- Nabors’ US rig count can increase modestly in Q1 2023, while in Saudi Arabia, it plans two rigs in Q1 and two more by Q3 2023.

- The leading-edge revenue per day has nearly doubled over the past year.

- However, the downward pressure of natural gas will adversely affect NBR’s performance.

- Its capex is set to increase by 41% in 2023, which can put the free cash flow and deleverage plan under strain.

Drilling Strategy And Outlook

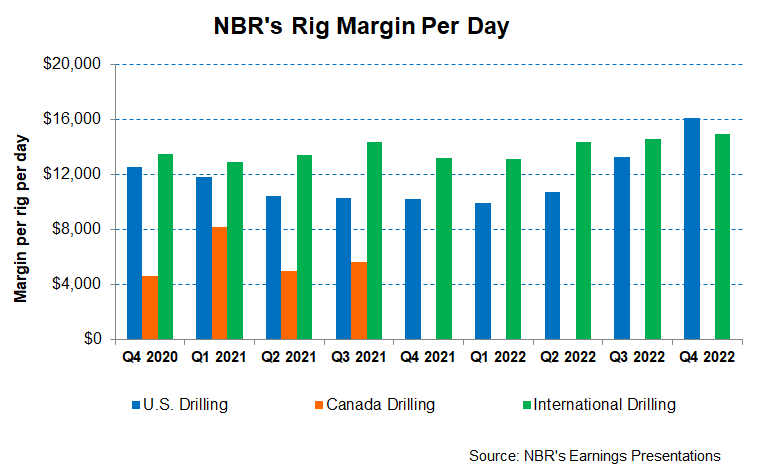

Nabors Industries (NBR) U.S. Drilling topline continued its positive momentum in Q4 2022, even though the US onshore drilling rig count got stuck. As estimated by Primary Vision, the frac spread count underperformed the rig count during this period. NBR’s average daily margins in the US onshore increased by 22% in Q4. The average daily revenue in the US onshore increased by 37%. The daily rig margin in the international operations underperformed versus the US (2% up).

The company’s strategies in the US are to remain short on contract duration, concentrate on the most capable rigs, and focus on premier fields. This approach helped raise the average daily revenue by 12% in the US onshore. It has recently signed contracts with revenue per day above $40,000. So, from leading-edge revenue per day in the low $20,000 range in Q4 2021, the rate has doubled over the past year. Given the trend, NBR’s management is contemplating increasing the long-term contract coverage to 20% to 30% in its US portfolio. With the reactivation of high-spec rigs and elements of NDS added, revenues can go higher. However, investors may note that the reactivation costs are also high, limiting margin expansion. Learn more about NBR in our previous article here.

NBR also saw higher activity and improved day rates in Saudi Arabia and Colombia in Q4. Its joint venture in Saudi Arabia (SANAD) received five awards for new builds, totaling ten. It estimates that each new build would generate an annual EBITDA of ~$10 million, leading to $100 million per year from the new build program. Earlier, in Q3, the company decided to upgrade 40 stacked M550 fleets as the cost advantage. So, combining new builds and cost optimization should increase NBR’s drilling rig revenue and push the margin up.

Q1 2023 Outlook

The natural gas price’s downward pressure will likely hurt NBR’s rig count. From September to December, the natural gas price declined by 33%. In Q1, the management expects to add only one rig compared to Q4. So, the US onshore margin can stay around $16,200 per day in Q1 2023, or 1% higher compared to Q4. In international operations, it plans to add one to two rigs in Q1. On top of that, it plans to add two more rigs in SANAD by Q3 2023. The international daily margin is expected to be in line with Q4 2022.

NDS And robotization

NBR has started investing in innovative technologies in automation, digitalization, and robotization. It aims to improve precision, control, and safety. During Q4, it deployed RZR, a robotics module, on an existing rig. Because the structure is modular, it can be retrofitted onto existing drilling rigs. Adopting a technology-centric business helped it increase the Drilling Solutions segment EBITDA by 18% in Q4 compared to Q3. The company’s gross profit margin expanded by 290 basis points in Q4 versus Q3.

The company’s NDS business also proves the merit of using technology. The penetration of NDS services increased in Q4 to an average of 6.5 services per rig. SmartPLAN installations and the performance tools portfolio, including ROCKit, REVit, and SmartDRILL, have doubled. NDS contributed nearly 38% of the combined average daily margin from the Drilling and Drilling Solutions business in the US onshore. NDS revenue on US third-party rigs grew by 10%.

Analyzing The Q4 Performance

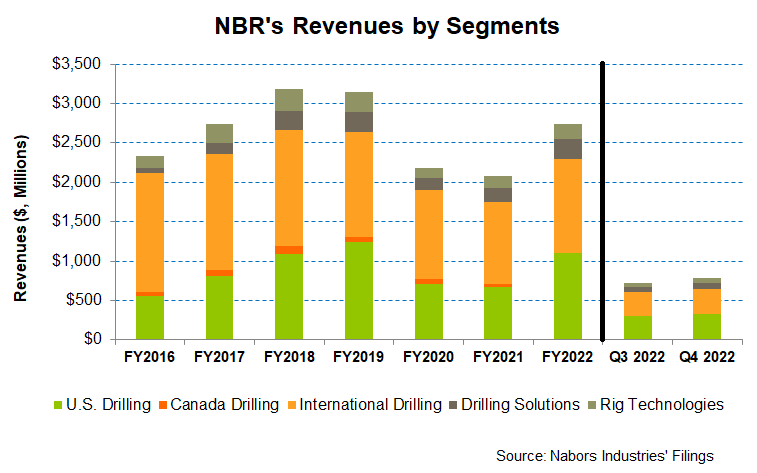

NBR’s drilling activity, leading-edge day rates, and rig utilization have improved over the past few quarters. In Q4 2022, the company’s U.S. Drilling rig count increased by 2% on average compared to Q3 2022, while the international rig count went up by 1%. However, quarter-over-quarter revenues from U.S. Drilling increased by 13% versus a 3% hike in international revenues.

Capex And FCF

In FY 2022, NBR’s cash flow from operations (or CFO) increased by 17% compared to a year ago, led by the year-over-year revenue rise in the past year. In FY 2022, the company’s capex increased by 48%, resulting in free cash flow declines in the past year. The company is targeting a $490 million capex in FY2023 ($180 million for the SANAD new builds), which would be a 41% hike compared to FY2022. In Q1, the target capex is $150 million.

NBR’s debt-to-equity (or leverage) is much higher (4.7x) than many of its peers’ (HP, PTEN, and PDS) average (1.6x). In 2022, it reduced net debt by $186 million.

Learn about NBR’s revenue and EBITDA estimates, relative valuation, and target price in Part 2 of the article.