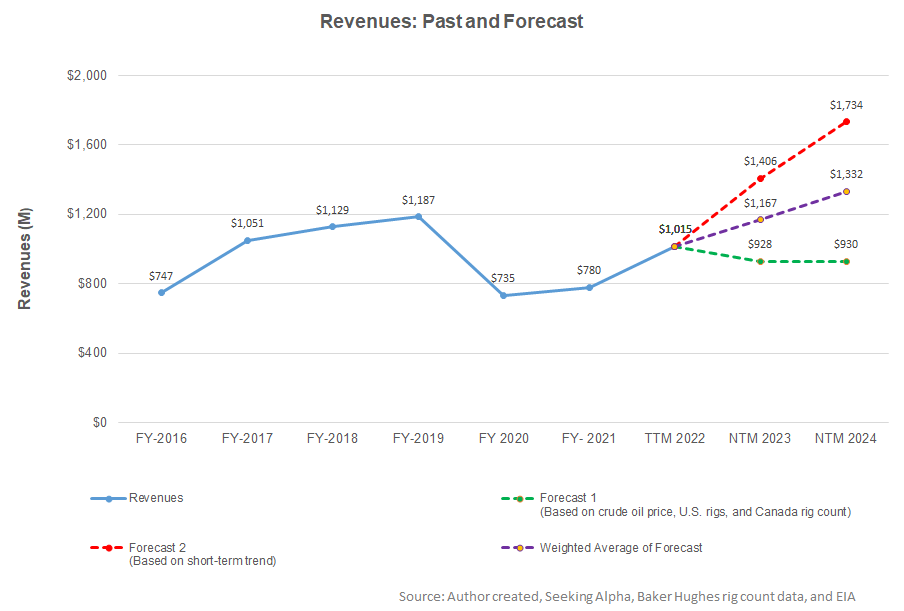

- Our regression estimates suggest a steady revenue growth in NTM 2023 and NTM 2024.

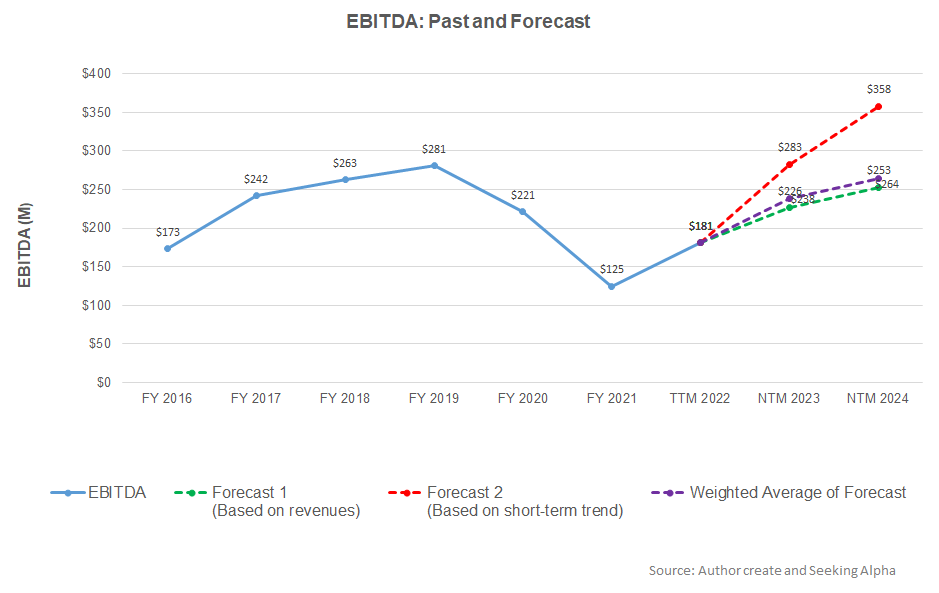

- The EBITDA growth rate is quite steep in NTM 2023 but may decelerate in NTM 2024.

