- The international energy markets will be Schlumberger’s primary short-term driver, driven by capacity expansion projects in the Middle East and offshore activities.

- North American onshore activity can see headwinds despite the overall growth in Q4.

- Its long-term growth opportunities lie in developing the core operations, digital, and new energy businesses

- While free cash flow turned positive in 9M 2022, high leverage can still be of some concern.

Industry Drivers And New Growth Opportunities

Our previous Schlumberger (SLB) article discussed how its management turned slightly conservative. However, it continues to trust that the international markets will go through an up-cycle while expected to see robust short-cycle activity in North America. After Q3, SLB strengthened its view regarding the mid-tier up-cycle. After a year of underinvestment, a significant push is required to re-balance the market. Despite the global economic growth slowdown, the energy sector holds its forte. The energy demand looks to stay robust in the near term, while the typical winter seasonality can marginally take away the sheen. The supply landscape remains tight, with OPEC dragging down production. Limited spare global capacity is another factor to consider here.

The company is investing handsomely in the clean energy business. Here, it funds and develops a new capability, including hydrogen and CCUS (carbon capturing). In October, it entered into an agreement with RTI International to accelerate the industrialization of non-aqueous solvent technology used in absorption-based carbon capture. It has also invested in ZEG Power which develops technology for clean hydrogen production from natural gas. SLB will strengthen its position by making further investments in these technologies.

The Q4 And Long Term Outlook

SLB’s management expects international markets will be driven by a capacity expansion project in the Middle East and offshore activities. However, the adverse effects of seasonality would cause activities in the Northern Hemisphere would drag the result. Also, the North American onshore activity can dial down in Q4. Nonetheless, with 81% of revenues generated from international operations, SLB’s management expects to see “mid-20s” year-over-year revenue growth, while the EBITDA margin can also expand. The updated guidance surpasses the company’s previous guidance.

Over the medium-to-long term, SLB sees growth opportunities in its core operations as well as digital and new energy businesses. An increased need for energy security in an uncertain geopolitical backdrop and the ongoing energy transition would justify its investments in clean energy technology development. So, various technology-led opportunities will put Schlumberger at an advantage over many of its peers, particularly in digital transformation, industrial decarbonization, and new energy systems.

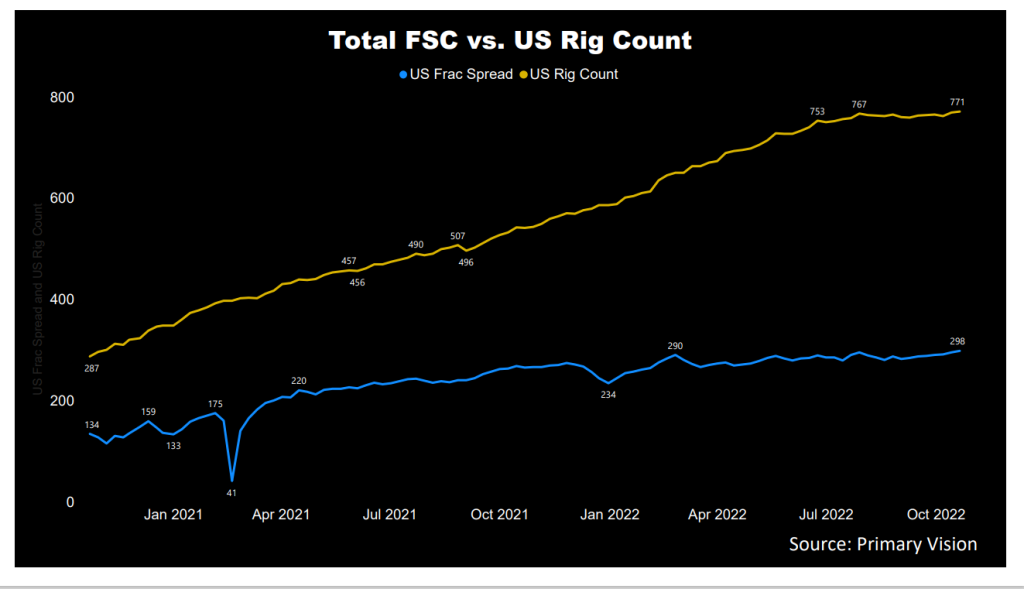

Frac Spread Count

According to Primary Vision’s forecast, the frac spread count (or FSC) reached 298 by the third week of October and has increased by 27% since the end of 2021. A rising frac count is positive for SLB’s growth. Over the past month, we saw ten frac fleet additions in the US. In 2022, Schlumberger sold a majority stake in its Permian frac sand business to Liberty Oilfield Services (LBRT). Please read our analysis on LBRT here.

