- In the traditional energy business, NOV focuses on the downhole energy business to improve visibility for precision well placement.

- Increased opportunities in well safety performance and reducing greenhouse gas emissions also drive its business.

- Its near-term drivers are the rising demand in the Middle East, reactivation and recertification projects, pressure control upgrades, and automation projects.

- Although cash flows are negative, it expects to turn it around in Q4.

Analyzing NOV’s Strategies

In the energy services market, NOV’s management will increase its focus on the efficient development of new fields. Outside the purview of strict conventional markets, it will pursue opportunities in safety performance and reducing greenhouse gas emissions. Digital technology is a significant area of interest. For example, the downhole energy business considers rotary steerable technology to improve visibility for precision well placement. Read our previous article in NOV to know more.

The company’s technology innovation includes eVolve IntelliServ wired drill pipe, allowing operators to have high-speed data flowing. Its KAIZEN intelligent drilling optimizer and NOVOS Automation help optimize well placement, reservoir development, rig efficiency, and crew safety. Its NOVOS drilling system, paired with MPowerD-managed pressure drilling, helps maintain downhole pressure control in challenging environments. So, downhole engineering has become a prominent feature of NOV’s technological ingenuity.

Industry Activity

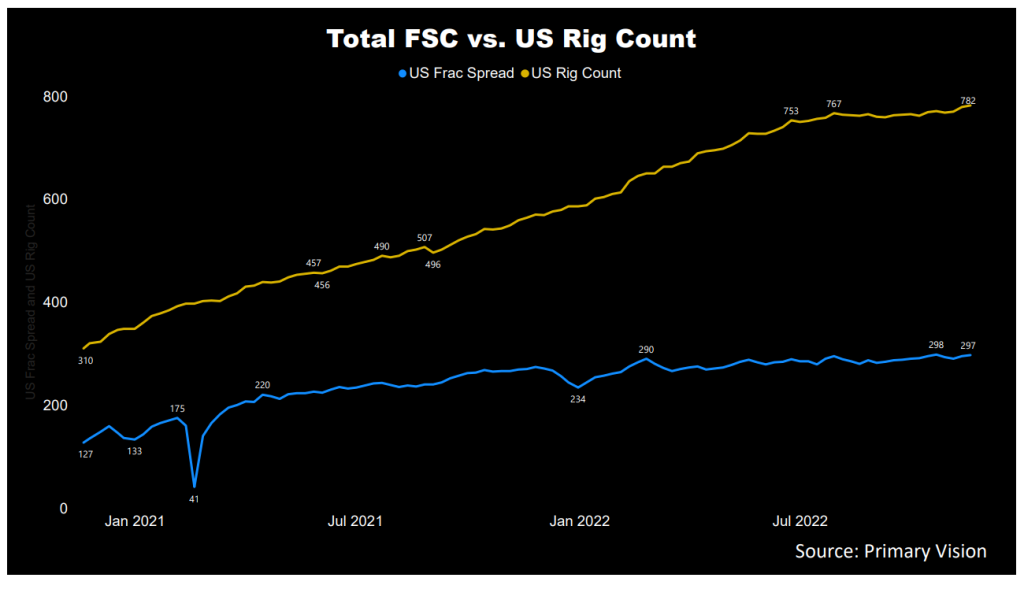

In North America, crew and equipment availability constraint translates into higher rig rates and oilfield service pricing. In the Middle East, Asia, Africa, and Latin America, nationalized oil companies, and sovereign wealth funds are now gearing up after taking a cue from the crude oil price recovery in 2022. The US rig count has remained steady since Q3-end, although the crude oil price has increased during this period. As estimated by Primary Vision, the frac spread count (or FSC) reached 297 by the second week of November and has gone up by 27% since the start of 2022.

The Near-Term Challenges And Opportunities

Among the critical challenges the company faces, high input costs and low book-to-bill ratio are prominent. In Q3, NOV’s book-to-bill ratio fell below 1x, due primarily to a declining backlog in the Completion & Production Solutions and Rig Technologies segments, due mainly to a lower backlog for capital equipment. Delaying capital equipment orders in the US and European oilfield companies will remain a concern in the near term.

Since the 2020 oil market downturn, the E&Ps have been focused more on returning cash to shareholders than reinvesting in the business. Given the capital constraints from the institutional lenders, the oilfield services companies will mostly reply on cash flows from operations for funding new investments. The supply side is also ridden with the energy transition plan without much relevance to reality. Too much importance on clean and alternative energy has been counterproductive to the energy sector, which, in turn, has made long-term investment in legacy energy projects uncertain.

