AutoBlend and Top fill System Outlook

We discussed our initial thoughts about Solaris Oilfield Infrastructure’s (SOI) Q1 2023 performance in our short article a few days ago. This article will dive deeper into the industry and its current outlook.

SOI has long-term agreements with many clients to continue using top-fill solutions and AutoBlend, its electric hydrated delivery system. This would be particularly beneficial when pumping equipment and labor availability are tight, thus protecting the margin. The automated all-electric design can replace traditional sand delivery and blender points. In the future, the operators can improve savings by tying all electric equipment to the same power source as electric truck fleets. The benefit of Solaris’ AutoBlend solution is the integration of three mixing tubs, effectively representing three blenders in one.

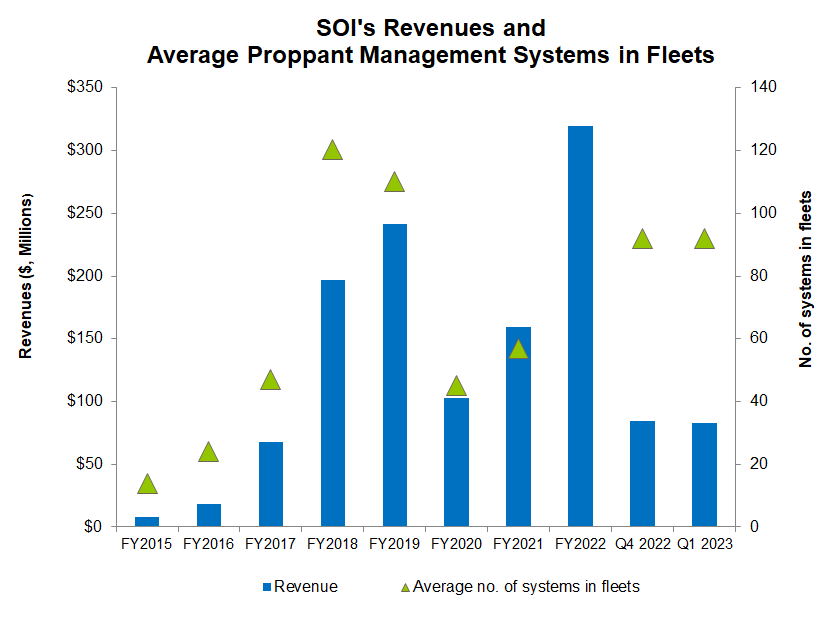

From operating two/three AutoBlend electric systems in 2022, it has increased to five/six by the end of Q1 2023. In Q2, AutoBlend electric system combined with the top fill system would result in higher earnings and return opportunity per well site. Although it may require deploying 2x-3x the capital deployed per frac crew, the contribution margin can also increase to 2x-3x compared to a single six-pack system per crew. With a growing demand backlog, the number can improve further.

Growth Opportunities

We already discussed in our previous article how SOI’s top fill systems and belly dump solution helped it proliferate in relatively less-active basins like the Rockies and sand storage facilities in other onshore Basins. The top-fill system delivers increased value by providing high-quality, low-cost, and safe technologies. SOI is one of the US’s largest belly dump-compatible sand storage providers onshore. From a mere 1% of its sand systems working with a top fill kit in Q1 2022, it has expanded to 25% and is growing. In Q2, it will likely face challenges from an activity softness led by the weakness of the natural gas price. The demand for flexible and delivery solutions will grow despite the current softness of hydraulic fracturing.

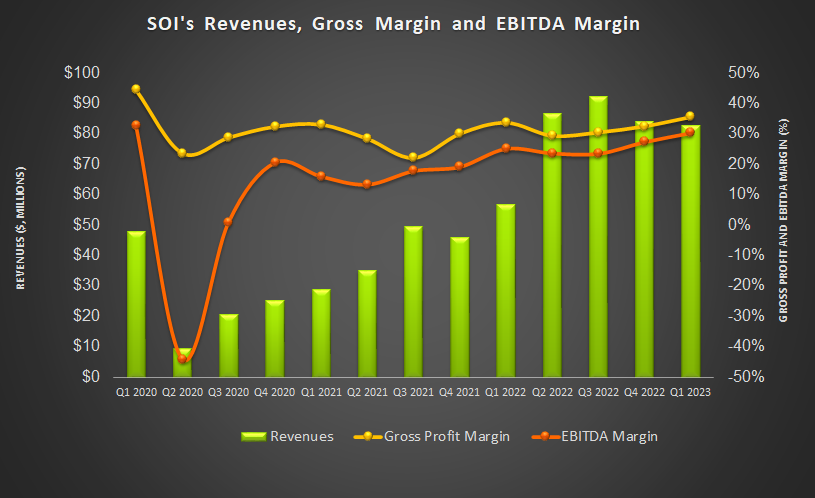

Quarter-over-quarter, SOI’s revenues decreased by 1.6% in Q1 due to lower contributions from last-mile trucking and equipment transportation. However, its adjusted EBITDA margin expanded by 300 basis points. In Q1, it added eight fully utilized top-fill systems, facilitating the incremental gross profit per sand system. Pricing improvement and contribution from additional top-fill systems led to margin progress in Q1. The deployments of the top fill and AutoBlend systems improved pricing. This also smoothed the weakness caused by frac fleet reallocations caused by lower natural gas prices.

