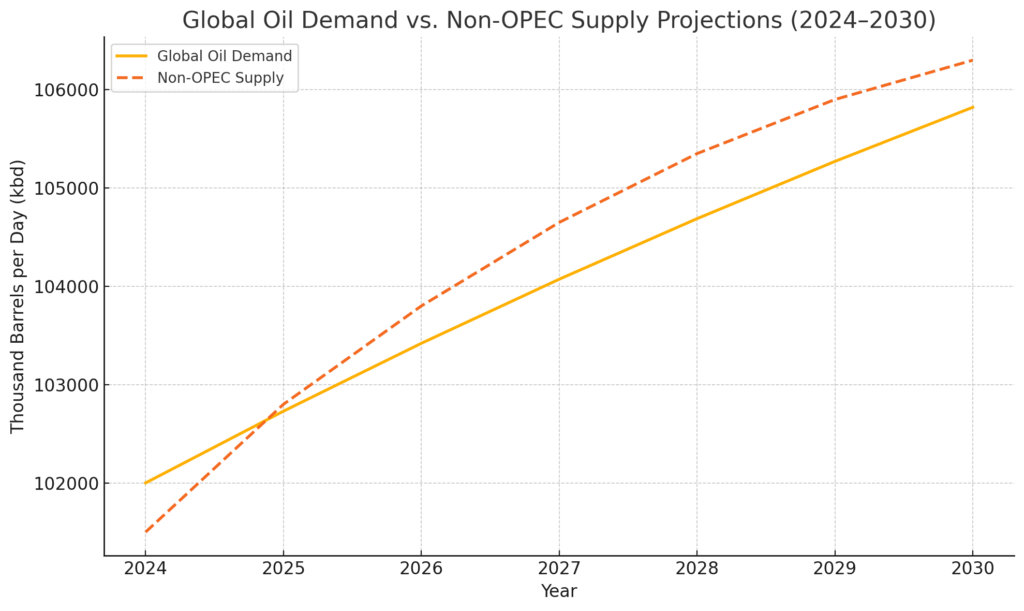

The global oil market is going through a rough patch, and it’s not just about supply and demand anymore — it’s politics, economics, and shifting long-term trends all colliding. The International Energy Agency has just cut its global oil demand growth forecast for 2025 to 730,000 barrels per day, which would be the slowest pace since the early pandemic days. And looking into 2026, things don’t improve much, with growth dipping further to 690,000 bpd. The IEA points to a mix of economic fragility, especially in China, and the increasing adoption of electric vehicles as major reasons. That’s a pretty big deal, considering China had long been the engine room for global oil consumption.

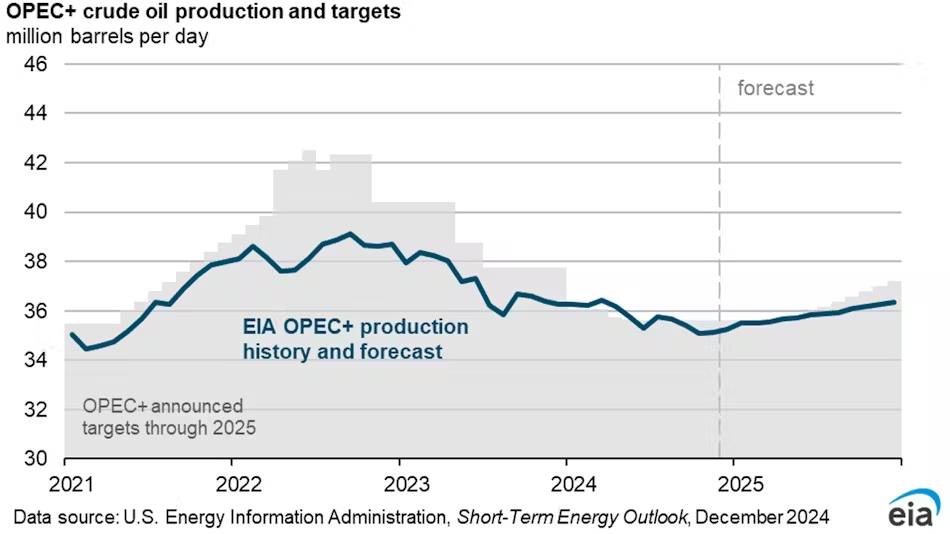

On the supply side, the game is changing too. Non-OPEC producers are set to pump more, with the IEA forecasting a 1.3 million bpd increase in 2025 alone — far outpacing demand. U.S. supply is still expected to grow, but more slowly now, especially with new tariffs weighing on production costs. The irony is thick here: even as the U.S. talks tough about energy independence and ramping up output, its shale producers are facing the reality of thinner margins and tighter access to steel and gear due to tariff wars. Assuming demand rises 730,000 bpd in 2025 and non-OPEC supply rises 1.3 million bpd, that leaves a theoretical surplus of about 570,000 bpd. Over a year, that’s nearly 208 million excess barrels. With global spare storage already tightening post-2022 drawdowns, this mismatch will keep a lid on prices unless OPEC+ offsets it — which so far, they’ve shown little discipline in doing.