On top of that, the supply chain challenges pulverized the investment decisions. Internationally, the oilfield service providers saw limited growth in the Middle East because the market has remained oversupplied in their long-term contracts. In the Middle East, the NOCs are looking to order more efficient equipment, which should benefit NOV. Therefore, the company’s management expects North America and European energy companies to increase their investment in response to the crude oil price recovery in 2022.

The Q4 Outlook

The Wellbore Technologies segment will see demand rising in the Eastern Hemisphere markets, particularly in the Middle East. North American drilling activity moderation, however, can impede the growth trajectory. The management expects revenues in this segment to grow by 2%-6%, while the EBITDA margin can clock in the 30% range.

The Completion & Production Solutions will benefit from the increased booking, including 67,500 horsepower of new pressure pumping equipment and rebuilding an additional 30,000 horsepower of pumping units. Other orders include injectors, pumps, nitrogen units, and other support equipment. On top of that, demand for coiled tubing equipment picks up in North America. Despite that, the revenue growth in Q4 can stay flat as a few projects were pulled forward while the supply chain issues continued. These factors can also contract EBITDA margins by 50-100 basis points.

The Rig Technologies segment can see revenue grow between 5% and 10% sequentially in Q4. The segment EBITDA margin can also expand. An increased quoting activity related to reactivation and recertification projects, pressure control upgrades, and automation projects will lead to the topline growth. Also, orders for a new wind vessel will likely take place in the near term, which can add to the topline growth and diversification.

