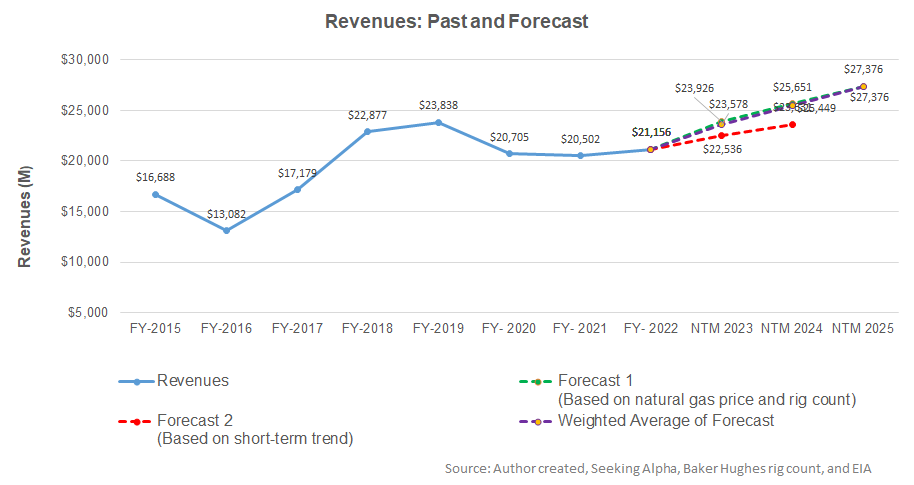

- Our regression model suggests a decelerating revenue trend in the next two years.

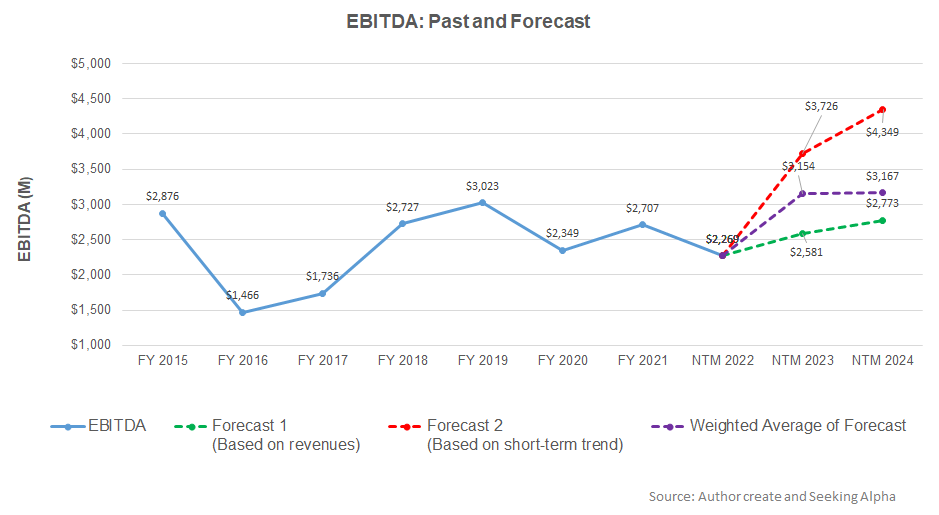

- EBITDA can increase sharply in NTM 2023 but can stagnate in NTM 2024.

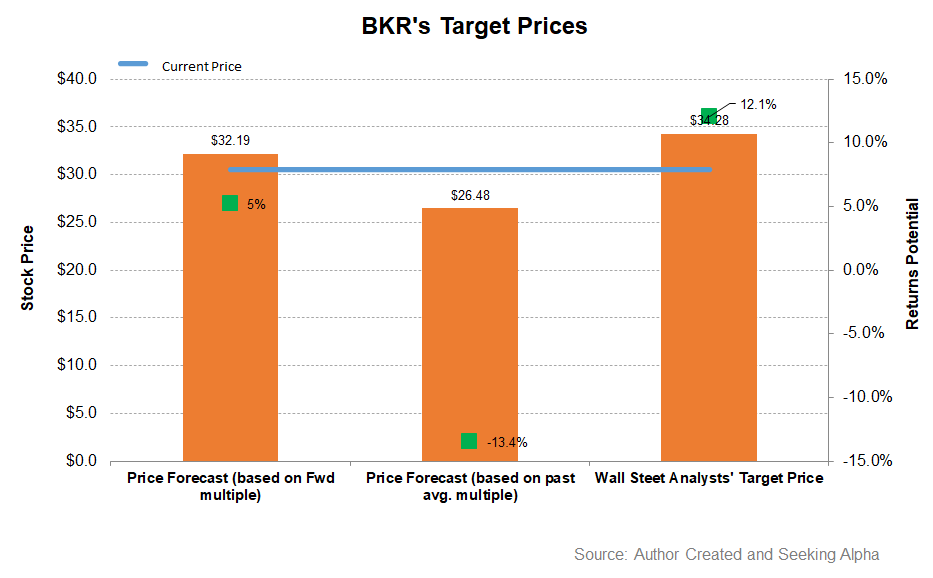

- The stock is mildly overvalued at the current level.

