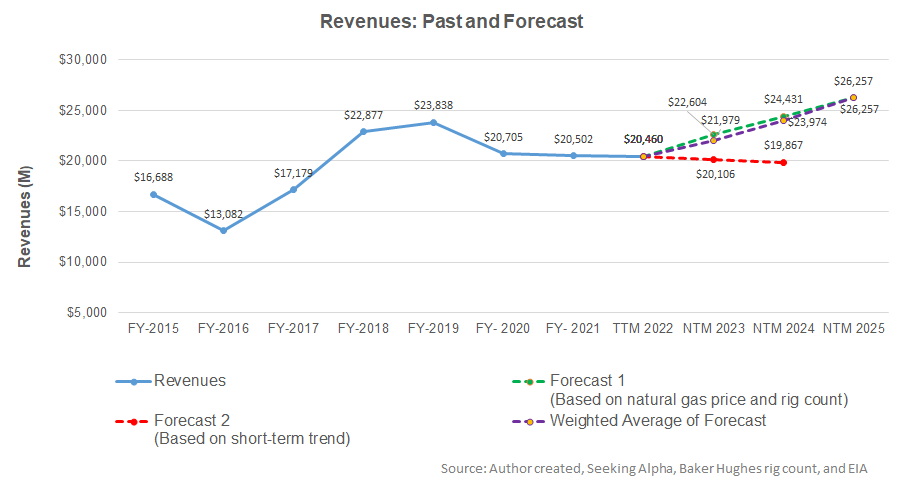

- Revenue estimates suggest a steadily increasing trend in the next three years

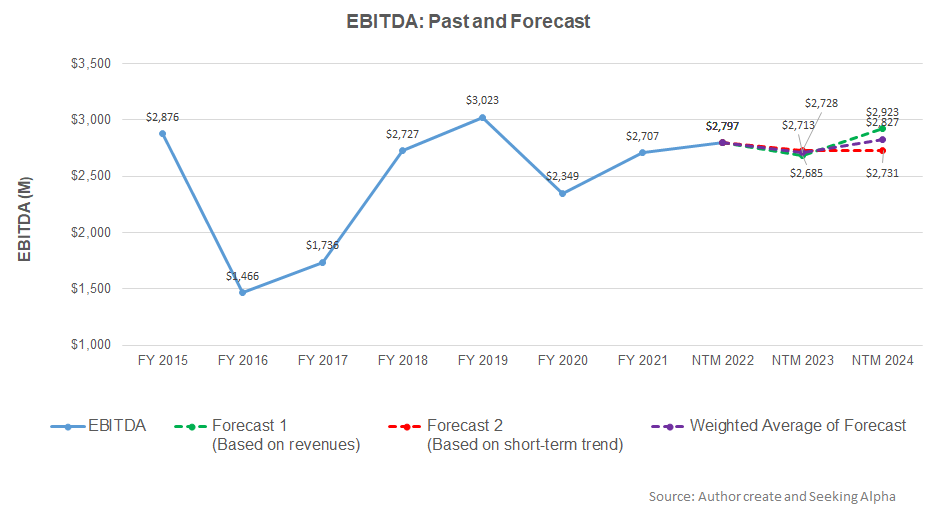

- EBITDA can improve in the next year but can decline in NTM 2024

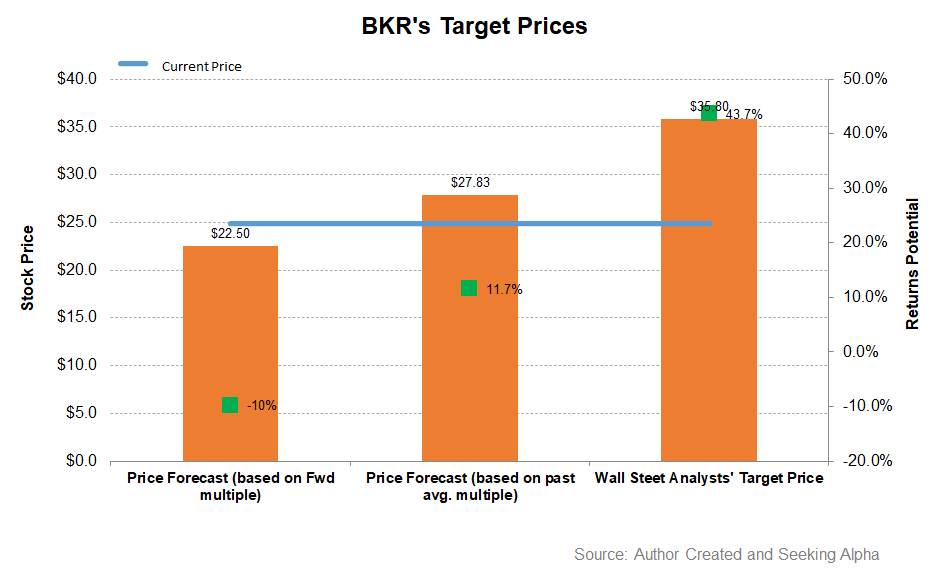

- The stock is overvalued at the current level

Part 1 of this article discussed Baker Hughes’s (BKR) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Forecast

Based on a regression equation among the natural gas price, global rig count, and BKR’s reported revenues for the past seven years and the previous eight-quarters, revenues will increase steadily in the next three years.

Based on the regression model using the average forecast revenues, the company’s EBITDA is expected to decrease moderately in the next 12 months (or NTM 2023). However, in NTM 2024, it can increase moderately.

Target Price And Relative Valuation

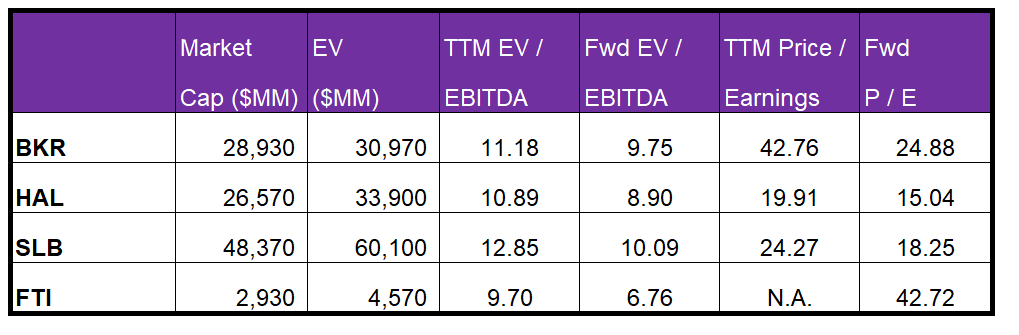

Returns potential using BKR’s forward EV/EBITDA multiple (9.75x) is lower (10% downside) compared to returns potential using the past average multiple (12% upside). The Wall Street analysts have higher return expectations (44% upside).

Baker Hughes is currently trading at an EV-to-adjusted EBITDA multiple of 11.2x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 9.7x. The current multiple is lower than the past five-year average EV/EBITDA multiple of 11.7x.

BKR’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is less steep than peers because the company’s EBITDA is expected to increase less sharply in the next four quarters. This would typically result in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple aligns with its peers’ (HAL, SLB, and FTI) average. So, the stock is overvalued versus its peers.

Analyst Rating

According to data provided by Seeking Alpha, 20 sell-side analysts rated BKR a “Buy” or “Strong Buy” in July, while five of them rated it a “Hold.” Only one of the sell-side analysts rated a “Sell.” The consensus target price is $35.8, which yields 44% returns at the current price.

What’s The Take On BKR?

