- Our regression model suggests that Liberty’s revenues will rise rapidly in NTM 2023 but can decelerate in NTM 2024

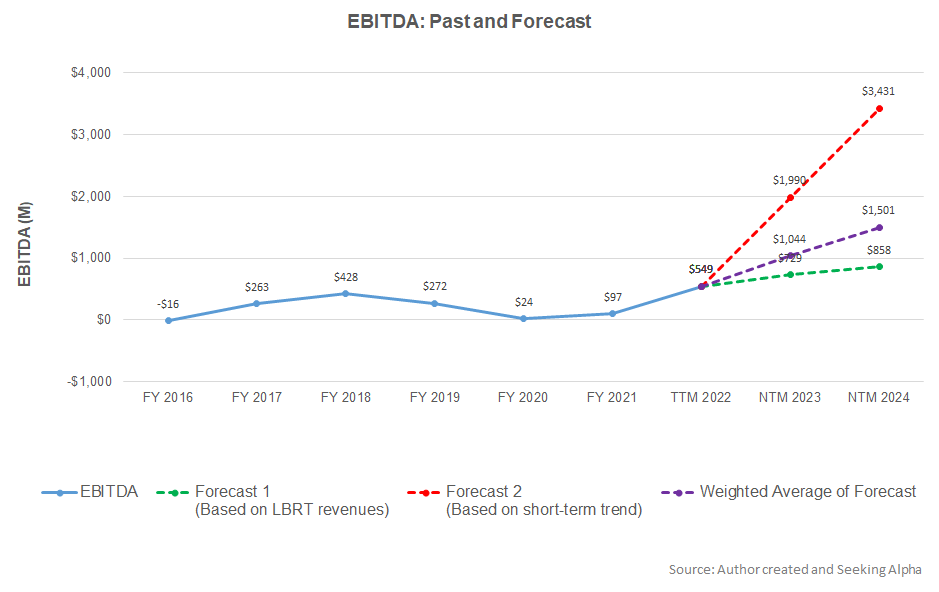

- EBITDA can nearly double in NTM 2023 but will fall sharply in NTM 2024

- The stock is reasonably valued versus its peers

In Part 1 of this article, we discussed Liberty Energy’s (LBRT) outlook, performance, and financial condition. In this part, we will discuss more.

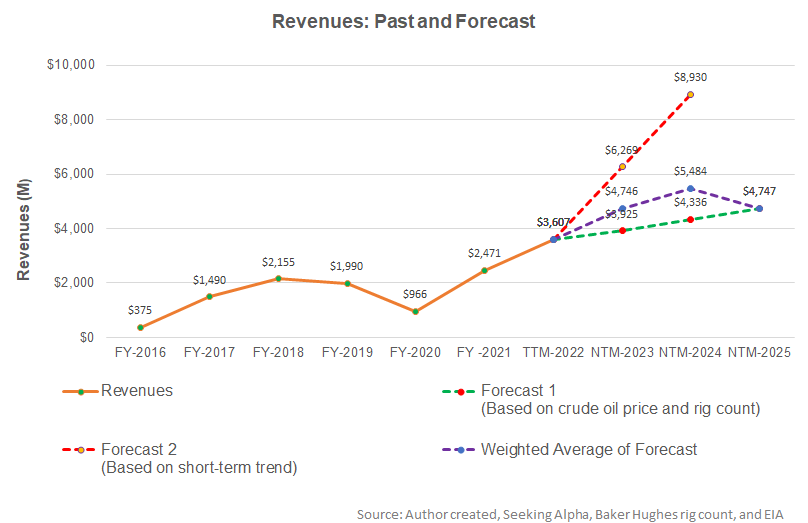

Linear Regression Based Revenue Forecast

Based on a regression equation between the crude oil price, rig count, and LBRT’s past seven-year revenues, its topline can increase sharply (by 32%) in the next 12 months (NTM 2023). The growth rate will decelerate to 16% in the following year and can decline in NTM 2025.

A regression model based on the forecast revenues suggests that the company’s EBITDA can increase by 90% in NTM 2023. In NTM 2024, the model indicates that the EBITDA growth rate will fall to 44%.

