Frac’ing Outlook

We have already discussed Liberty Energy’s (LBRT) Q1 2023 financial performance in our recent article. Here is an outline of its strategies and outlook. Liberty Energy believes that in the current environment, demand for hydraulic fracturing would primarily originate from maintenance requirements as production will likely remain stagnant in the US and Canada. The real focus for the oilfield services company is its transition from diesel to natural gas. The industry’s demand for fuel-efficient energy and power generation is high because they typically lead to high-return opportunities and offer mobile power generation technology.

About ten years ago, LBRT deployed its first dual-fuel frac spread. Later, it combined DBG frac spreads with digiTechnologies, which include mobile power generation, digiFrac electric fleets, digiPrime hybrid pump, and digiWire electric wireline solutions. During Q1 2023, it deployed its first electric pump, which will soon be integrated with the digiWire electric wireline facility. More recently, in February, it introduced the hybrid pump digiPrime with an all-natural gas engine, which one or two digiFrac electric pumps will complement. It is also in the process of deploying the second digiFrac modularly.

Natural Gas Price & Strategic Adjustments

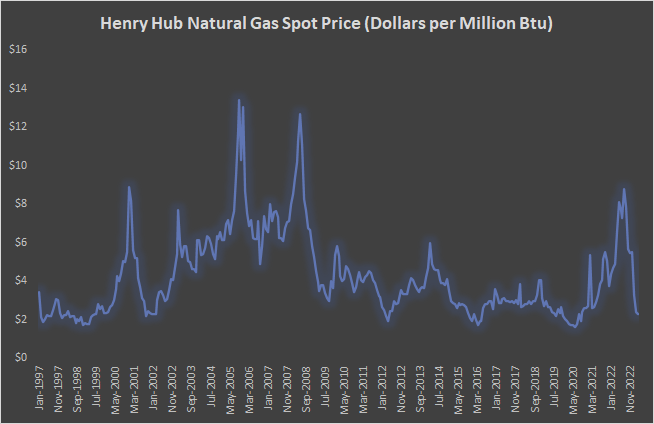

In the US, the Ukraine-Russia conflict and lower winter demand in Europe pushed the natural gas price to an abysmally low level. In the past year, until March 2023, it declined by 53%. The company estimates that the demand pullback would amount to a 6% or 7% decline industry-wide demand for frac fleets. Because many frac services are weighted toward oil-heavy basins, we can expect some movement from natural gas to oil-rich basins in the transitory period before the price recovers.

But LBRT’s management believes that the pricing softness is transitory. An LNG pipeline export growth in Mexico will free the temporary shackle. Rising demand in emerging markets and a gradual recovery in China will lead the charge for the nat gas price recovery.

Frac Spread Supply Update

LBRT reckons that there are about 30 frac spreads that are planned (or under construction) in the industry in the US. Less than 50% of the newbuilds would be deployed in 2023 and the rest in 2024. On the other hand, old and legacy equipment with inefficient pumping would be retired. That would take approximately 25 frac spreads out this year and the next.

Since the new-generations pumps will increase, LBRT’s digiFrac electric pumps will likely stay in high demand because it pairs well with Tier 4 DGB or a Tier 2 dual fuel. A comparison between a digiFrac electric pump and a Tier 4 DGB estimates a 25% to 30% reduction in emissions profile, and a significant improvement in fuel economy can be achieved through electric pump use.

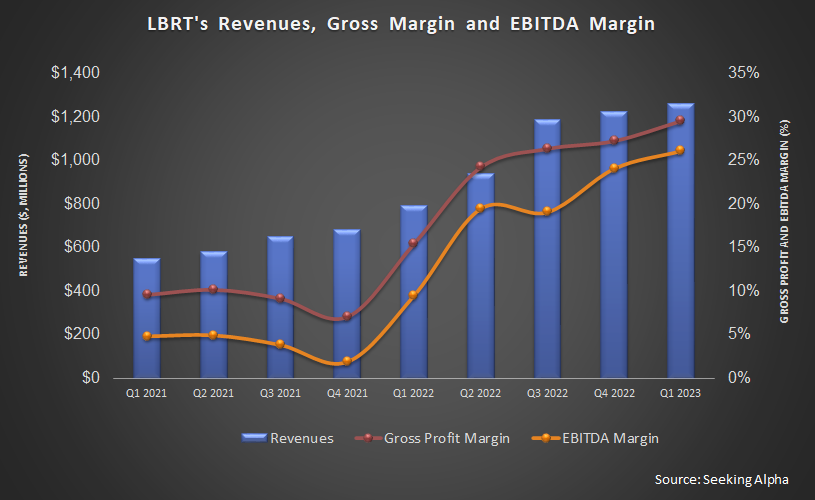

Not only has the company’s topline improved in the successive quarters over the past several quarters due to the change in frac spread fleet dynamics, but the operating margin, too, but has also improved. From Q4 2022 to Q1 2023, its gross and operating margins increased by 230 basis points and 200 basis points, respectively.