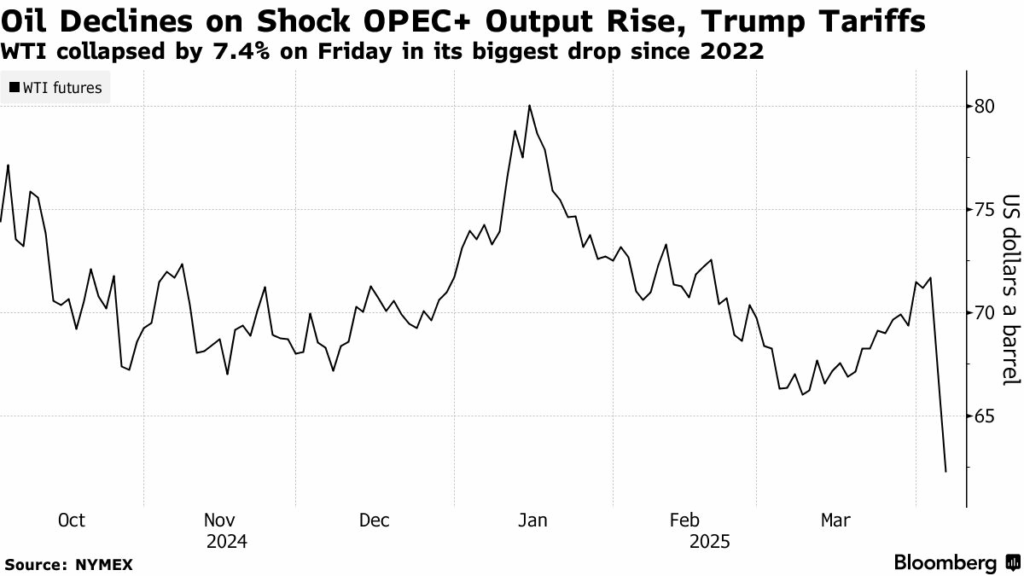

All of this is happening against a backdrop of tumbling oil prices — Brent fell below $60 recently, the lowest since early 2021 — and that’s sending shockwaves through oil-dependent economies. From Saudi Arabia to Venezuela, many producers are suddenly scrambling to plug budget gaps. Saudi Arabia, for one, is back in debt markets, issuing nearly a billion dollars in sukuk just in April. That follows an already aggressive borrowing streak, with the kingdom among the top emerging market debt issuers last year. Riyadh has big ambitions with its Vision 2030 plan, but lower oil revenue and shrinking dividends from Aramco are forcing it to reconsider some timelines. The government is trying to balance the books without stalling economic diversification efforts, but they’re clearly having to recalibrate.

The IMF estimates Saudi Arabia needs over $90 oil to balance its budget. With Brent at $60–65, that’s a shortfall of $25–30 per barrel. Given that Saudi production is around 9 million bpd, even conservatively assuming 8 million bpd are exported at these prices, Riyadh is losing $200–240 million per day in potential budgetary revenue. Multiply that over a year, and you’re looking at a shortfall of $73–88 billion — a major hit for a country planning trillion-dollar megaprojects. It’s not just the Gulf. Kuwait finally passed a debt law after years of gridlock, enabling it to return to global capital markets to finance its deficits. Iraq, Nigeria, and Iran are all feeling the squeeze, with their budgets built around higher oil price assumptions that no longer look realistic. Even Russia, which had weathered sanctions and price volatility before, is starting to wobble again, with its non-defense sectors stagnating and pressure mounting for interest rate cuts.

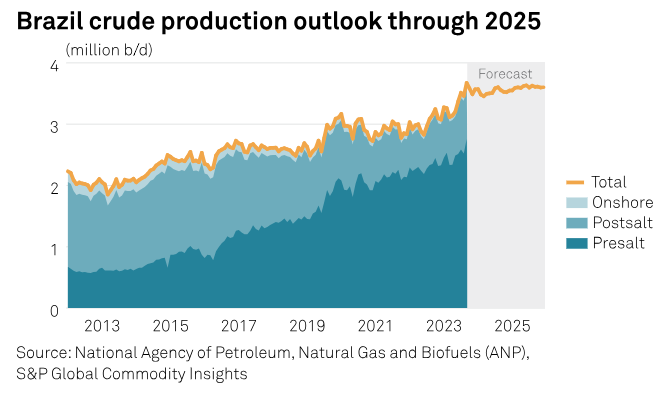

Russia’s 2025 budget assumes $69.70 per barrel. If Brent averages $62 instead — a not-unlikely scenario — Moscow will fall short by roughly 11%. With oil and gas making up more than a third of government revenue, that gap could translate into a 3.5–4% hole in federal income, likely requiring either deeper borrowing or cuts. That, combined with ongoing sanctions and inflation, puts Russia at risk of stagflation. In Latin America, Brazil is scrambling too — looking to speed up auctions for offshore oil stakes to bring in extra cash. And Venezuela, already deep in crisis mode, now has to contend with even less revenue and tighter U.S. sanctions that are choking off whatever exports are left. Brazil had budgeted for Brent at $80.79 for 2025. With current prices $20 below that, the fiscal math changes fast. A 25% shortfall in price expectations could cut oil-linked revenue projections by at least 20–25 billion reals (~$4–5 billion), forcing either mid-year revisions or fiscal tightening.

