ProPetro will keep its frac spread count nearly unchanged in 2025, although the share of electric frac deployment will rise. The most notable development in recent times is the setting up the PROPWR subsidiary, which entails its foray into the natural gas-fueled power generation equipment market. It has won significant new orders in this business. On top of that, the cementing, Silvertip wireline, and AquaProp sand logistics businesses will continue to strengthen the company’s operations. However, in Q4, revenues from hydraulic fracturing fell.

Frac’ing Update

In our short article, we discussed our initial thoughts about ProPetro Holding’s (PUMP) Q4 2024 performance a few days ago. This article will dive deeper into the industry and its current outlook. In Q4, PUMP kept its fracturing frac spreads unchanged at 14, although utilization decreased. It plans to run 14-15 frac spreads in Q1 2025. Currently, it operates four electric fracs under long-term contracts. It plans to deploy the fifth e-frac spread in 2025.

Investors may note that early in 2024, PUMP inked a three-year contract with ExxonMobil to provide hydraulic fracturing, wireline, and pump-down services through the FORCE e-fracs. As it builds its e-frac portfolio, PUMP will reduce its Tier II diesel-only equipment investment. Electric fracs offer lower costs to customers through fuel savings. The Tier IV dual-fuel and electric fleet assets continue to be highly utilized. PUMP estimates that 75% of its fleet consists of next-generation gas burning equipment.

PROPWR Prospect

In December, PUMP received an initial order of 110 megawatts of natural gas-fueled power generation equipment with a further agreement to purchase an additional 30 MW. It will carry out the business under a subsidiary called PROPWR. The deliveries, expected to be spread in Q2 2025 and 2026, will bring the total capacity to 150 MW – 200 MW.

PROPWR is expected to capitalize on multiple high-growth verticals as demand for reliable low-emission power solutions increases fast. Besides traditional markets like drilling, completions, production, and midstream operations, power solutions can significantly grow in industrial power applications. Further, in the long term, opportunities arise from the data center space in Permian as it deploys scalable, low-cost natural gas-powered energy solutions for data center developers.

Strategic Priorities

- PUMP’s cementing, Silvertip wireline, and AquaProp sand logistics businesses continue to contribute to the company’s financial strength

- In Q4, utilization fell primarily due to the adverse effects of seasonality

- However, its bifurcated service offering reduced the seasonality impact

- The company’s divestiture of the Utah cementing operations in Q4 aligns with its Permian-focused strategy

- Utilization rates continue to trend upward, primarily for its frac spreads

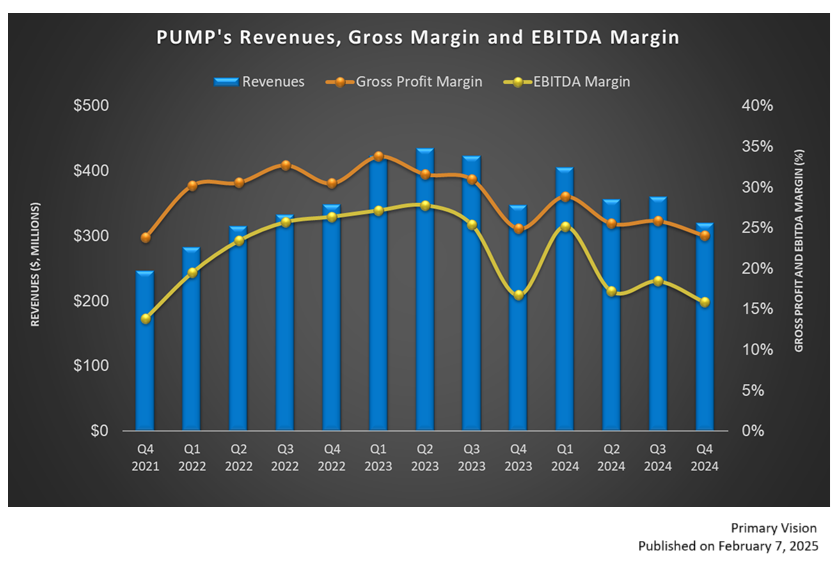

Q4 Results And Financial Metrics

As we discussed in the Q4 earnings article, quarter-over-quarter, PUMP’s revenues from the Hydraulic Fracturing segment decreased by 14% in Q4 2024, while its adjusted EBITDA decreased by 17%. Its revenues and adjusted EBITDA from the Wireline segment decreased by 6% and 23%, respectively.

PUMP’s cash flow from operations decreased significantly (by 33%) in FY2024 compared to FY2023. Its free cash flow, however, increased significantly as capex fell even more sharply during this period. Its FY2025 capex guidance is $300 million-$400 million, much higher than FY2024. Of this, $150 million to $200 million will be allocated for the PROPWR business. By December 31, its liquidity was $161 million. Since the inception of the share repurchase program in May 2023, it has returned $111 million of capital to its shareholders.

Relative Valuation

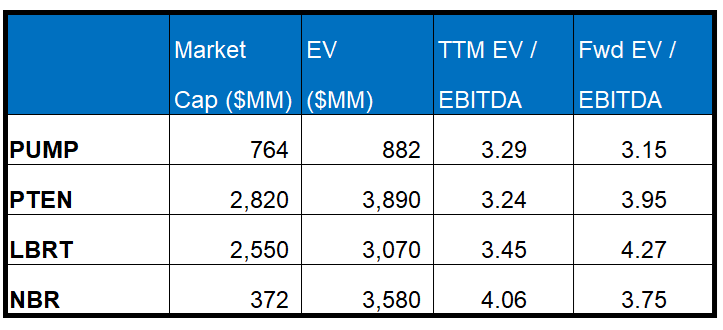

PUMP is currently trading at an EV/EBITDA multiple of 3.3x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 3.2x. The current multiple is below its five-year average EV/EBITDA of 4.7x.

PUMP’s forward EV/EBITDA multiple contraction versus the current EV/EBITDA contrasts its peers because its EBITDA is expected to increase compared to a fall in EBITDA for its peers over the next year. This typically results in a much higher EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple is lower than its peers’ (PTEN, LBRT, and NBR) average. So, the stock is undervalued compared to its peers.

Final Commentary

After Q4, PUMP kept its frac spread count unchanged and expects to add one more in 2025. In the ExxonMobil contract, it expects to deploy the fifth FORCE electric spread in the next few months. Diversifying into mobile power solutions, it has floated a subsidiary called PROPWR. It has an initial order of 110 megawatts of natural gas-fueled power generation equipment with a further agreement to purchase an additional 30 MW. It expects to witness robust opportunities arising from the data center space in Permian for natural gas-powered energy solutions.

However, In Q4, utilization fell primarily due to the adverse effects of seasonality. PUMP’s cash flow from operations decreased significantly in FY2024. Its FY2025 capex guidance is much higher than FY2024 following capital allocated for the PROPWR business. The stock is undervalued compared to its peers.

Premium/Monthly

————————————————————————————————————-