Liberty’s Future

LBRT’s current plans include a strategic expansion to power the digiFleets, dual fuel fleets, and reliable CNG supply. Going beyond Permian, it plans to grow its fleet of CNG trailers and expand field gas processing and treating capabilities. On top of the frack equipment demand, LBRT may look to meet increasing demand from micro and mini-grids, data centers, utilities, and emergency power with a combination of CNG and RNG, like hydrogen.

So, intending to secure the supply chain that fuels these frac spreads, it has recently launched Liberty Power Innovations to expand the vertical integration that includes sand, logistics, manufacturing, and design capabilities. It has acquired Siren Energy to accelerate the expansion, which facilitates two Permian sites with transportation, logistics, and well-site pressure reduction services. You can read more about these initiatives in our article here.

Cash Flow & Balance Sheet

Since July 2022, LBRT has returned $218 million to shareholders through cash dividends and the retirement of 7.1% of outstanding shares. The company also expects to fund the repurchases from the available liquidity and expected free cash flow to be generated in the coming quarters.

In January 2023, Liberty restructured its debt. It also retired its $105 million term loan due September 2024. As of March 31, 2023, its total liquidity stood at $308 million.

Relative Valuation

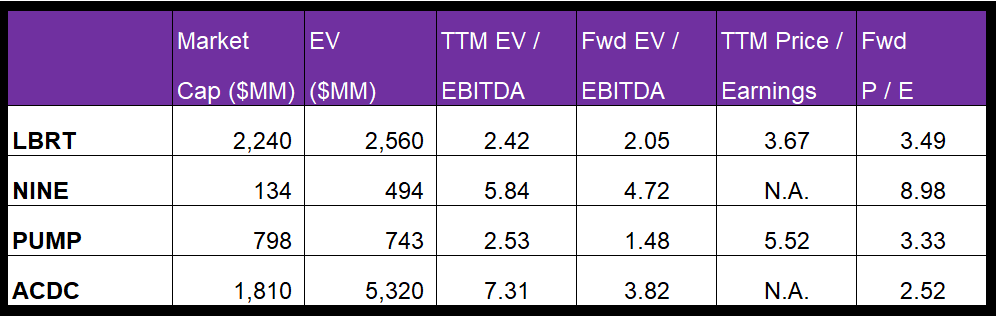

Liberty is currently trading at an EV-to-adjusted EBITDA multiple of 2.42x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 2.1x. The current multiple is significantly lower than its five-year average EV/EBITDA multiple of 20x.

LBRT’s forward EV-to-EBITDA multiple contraction versus the adjusted current EV/EBITDA is less steep than peers because the company’s EBITDA is expected to increase less sharply in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is lower than its peers’ (NINE, PUMP, and ACDC) average. So, the stock is reasonably valued versus its peers.

Final Commentary

LBRT’s management concedes that hydraulic fracturing activity may slow growth in North America due to production growth stalling. The roadblock has accelerated its transition from diesel to natural gas. During Q1 2023, it deployed its first electric pump. It has also brought various solutions to improve energy efficiency, including mobile power generation, digiFrac electric fleets, digiPrime hybrid pumps, and digiWire electric wireline solutions.

Because of natural gas’s spectacular decline over the past six months, we can expect some movement from natural gas to oil-rich basins in the transitory period before the price recovers. However, an LNG pipeline export growth in Mexico will free the temporary shackle. The current environment has helped it integrate its operations. The company’s plans include a strategic expansion to power the digiFleets, dual fuel fleets, and reliable CNG supply through acquisitions and launching a new division called Liberty Power Innovations. The other critical focus is to increase shareholders’ returns, which it plans to finance through liquidity and an expected FCF rise. The stock is reasonably valued versus its peers at this level.