Part 1 of this article discussed Baker Hughes’s (BKR) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Forecast

Based on a regression equation among the natural gas price, global rig count, and BKR’s reported revenues for the past seven years and the previous eight-quarters, revenues will increase by 11% in the next 12 months (or NTM 2023) and further by 7.9% in NTM 2024, before reaching a 7.6% growth rate in NTM 2025. For the short-term trend, we have also considered seasonality.

Based on the regression model using the average forecast revenues, the company’s EBITDA is expected to increase by 39% in NTM 2023. However, in NTM 2024, it can remain unchanged.

Target Price And Relative Valuation

Returns potential using BKR’s forward EV/EBITDA multiple (11.6x) is lower (5% upside) compared to returns potential using the past average multiple (13% upside). The Wall Street analysts have higher return expectations (12% upside).

Baker Hughes is currently trading at an EV-to-adjusted EBITDA multiple of 12.4x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 11.6x. The current multiple is lower than the past five-year average EV/EBITDA multiple of 11.4x.

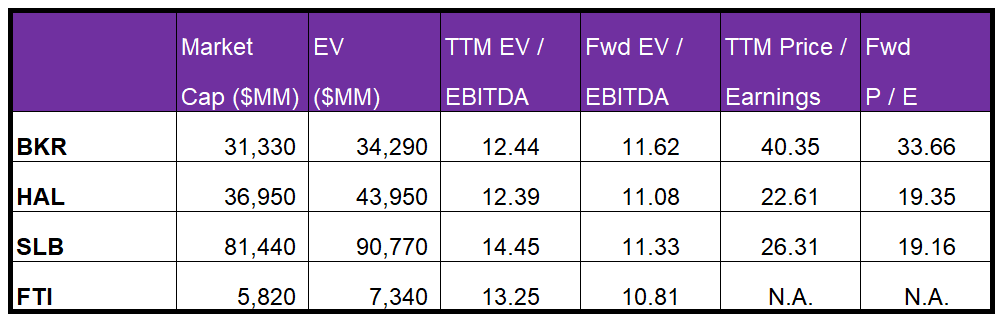

BKR’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is less steep than peers because the company’s EBITDA is expected to increase less sharply in the next four quarters. This would typically result in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is marginally lower than its peers’ (HAL, SLB, and FTI) average. So, the stock is mildly overvalued versus its peers.

Analyst Rating

According to data provided by Seeking Alpha, 20 sell-side analysts rated BKR a “Buy” or “Strong Buy” in the past 90 days, while five of them rated it a “Hold.” None of the sell-side analysts rated a “Sell.” The consensus target price is $34.3, which yields 12% returns at the current price.

What’s The Take On BKR?

While the new FIDs and order bookings in LNG remain consistently high, BKR will gain the most in its Industrial & Energy Technology segment from new orders. The pipeline of new orders lies in LNG, onshore/offshore, and new energy. The new energy has recently booked an order in Malaysia to supply CO2 compression equipment. Along with the topline growth, it has restructured the business in recent times, which can reduce operating costs by $150 million in 2023. Over the next two to three years, it aims to achieve an EBITDA margin target of 20%.

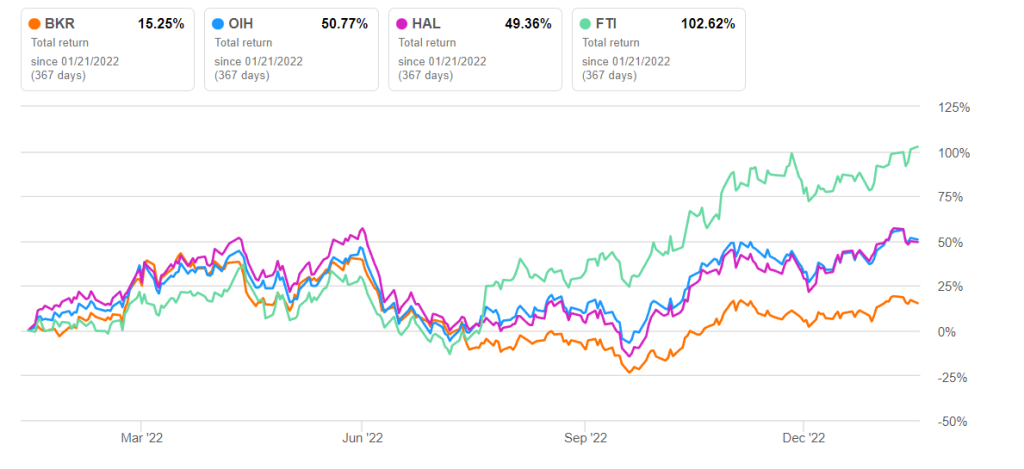

However, the lack of new orders in the Oilfield Services & Equipment segment and the global economic recession are causes of worries for BKR. The drop in cash flow is also something investors need to watch out for. The stock is reasonably valued, with a mild negative bias, versus its peers. So, the stock underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. The balance sheet is relatively robust due to low leverage, while the management expects to return 60%-80% of FCF to shareholders through dividends and share buybacks. Investors might want to “hold” the stock for steady returns in the long term.