Relative Valuation And Target Price

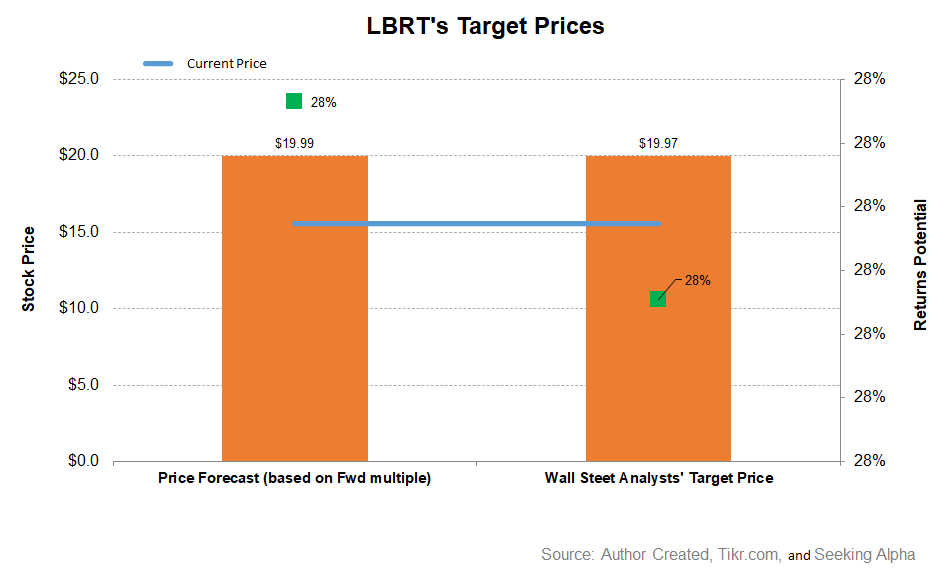

Here is an analysis of LBRT’s relative valuation using its forward EV/Revenue multiple. The returns potential (28% upside) using the forward EV/Revenue multiple (0.83x) is almost equal to the sell-side analysts’ expected returns from the stock.

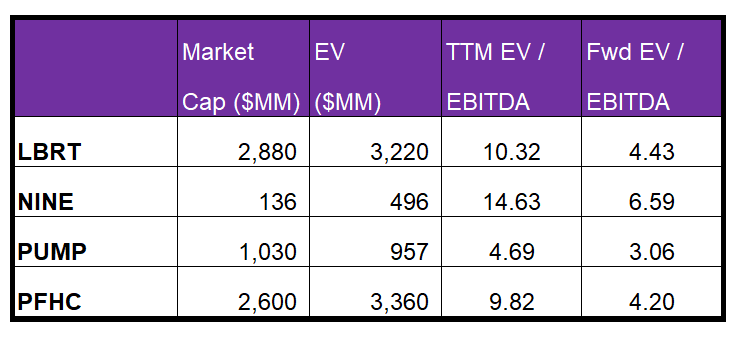

LBRT’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is steeper than its peers because its EBITDA would rise more sharply than its peers in the next four quarters. Its EV/EBITDA is higher than its peers’ (NINE, PUMP, and PFHC) average (9.7). So, I think the stock is reasonably valued versus its peers (with an EV/EBITDA of 10.3x) at this price level.

Analyst Rating

According to data provided by Seeking Alpha, nine sell-side analysts rated LBRT a “Buy” or “Strong Buy” in the past 90 days, while seven of them rated it a “Hold.” None of the sell-side analysts rated a “Sell.” The consensus target price is $20, which yields 28% returns at the current price.

What’s The Take On LBRT?

In a market where frac fleets and pressure pump supply remain tight, LBRT, with its suite of ESG-friendly frac fleets, will benefit from high demand due to its stringent emissions standards and fuel savings measures. Through its technology, scale, and vertical integration, the company has maintained a long-term relationship with its customers. It has recently introduced Sentinel logistics automation software. Its investment in Natron Energy would enhance its digiFrac fleets’ capability. We think contributions from crews deployed in Q3 can offset the typical adverse seasonality of Q4. Operating margin.

