- The regression model suggests that the revenue growth trend has remained the same from our last estimates, i.e., an acceleration from NTM 2023 to NTM 2024.

- EBITDA can show healthy growth in the next two years.

- While relative valuation suggests, the stock is reasonably valued versus its peers.

Part 1 of this article discussed RPC’s (RES) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Forecast

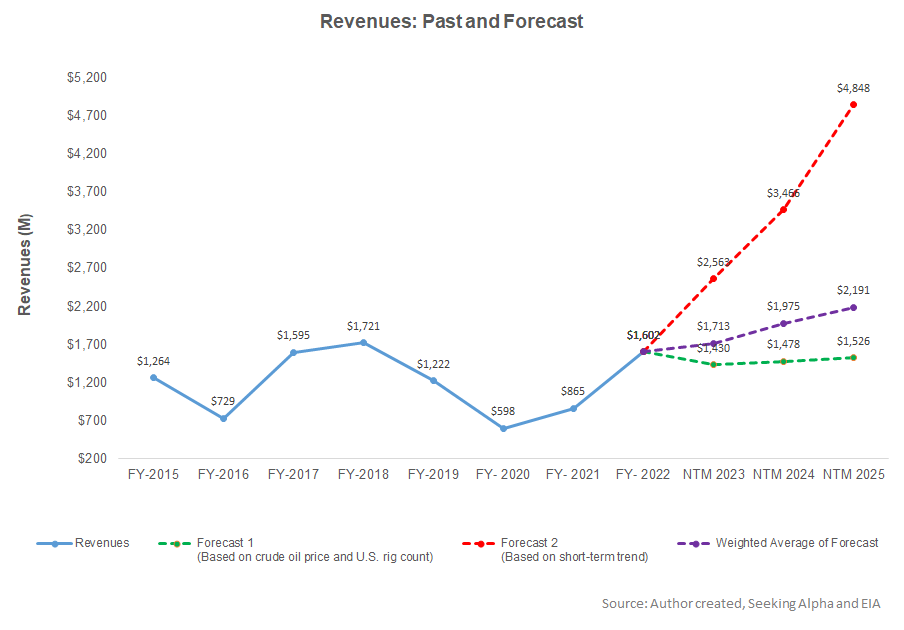

Based on a regression equation on the key energy indicators (crude oil price and the US rig count) and RES’s reported revenues for the past eight years and the previous four quarters, revenues can increase by 7% in the next 12 months (or NTM 2023). The growth rate can accelerate (15% up) in NTM 2024 but moderate in NTM 2025. For the short-term trend, we have also considered seasonality.

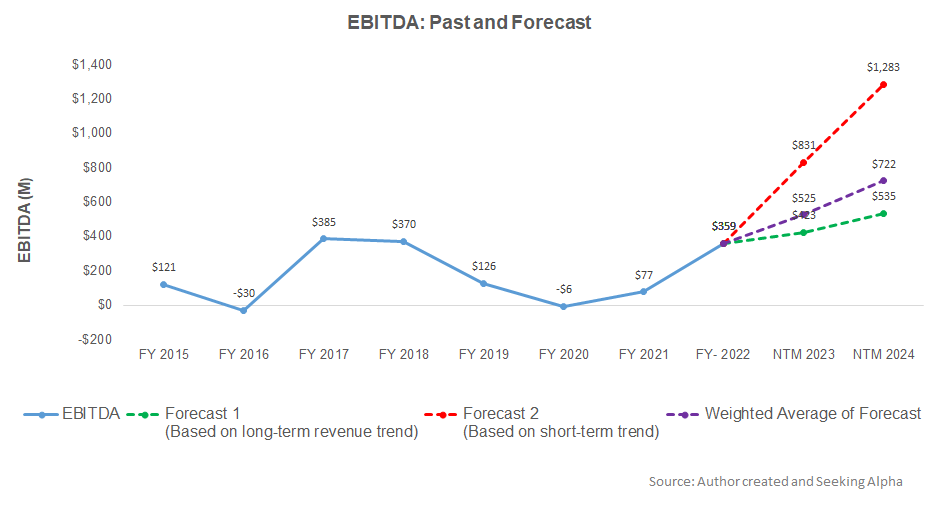

Based on the regression model and the forecast revenues, the company’s EBITDA can increase by 46% in NTM 2023. According to the model, EBITDA can continue to grow by 38% in NTM 2024.