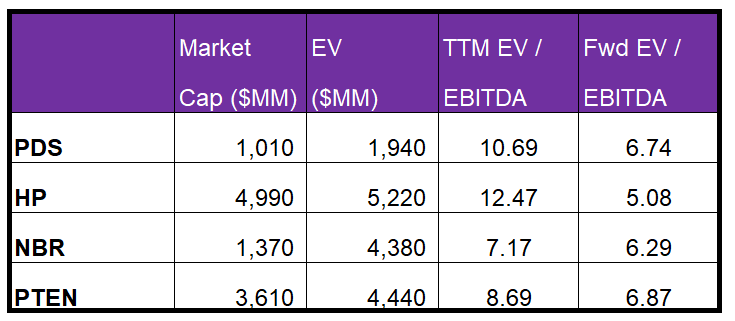

- The relative valuation suggests the stock is reasonably valued, although our regression model suggests a potential downside at this level.

Part 1 of this article discussed Precision Drilling Corporation’s (PDS) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Forecast

Based on a regression equation on the relationship between the crude oil price, the US rig count, the Canadian rig count, and PDS’s reported revenues for the past seven years and the previous four quarters, I expect revenues to increase by 15% in the next 12 months (or NTM 2023) and 14% in NTM 2024 (sequentially).

Based on a simple regression model using the average forecast revenues, the company’s EBITDA can improve by 31% and 11% in NTM 2023 and NTM 2024, respectively.

Relative Valuation Analysis

PDS’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is marginally steeper than its peers because its EBITDA is expected to increase slightly more sharply than its peers in the next four quarters. This typically reflects a marginally higher EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple (10.7x) is higher than its peers’ (HP, NBR, and PTEN) average of 9.4x. So, the stock is reasonably valued at the current level.

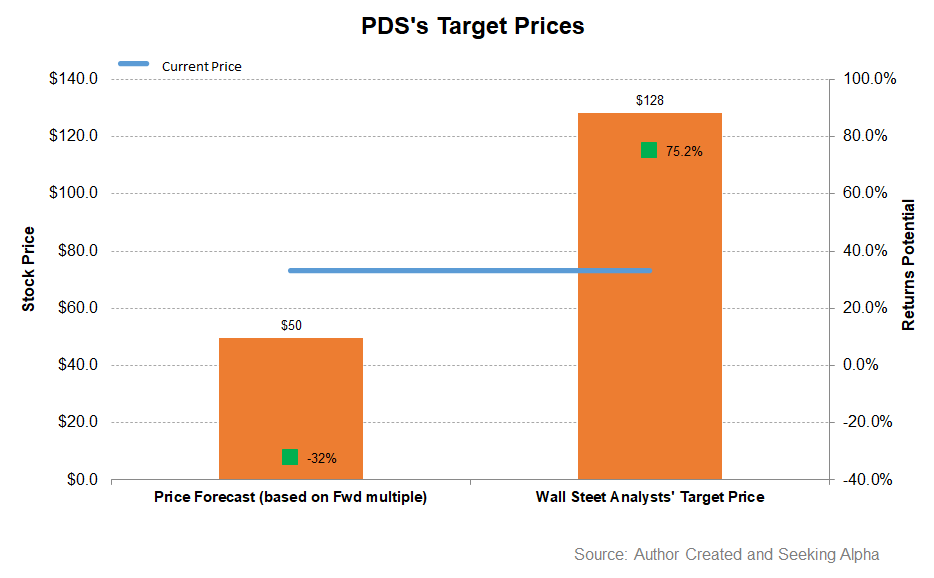

EV has been calculated using PDS’s EV/EBITDA multiple. The returns potential using the forward EV/EBITDA multiple (8.2x), given our regression model-derived EBITDA, is lower (32% downside) than sell-side analysts’ expected returns (75% upside) from the stock.

Analyst Rating

The sell-side analysts’ target price for PDS is $128.2, which, at the current price, has a return potential of 75%. Out of the 12 sell-side analysts rating PDS, ten rates it a “buy” or a “strong buy,” while two rate it a “Hold.” None rates it a “sell.”

What’s The Take On PDS?