Industry Indicators Gain Strength

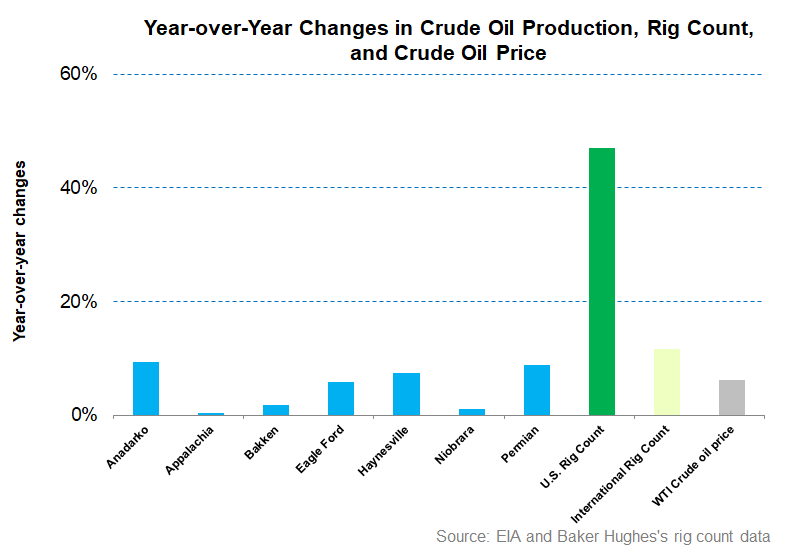

In the past year until September 2022, the key US unconventional Basins, on average, saw a 5% rise in tight oil production. However, the US rig count recovery (47% up) significantly outperformed the production growth. The EIA expects OPEC crude oil production will fall to 28.6 million barrels per day in Q1 2023. According to the EIA, crude oil prices can increase by ~9% in Q4 compared to the current level. By 2023, however, it can rise further (2% up) due to the petroleum supply disruptions and slow crude oil production growth.

From Q2 to Q3, SLB’s revenue share from international operations inflated to 79% from 77%. The North American area grew less (0.4% up quarter-over-quarter) than the others. Europe/CIS/Africa saw the most remarkable sequential recovery (21% up), followed by Latin America (13.5% up). A global growth cycle combined with an offshore market recovery led to the company’s topline increase in Q3.

