Market Outlook

We have already discussed Liberty Energy’s (LBRT) Q4 2024 financial performance in our recent article. Here is an outline of its industry outlook. LBRT anticipates geopolitical uncertainties, lower Chinese economic growth, and sustained OPEC+ production plans to challenge energy pricing. But so far, the energy operators’ capex plans have not indicated they can fall lower than already stated.

On top of that, LNG export capacity expansion can boost natural gas demand, led by multiyear increase in North American power consumption. As I discussed in my previous articles, LBRT has a competitive advantage in e-fracking as it transitions fleet to next-generation digiTechnologies. In January, LBRT announced the latest development for its digiPrime platform with its partner Cummins. The engine enhances the digiFleet offering by combining high fuel efficiency with the ability to manage transient load and precision rate control.

Frac Strategy

The frac market continues to stay under pressure. Industry activity has been on a slope since 2023, resulting in frac markets reaching a trough by 2024-end. With this, the year-end slowdown can slowly turn into increased fracking activity as crude oil producers look to maintain production. Its recent deployment of digiPrime frac spreads it achieved 96% under the normal dedicated fleet utilization. In FY2025, the lateral footage completed is expected to remain unchanged compared to 2024.

Frac pricing is headed north in early 2025. LBRT’s management believes that fleet idling, attrition, and cannibalization of aging equipment will likely accelerate by 2026 as many Tier 2 equipment reaches their end of life. Lower pricing will largely impact conventional frac spreads, although the outlook for next-generation higher-quality fleets remains strong. The current trend points to an expansion in fleet sizes due to increased horsepower requirements for higher-intensity fracs. As the demand-supply balance improves, frac activity can rise and support better pricing by the end of 2025.

Key Investment – Power

Since 2022, Liberty has invested in geothermal, nuclear, battery, power, generation technologies, and the Australian Beetaloo basin assets. Increases in mining, electrification, and other commercial and industrial applications will likely increase power demand in the medium term. This will support Liberty’s power generation business growth outside the oilfield. It can also increase requirements for power infrastructure solutions, for which Liberty has a strong platform. With an eye on higher demand for power generation and distribution, LBRT has initiated its distributed energy operation.

Since 2011, it has deployed nearly $5 billion to build a completion business that now operates and maintains rotating heavy equipment in remote environments across North America. This delivery mechanism for electrons fits specific applications like merchant power, data centers, commercial EV charging stations, and microgrids. Having already deployed 130 megawatts for digiFleet applications, it plans to generate an incremental 400 megawatts of power by 2026.

Q4 Performance And Balance Sheet

LBRT’s revenues decreased by 17% quarter-over-quarter in Q3, while its adjusted EBITDA declined by 37%. Read more about LBRT’s performance in our short article. The company’s debt-to-equity, however, increased to 0.10x as of December 31, 2024. During Q4, it repurchased 1.0% of its outstanding shares and raised its quarterly dividend by 14% to $0.08 per share.

Relative Valuation

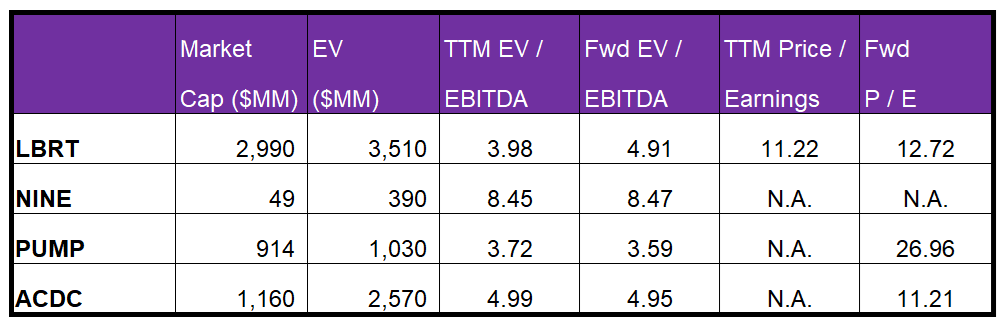

Liberty is currently trading at an EV/EBITDA multiple of ~4x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is higher. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 15.8x.

LBRT’s forward EV/EBITDA multiple expansion versus the current EV/EBITDA is higher than its peers because the company’s EBITDA is expected to decline more sharply than its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is lower than its peers’ (NINE, PUMP, and ACDC) average of 5.7x. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

In early 2025, LBRT will continue to deal with the industry’s ongoing challenges, namely the adverse geopolitical environment, lower Chinese economic growth, and OPEC’s crude oil production plans. However, it looks confident of pulling off a turnaround by the end of the year based on natural gas demand and a multiyear increase in North American power consumption. It will continue to focus on e-fracking, particularly in the next-generation digiTechnologies. Frac pricing will stay depressed in early 2025, though as many Tier 2 equipment reaches the end of life. This can affect the company’s profitability until the demand-supply balance is replenished.

LBRT has taken a keen interest in the power generation business growth outside the oilfield. It will serve the fast-growing sectors like merchant power, data centers, commercial EV charging stations, and microgrids. Despite that, it continued to generate return capital to shareholders and raised its quarterly dividend in Q4. Compared to its peers, the stock is reasonably valued, with a negative bias.

Premium/Monthly

————————————————————————————————————-