and 10% on imports from China—has contributed to external economic pressure. The US goods trade deficit in December soared to $122.1 billion from $103.5 billion in November, indicating a widening imbalance in trade. Furthermore, US manufacturing output declined by 0.4% from Q4 2023 to Q4 2024, while market-based measures show that the one-year breakeven inflation rate increased to 2.84% and the headline CPI is now expected to be around 2.9% for January. Finally, the manufacturers’ prices paid index reached an eight‐month high of 54.9 (up from 52.5 in December), signaling rising input costs that could erode profit margins and dampen future investment.

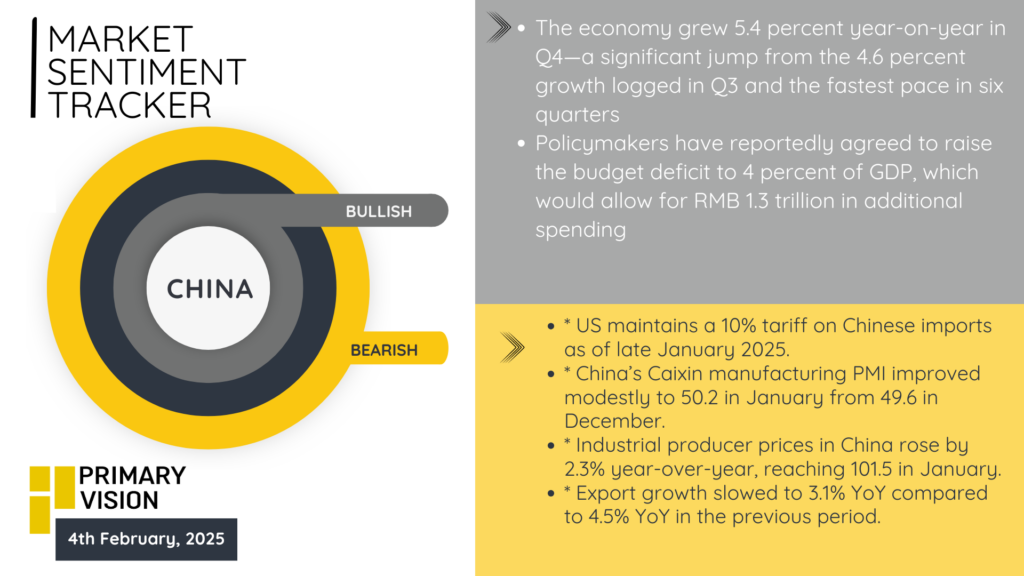

China Market Sentiment Tracker

Based on the provided data, the bullish factors for China are reported as identical to those for the Eurozone. According to this information, China benefits from aggressive monetary easing with five consecutive rate cuts that have lowered the deposit rate to 2.75%. This easing is intended to boost liquidity, encouraging both consumer spending and business investment. Additionally, manufacturing activity in China is said to be showing early signs of stabilization, as reflected by an improving Purchasing Managers’ Index (PMI) that rose from 45.1 in December to 46.6 in January. A resilient labor market—featuring historically low unemployment and a gradual recovery in private consumption—further supports the expectation of a modest economic rebound.

Conversely, the bearish factors for China mirror those listed for the Eurozone. Headline inflation has risen to 2.5% in January, driven by surging energy prices, and remains above the target of 2%, creating concerns about persistent inflationary pressures. GDP data reportedly indicate divergent performance among major economies, with contractions noted in countries like Germany and France (–0.2% and –0.1% respectively in Q4 2024). In addition, services growth in the region is described as having cooled to one of the weakest rates seen over the past year, while heightened trade policy uncertainty—particularly the potential for further US tariffs on European goods—and ongoing geopolitical risks may depress investment and export demand.