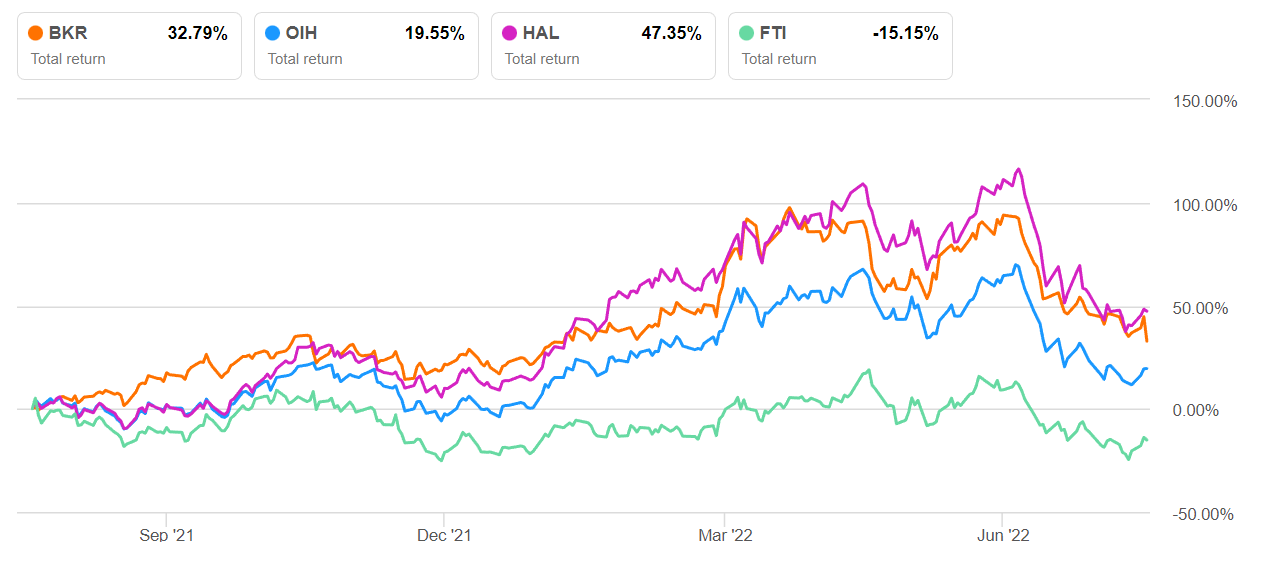

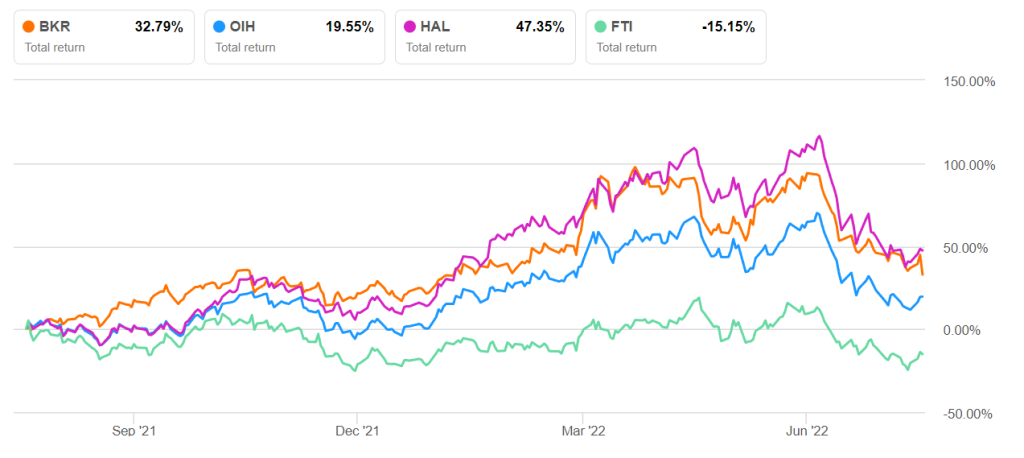

A rise in significant LNG projects and increased contracting activity underline the natural gas business’s long-term prospects. Baker Hughes will expand into industrial energy technology, look for optimizing operations, and find additional synergies between its inter-related segments. On the offshore, securing several large deepwater contracts across the Americas (Brazil) and the Middle East and stable activity in North America onshore will drive revenues. Aided by these growth drivers, the stock outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

While natural gas’s role as the medium to the long-term driver has continued to be the mainstay of Baker Hughes’s impressive run, the company will face uncertain times in the short term. Over the past few months, the company has suspended all equipment and service contracts in Russia. As a result, cost under absorption can adversely impact the margin in the near term. Also, the sharp fall in order backlog in the TPS segment can thwart the revenue growth potential in 2022. BRR has low leverage and can withstand the pressure of cash flows. The management also expects free cash flow conversion from adjusted EBITDA to decline in 2022 due to lower cash generation in Russia. The stock is relatively overvalued at this level. Nonetheless, investors can hold the stock for steady returns in the long term.