Frac’ing Update And Challenges

In our short article, we discussed our initial thoughts about ProPetro Holding’s (PUMP) Q4 2023 performance a few days ago. This article will dive deeper into the industry and its current outlook. The first leg of the strategy involves transitioning its legacy fleet and equipment to next-generation offerings. The company continues to add to its FORCE electric fleet offering in the Permian Basin. At the start of 2024, it had two FORCE electric fleets after deploying the second FORCE electric fleet in early November. Plus, it has seven Tier IV DGB dual fuel fleets operating. The company expects to deploy two more FORCE electric fleets in the next few months. In the near future, its next-gen fracs will displace diesel-run fracs.

However, in Q4, PUMP’s effective frac spread utilization fell to 12.9 from 15.4 a quarter earlier. The challenge for the company is to improve utilization, which fell in Q4 due to higher-than-expected white space from deferred customer activity. In Q1 2024, the company expects frac spread utilization to back up to 14-15 spreads. It also has to maintain crew continuity and the ongoing fleet performance. This involves associated labor costs despite the temporary decline in utilization. For example, the company incurred a lease expense of $4.3 million related to the FORCE electric spreads.

Acquisitions

PUMP has also been active in the M&A space, its second growth strategy. Recently, it acquired Par Five Energy Services to scale up its cementing business. The acquisition also expanded its operations in the Permian’s Midland and Delaware Basin areas. The company should benefit from potential revenue synergies, leveraging Par Five’s capacity. In November 2022, it acquired Silvertip Wireline business accretive to its earnings power and free cash flow generation.

Capital Allocation Strategy

In May 2023, PUMP’s board authorized a $100 million share repurchase program. The strategy signals the management’s conviction in the future of the company. The management also believes that ProPetro’s stock is relatively undervalued compared to the intrinsic strength of its financial results and strong outlook.

Industry Outlook

PUMP will look to capitalize off the recent transactions in the E&P industry, including the Diamondback And Endeavour potential merger, the XOM-PXD merger, and the CVX-HES merger; many of the recent mergers are aimed at benefiting from the Permian basin’s stupendous growth in energy production over the past decade. PUMP offers differentiated service quality and equipment, intending to become the “service provider of choice” after this consolidation. Outside of the Permian, it plans to insulate its business from the uncertainty over the spot market rate.

As I pointed out in my previous article, over the past year, the fracking industry went through equipment attrition, supply chain constraints, and a resulting equipment discipline. The company has been optimizing its operations and industrializing the business following the transformation of its fleet, share buyback, and accretive M&As. The measures are expected to accelerate its free cash flow and continue to return capital to shareholders.

Q4 Results And Financial Metrics

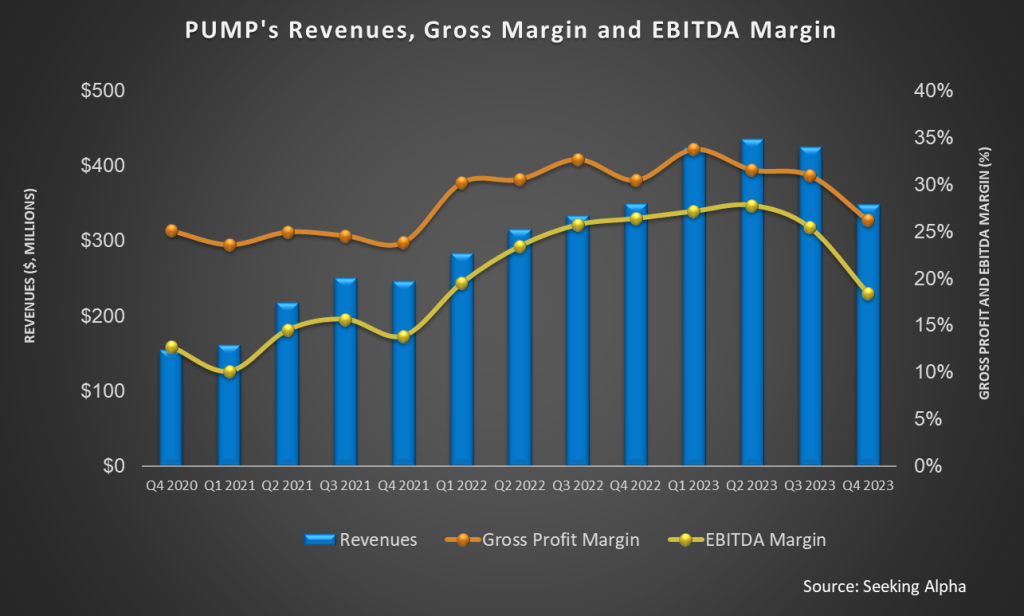

As we discussed in the Q4 earnings article, Quarter-over-quarter, PUMP’s revenues decreased by 18% in Q4, while its adjusted EBITDA margin contracted by 690 basis points due primarily to lower hydraulic fracturing utilization. Its cash flow from operations increased by 25% in FY2023.

However, its capex guidance indicates a lower capital expenditure in FY2024 ($200 million and $250 million). In 2023, it completed a large reinvestment cycle and is realizing the benefits of its optimization efforts. a lower capital intensity. Higher quality and longer-term investments can result in capital returns through M&As and share repurchases.

Relative Valuation

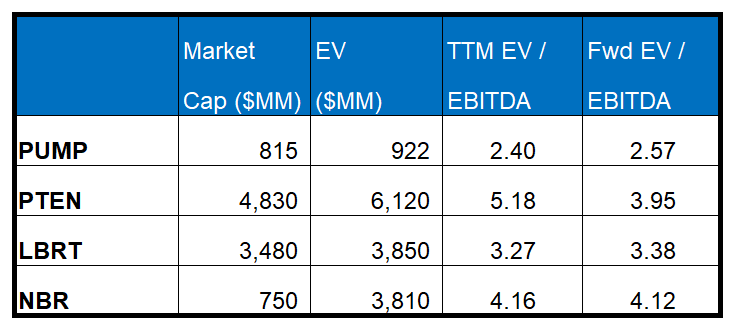

PUMP is currently trading at an EV/EBITDA multiple of 2.4x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 2.6x. The current multiple is below its five-year average EV/EBITDA of 4.7x.

PUMP’s forward EV/EBITDA multiple expansion versus the current EV/EBITDA contrasts with its peers because its EBITDA is expected to decrease versus a rise in EBITDA for its peers in the next year. This typically results in a much lower EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple is lower than its peers’ (PTEN, LBRT, and NBR) average. So, the stock is reasonably valued, with a negative bias, compared to its peers.

Final Commentary

At the end of 2023, PUMP’s frac utilization took a downturn due to lower customer activity. Lower utilization led to higher labor costs. It gradually reduces the share of the diesel fleet in the portfolio and replaces it with e-francs and Tier IV DGB frac spreads. After deploying the first e-frac in Q4, it also plans to add two more in early 2024. During Q4, it acquired Par Five Energy Services to scale up its cementing business. The company continued its share repurchase program as it considers the stock undervalued in the current market. Its focus on the Permian Basin will continue to support the company’s growth plans as E&P consolidations take place in that region.

Combining efficient frac spreads, M&As, and capital allocation strategies should enhance PUMP’s values in the market. It will spend less on capex in FY2024, improving its free cash flow. The stock appears reasonably valued, with a negative bias, versus its peers.