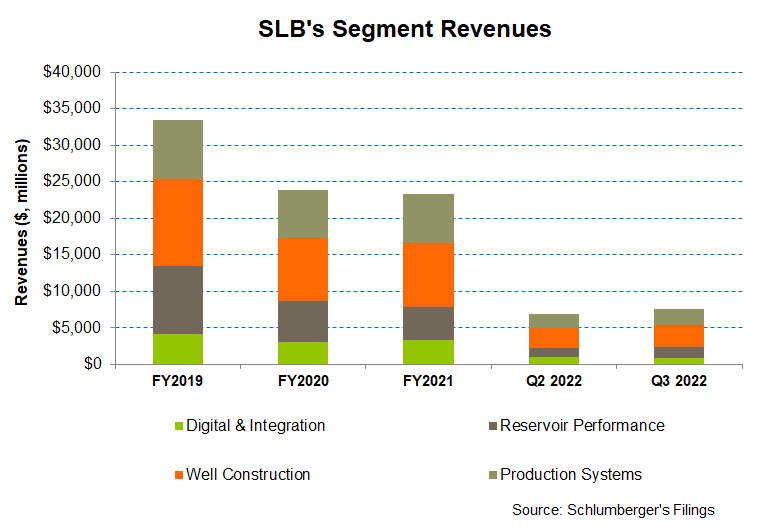

The Key Segment Drivers In Q3

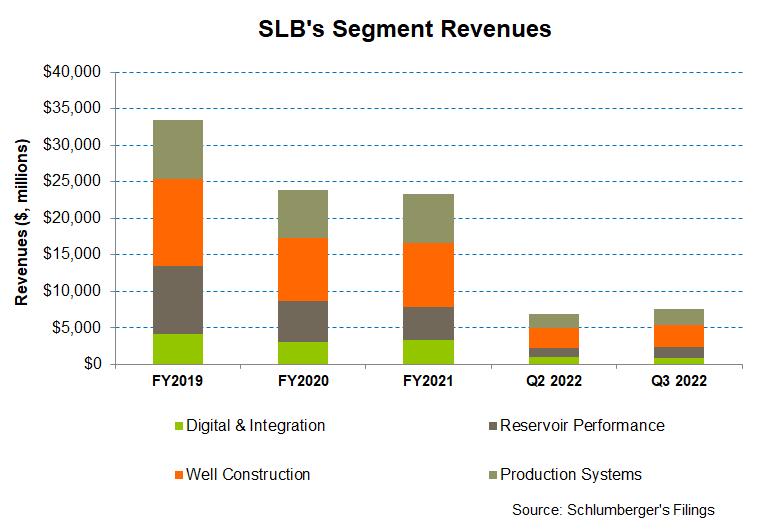

In Q3 2022, Schlumberger’s Digital & Integration revenue segment revenues decreased by 6% compared to Q2 because of higher exploration data transfer fees. The segment operating income, too, pared down by 20%.

Quarter-over-quarter, SLB’s Well Construction segment revenue increased the most (by 15%) in Q3 due to improved pricing and strong activity growth, particularly in offshore and international markets. It also pushed the operating income margin up by ~400 basis points. Revenue growth in the Production Systems segment was also impressive (14% up) in Q3, following higher backlog conversions as supply chain logistics eased up.

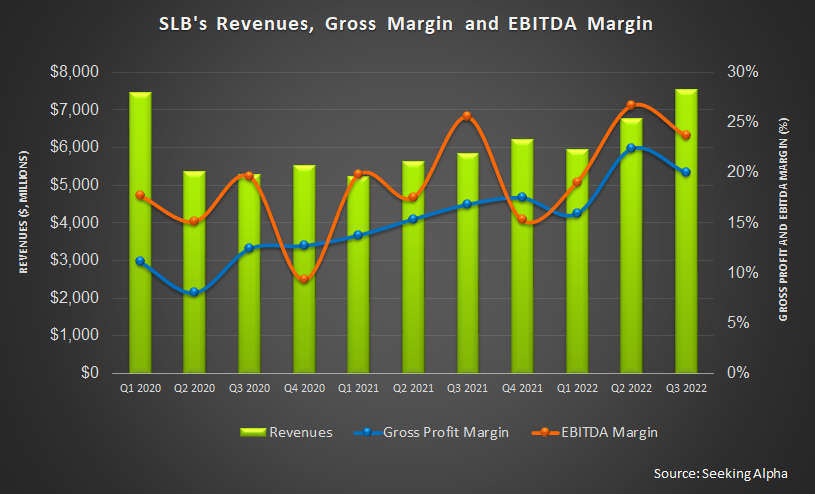

In Q3, SLB recorded an adjusted EPS of $0.63, or a 26% increase, versus a quarter ago, which was the highest quarterly adjusted EPS since Q4 2015. The company’s operating margin has been among the best for the past two quarters since FY2015.

FCF and Capex In FY2022

In 9M 2022, SLB’s free cash flow (or FCF) turned positive but was nearly half of its 9M 2021 FCF. Lower cash flow from operations (or CFO) reduced FCF. Although revenues increased in this period, a higher working capital requirement caused the CFO to decline. Capex, too, was raised in the past year. The management estimates the cash flow trend to accelerate in Q4. So, FCF can improve in the short term. FY2022 expects capital investments to be ~$2.2 billion, or 38% higher than FY2021.

Higher earnings and FCF can help expedite the balance sheet deleverage process. The company’s debt-to-equity is 0.76x, which was an improvement compared to a quarter ago. However, it is higher than the peers’ (HAL, BKR, and FTI) average of 0.70x.

Dividend And Dividend Yield

Schlumberger maintained its annual dividend at $0.70 per share, with a 1.39% forward dividend yield. In comparison, Halliburton (HAL) pays a yearly dividend of $0.48, which amounts to a forward dividend yield of 1.42%.

Learn about SLB’s revenue and EBITDA estimates, relative valuation, and target price in Part 2 of the article.