Target Price And Relative Valuation

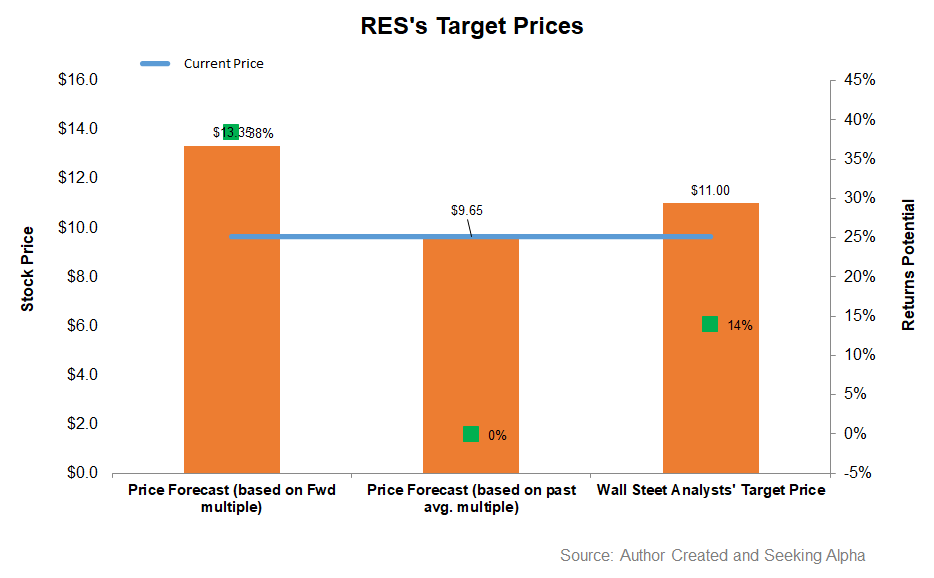

Calculating the EV using RES’s forward EV/EBITDA multiple shows that the returns potential using the forward multiple (5.3x) is higher (38% upside) than the past average multiple (zero returns) and sell-side analysts’ estimates (14% upside) in the next year.

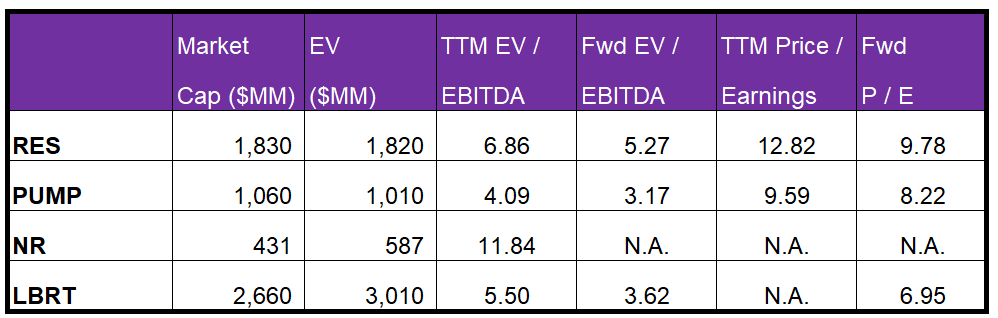

The company’s EV/EBITDA multiple (6.8x) is lower than its peers (PUMP, NR, and LBRT). RES’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA suggests a marginally lower EBITDA growth compared to the peers, which typically reflects in a lower EV/EBITDA multiple. So, the stock is reasonably valued versus its peers.

Analysts’ Rating

According to data provided by Seeking Alpha, one sell-side analyst rated RES a “buy” in the past 90 days, while four of the analysts rated it a “hold.” None rated it a “sell.” The consensus target price is $11, suggesting a 14% upside at the current price.

What’s The Take On RES?

RES recently re-activated its 10th frac fleet and will likely keep the count unchanged in 2023. It expects to increase the share of the ESG-friendly frac fleet composition from 50% to ~75% in the next two years. Improved job mix and efficiency will lead to a better operating performance in the short term. So, the stock outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

However, the US frac spread count growth contracted in recent weeks. Many upstream operations remain vigilant over their capex as the global economic recession sets in. With zero debt and a healthy liquidity base, RES is a healthy investment avenue. The stock is reasonably valued versus its peers. Investors might want to hold it with expectations for a higher return over the medium term.