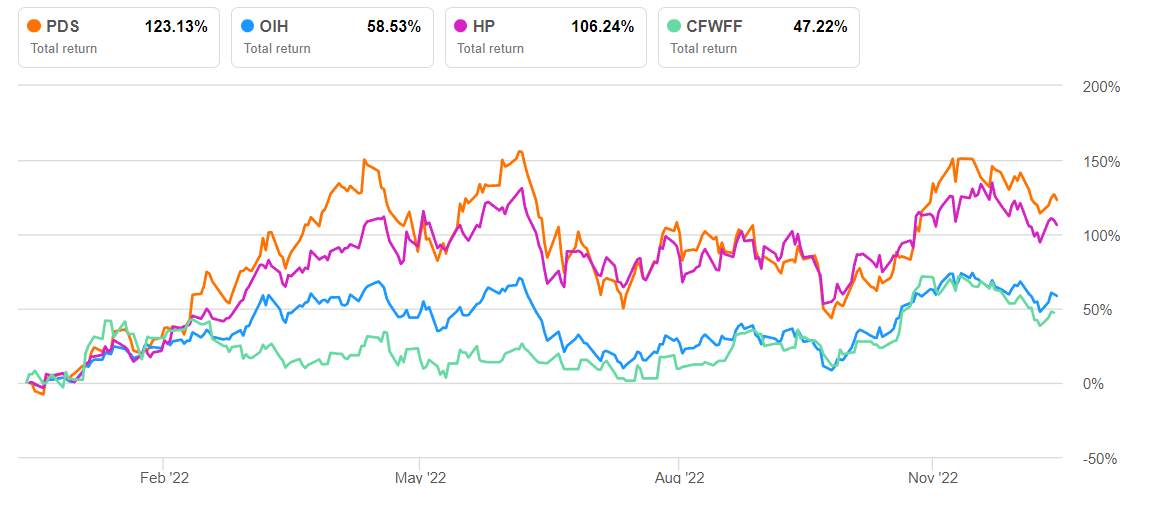

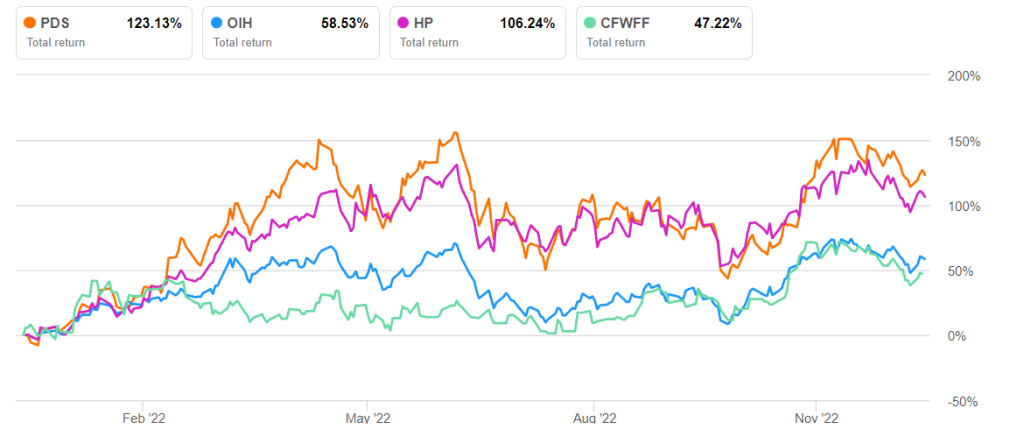

As drilling activity in Canada rises, the leading-edge rates are trending up. PDS’s Superior Triple rigs increasingly adopt Alpha Automation and Alpha Apps, which command a premium over the industry rate. In Kuwait, it has recently received four contracts, including the reactivation of two large rigs. The positive impact of technologies, increased efficiency, and higher fixed cost absorption mitigated higher operating costs over the past years, leading to higher operating margins in 20233. As the operating margin improved, the stock outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

However, the continued labor and supply inflation and higher maintenance costs in the oilfield industry have increased PDS’s operating costs. In 9M 2023, PDS’s free cash flows turned negative, which, coupled with a leveraged balance sheet, can raise concerns. A robust liquidity dis-spell the worries, though. The stock is relatively undervalued at this level.