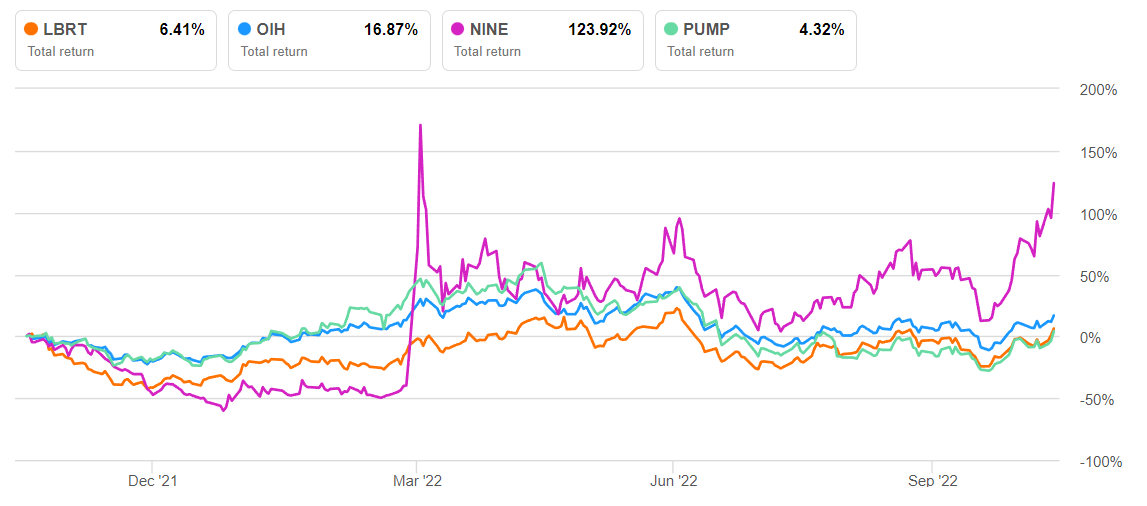

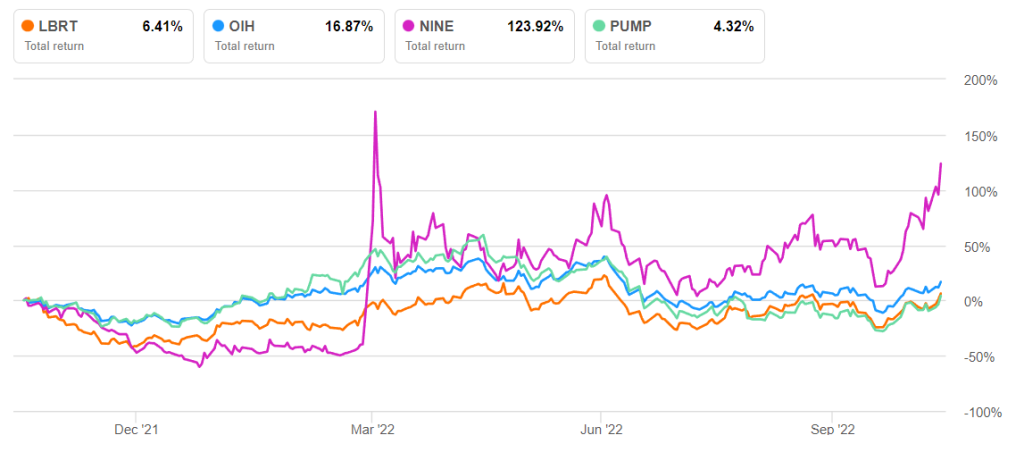

However, after adding six more frac fleets, Liberty’s frac fleet will remain unchanged in the near term. The COVID lockdowns in China may persist longer than expected, thus crippling the supply chain. Also, with a limping economy, heavy investment in new-age fleets may not be sustainable and may force it to defer capex to 2023. So, LBRT’s stock price underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. Nonetheless, its low leverage (debt-to-equity) will protect it from any possible pressure on cash flows. The stock is reasonably valued versus its peers at the current level. Investors should stay invested in this stock, expecting to improve returns in the medium-to-long term.