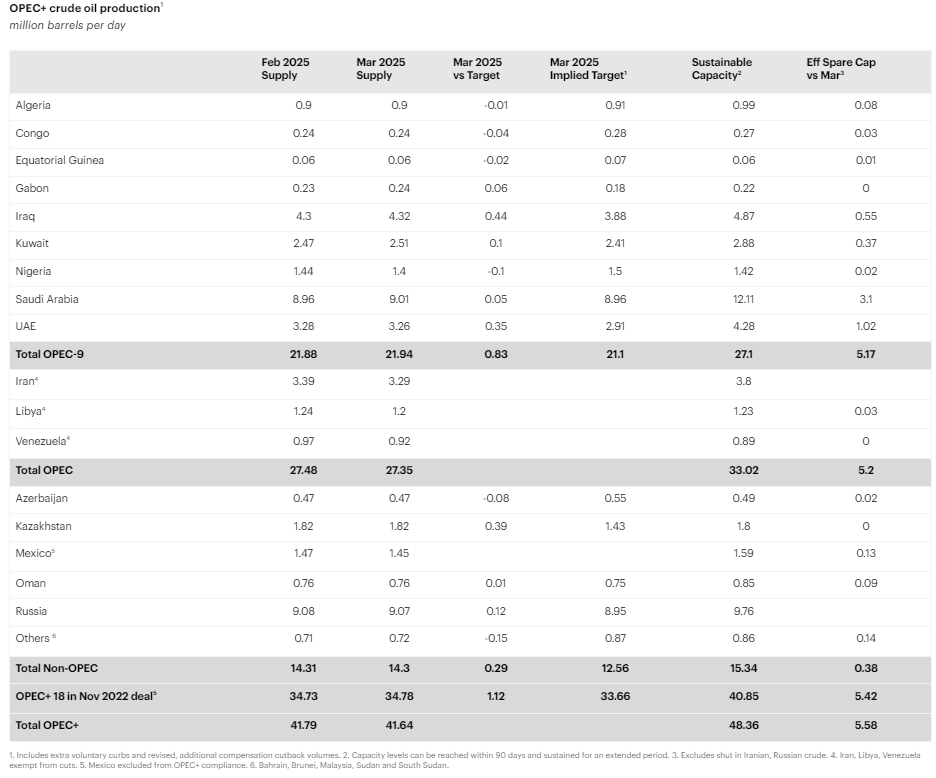

It’s a mess for OPEC+ too. Their decision to ramp up supply in May just added fuel to the fire, and attempts to compensate for earlier overproduction by some members have fallen flat. Market confidence in their cohesion and ability to manage prices is clearly shaken. In fact, OPEC+ is on a slippery slope. The group’s internal quota discipline has always been shaky, but now it’s worse. With compensation efforts looking increasingly symbolic, and national pressures growing, the cartel risks triggering a self-reinforcing price spiral. Every member is thinking: “If prices are going to be low anyway, I might as well sell more.” That’s a textbook prisoners’ dilemma — and the market knows it.

What we’re looking at isn’t just another cycle — it feels like a turning point. Structural shifts are taking shape: the EV transition is real, demand growth is losing steam, and supply is increasingly coming from outside the traditional powerhouses. For oil producers, the playbook of the past — cut output, wait for prices to rise — may not work like it used to. Everyone’s watching to see how these economies adapt, whether through reform, diversification, or just sheer borrowing power. To underscore the scale of this transition: if EVs displace just 3 million barrels per day by 2030 — a conservative estimate — that alone would erase almost four years of cumulative demand growth at current trends. That’s not a dent; that’s a structural demand shift. But one thing’s clear — the age of easy oil-driven prosperity is slipping further into the rearview. And with over $168 billion in energy-related sovereign debt coming due across the GCC by 2029, the financial fuse is already lit. The next few years aren’t just about navigating volatility — they’re about fundamentally rethinking what it means to be an oil economy in a world that increasingly wants less of it.

Basis for Calculations:

- Starting global oil demand: 102 million barrels/day in 2024

- IEA demand growth: +730k bpd in 2025, +690k bpd in 2026

- Post-2026 demand growth slows ~5.5% per year

- Non-OPEC supply grows: +1.3 million bpd in 2025, tapering to +800k bpd by 2027, and slowly declining after

- Supply and demand are expressed in ‘000 barrels/day (kbd)