Margin Challenges

In Q1 2023, SOI’s gross margin and adjusted EBITDA margin expanded by 310 basis points and 300 basis points, respectively, compared to Q4 2022. But, the company faces challenges due to the low-margin pass-through characteristics of the trucking services. The longer distances between mines and well sites can adversely affect the margin. Investors may note that the share of ancillary services (last mile sand transportation) reduced to 5% of total gross profit in Q1 from 10% a quarter earlier. The drop in sequential change was caused by fewer tonnes transported in the last mile service offering.

Year-to-date, crude oil and natural gas prices dipped by 8% and 50%, respectively. According to Primary Vision, the US frac spread count was steady during this period, 9% up. However, the energy price weakness can trigger frack spread count slowdown in the coming weeks, adversely affecting its operating performance.

Shareholders’ Returns And Cash Flows

In 2018, the company initiated dividends and consistently returned cash to shareholders. In March 2023, it committed to return at least 50% of free cash flow to shareholders through dividends and share repurchases. So, it raised the dividend by 5% to $0.11 per share. It also initiated a $50 million share repurchase program. In Q1, it completed a share repurchase worth $14 million. The company’s management believes that the volatility and recession in the global markets drove a dislocation in its stock price relative to its intrinsic value. So, enhancing shareholder returns can address the issue by pumping up the stock price.

In Q1, SOI’s cash flow from operations increased by 169% compared to a year ago. Free cash flow, however, stayed marginally negative. It has recently expanded its credit facility to $75 million. If cash flows improve further, it will have lesser dependence on the credit facility borrowing to fund the capex. The increased liquidity can support its capital expenditure program, which is weighted towards 1H 2023. It also helps the shareholder returns policy.

Relative valuation

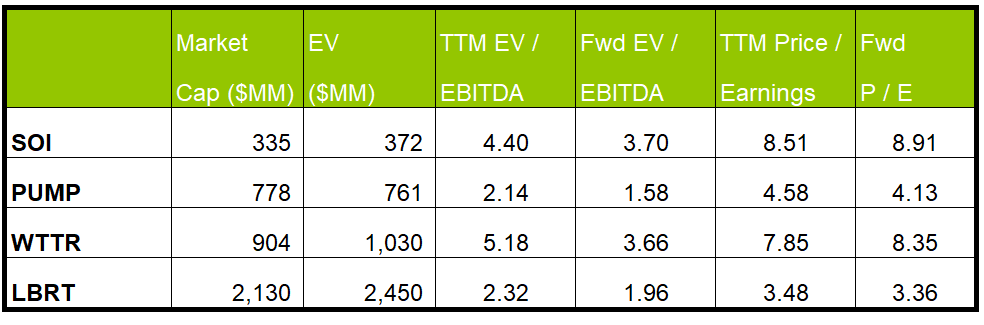

SOI is currently trading at an EV-to-adjusted EBITDA multiple of 4.4x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 3.7x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 10.7x.

SOI’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is less steep than peers because its EBITDA is expected to increase less sharply than its peers in the next year. This typically results in a lower EV/EBITDA multiple than its peers. However, the stock’s EV/EBITDA multiple is higher than its peers’ (PUMP, WTTR, and LBRT) average. So, the stock is overvalued versus its peers.

Final Commentary

Since 2022, SOI’s AutoBlend electric systems have increased from two to three to five-to-six by the end of Q1 2023. With a growing demand backlog, the number can improve further. Many clients continue using top-fill solutions and AutoBlend, which would result in higher earnings and return opportunities per well site. The other key offering for SOI is the belly dump-compatible sand storage, which made inroads in relatively less-active basins like the Rockies. In Q1, it added eight fully utilized top-fill systems, facilitating the incremental gross profit per sand system.

On the other hand, it faces operating margin challenges due to the low-margin pass-through characteristics of the trucking services. So, the share of ancillary services has reduced considerably over the past year. Given the relative weakness in fracking in the current environment, SOI’s management has increased shareholders’ values through dividend hikes and share repurchases. The stock is relatively overvalued versus its peers.