Strategy Analysis

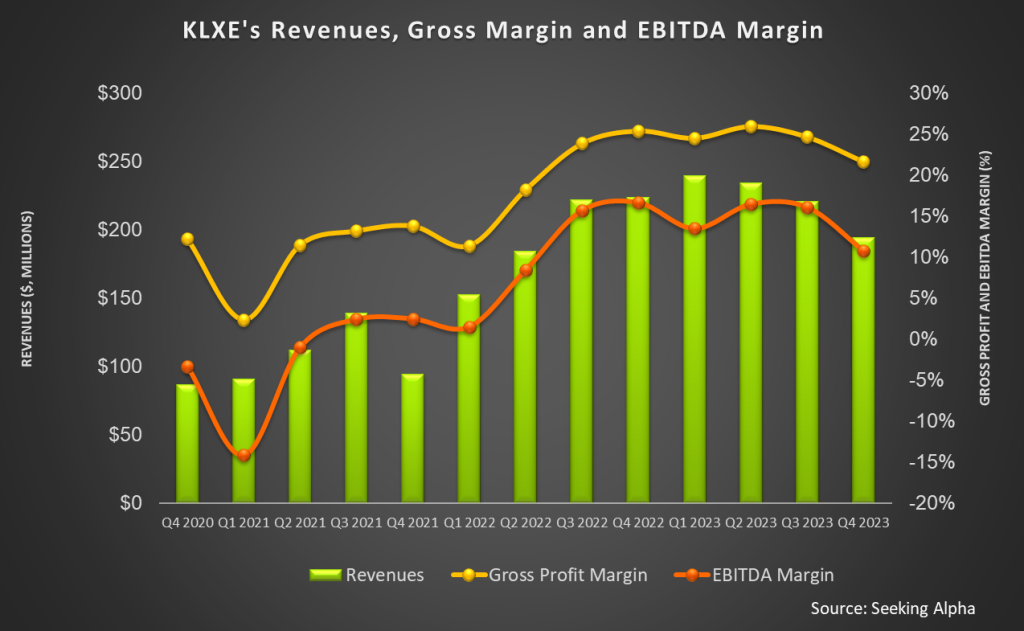

Our short article discussed our initial thoughts about KLX Energy Services’ (KLXE) Q4 2023 performance a few days ago. From Q3 to Q4, the company’s dissolvable plugs sales increased by 85%. Its fleet of large-diameter coiled tubing and SRT (downhole thru tubing) has also gone up. Higher demand for PhantM Dissolvable Plug and Oracle Smart Reach SRT will drive its sales in the near term.

The company also changed its customer strategy over the years. Although its customer base has shrunk significantly since 2019, it now focuses on dealing with large, active, and highly capitalized E&P operators. This is a part of its customer high-grading process. In FY2023, its top ten customers accounted for approximately 41% of its revenue. The strategy has been in focus following the recent spate of upstream energy industry consolidation, especially in the Permian Basin. The trend is expected to be a net positive for KLX because it typically enjoys “outsized relationships” with the acquirers.

The company will also be actively looking for M&As because its management believes a discrepancy exists in the consolidation rate between its customers and the service providers. While there has been a spate of consolidation for the energy operators, fewer OFS M&As have come to the fore. The lack of enthusiasm can be attributed to the depressed market multiples and highly fragmented competitive landscape for the OFS companies. In this scenario, KLXE believes it can derive value-creating transactions through acquisitions.

Q1 and FY2024 Outlook

Typical seasonality and adverse weather will likely affect KLXE’s Q1 performance, particularly in the Rockies, Mid-Con, and Texas. It can lose some revenue days. In Q1, safety standdowns would impact some customers’ operations in the Rockies. As a result, its Q1 revenues can decline compared to Q4 2023. As customers maintain their budgets, it will likely compensate for the revenue loss. KLXE will optimize utilization and pricing to drive margins and free cash flow. It expects to derive the benefits of a solid onshore activity in 2H 2024.

After a slower start in Q1, KLXE’s performance can get increasingly stronger through Q2 and Q3. However, modest seasonality can affect its Q4 revenues, but the impact should be less pronounced than in 2023 because gas-directed activity should begin to improve. In aggregate, in FY2024, the company expects revenue to be “in line with or slightly above” 2H 2023.

Q4 Performance Drivers

Our short article discussed KLXE’s year-over-year topline and margin by geography in Q4 2023. In Q4, seasonal slowdowns, customers’ budget exhaustion, and capital discipline led to lower revenue and EBITDA margin. On the other hand, revenues from pressure pumping and downhole production services increased following previous frac contracts and continued adoption of the PhantM Dissolvable Plug, as discussed above.

In Northeast/Mid-Con, KLXE continues to run two frac spreads, one operating under a contract with a top-tier operator. Its pricing and utilization improved for the completion and production intervention service lines.

Cash Flows And Debt

KLXE’s cash flow from operations turned significantly positive in FY2023 compared to a negative cash flow a year ago. Although capex increased, its FCF also turned positive. The cash flow improvement reflects higher revenues and improved working capital management. Its FY2024 capex budget falls below the FY2023 capex by 8%.

Most of the capex would support ongoing operations, and the remaining would be used for reactivation equipment related to rentals, frac rentals, and coiled tubing. Although it reduced net debt by 24% from FY2023, as of December 31, 2023, KLXE’s leverage (debt-to-equity) was high, at 7.3x, due to low and deteriorated shareholders’ equity. As of that date, the company’s liquidity was $154 million.

Relative Valuation

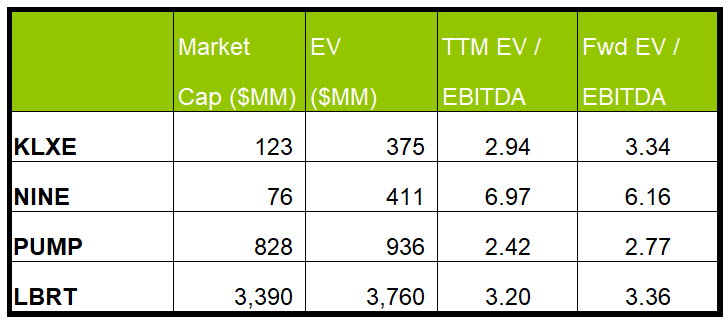

KLXE is currently trading at an EV/EBITDA multiple of 2.9x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is higher (3.3x).

KLXE’s forward EV/EBITDA multiple expansion versus the current EV/EBITDA is much steeper than its peers because its EBITDA is expected to decrease more sharply than its peers in the next year. This typically results in a lower EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple is lower than its peers’ (NINE, NEX, and LBRT) average. So, the stock is reasonably valued versus its peers.

Final Commentary

After Q4, higher demand for PhantM Dissolvable Plug and Oracle Smart Reach SRT will push KLXE’s topline in 2024. It continues to run two frac spreads while pricing and utilization improved for the completion and production intervention service lines. However, seasonal slowdowns, customers’ budget exhaustion, and operators’ capital discipline have recently trimmed their growth. The upstream energy consolidations have shrunk OFS companies’ aggregate end market size. In this environment, KLXE’s high customer rating can restrict the adverse effects and lead to premium pricing for its efficient product lines.

The company expects the situation to improve sequentially from Q2 through Q4 as natural gas activity picks up by the end of the year. Its cash flows improved significantly in FY2023. However, the company’s low shareholders’ equity will continue to make its balance sheet inherently risky. The stock is reasonably valued compared to its peers.