Q3 2022 Segment Performance Drivers

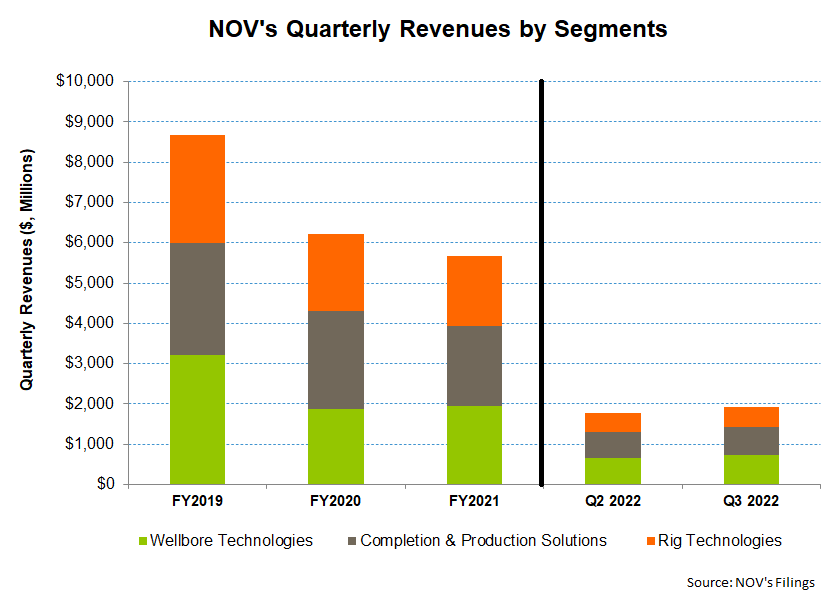

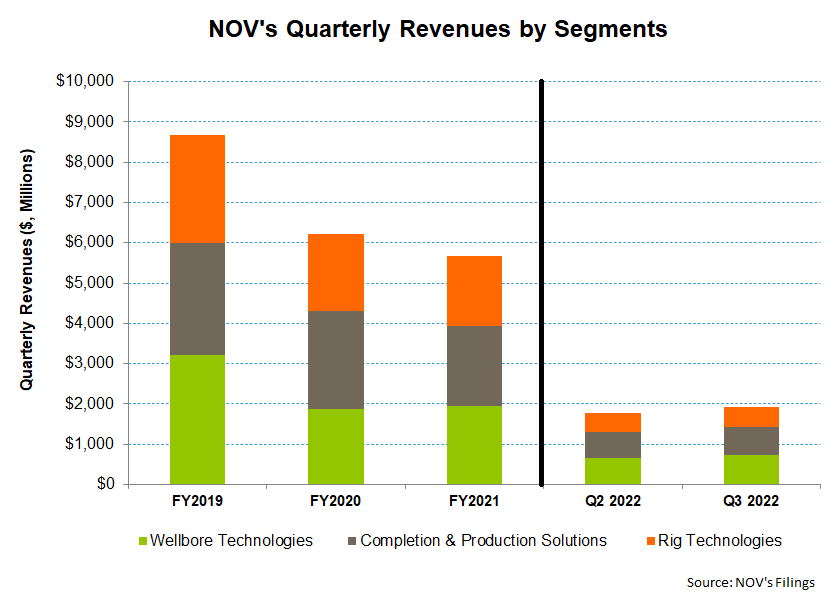

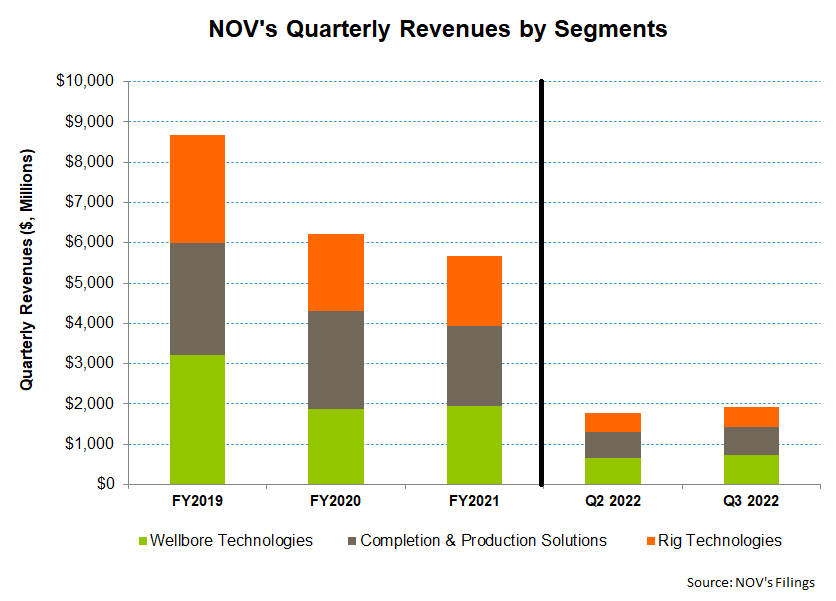

In Q3, NOV’s revenues increased by 9% compared to Q2 2022. The Wellbore Technologies segment, which is its largest segment (accounting for 38% of Q3 revenues), saw revenues rise by 11% quarter-over-quarter. The segment also saw operating income fall by 9% during this period. In this segment, the downhole business saw impressive topline growth. It overcame the supply chain challenges by using certain steel grades in the high-spec products, especially in the proprietary tools. The demand for drilling tools increased in the Middle East, although activity in North America slowed down in Q3.

Revenues in the Completion & Production Solutions segment increased by 7% quarter-over-quarter in Q3, while the operating profit increased (5% up). In this segment, improved execution on offshore projects led to revenue growth, although an extended lead time for new build deliveries took a toll on the segment’s performance.

The Rig Technologies segment saw 11% topline growth in Q3 over Q2. However, the segment’s operating profit declined sharply (by 29%). During Q, it saw an improvement in the aftermarket business and rapid progress on offshore wind and Saudi rig projects. The day rate in the US will likely reach $40,000 as many operators may start reinvesting in their existing asset bases. However, Rates were much lower in Q3, contributing to the lower profit level.

Dividend And Dividend Yield

NOV pays an annual dividend of $0.20 per share at the current rate. It translates to a 0.89% forward dividend yield. Schlumberger (SLB) pays a yearly dividend of $0.70, which equals a forward dividend yield of 1.35%.

Negative Cash Flows; Strong Liquidity

As of September 30, 2022, NOV’s liquidity (cash and including revolving credit facility) was ~$3.0 billion. The company’s leverage (debt-to-equity) was 0.35x, slightly higher than its peers’ (CHX, FTI, WHD) average.

NOV’s cash flow from operations (or CFO) was steeply negative in 9M 2022, strikingly contrasting to the positive CFO a year ago. Although revenues increased in the past year, a rise in receivables and inventories and lower accounts payable contributed to the fall in CFO. As a result, free cash flow was sharply negative. In Q2, the management expects to generate $100 million-$200 million in free cash flow, which means its free cash flow conversion will improve significantly in Q4.

Learn about NOV’s revenue and EBITDA estimates, relative valuation, and target price in Part 2 of the article.