Frac Spread And Strategies

Our short article discussed our initial thoughts about ProFrac Holding’s (ACDC) Q1 2024 performance a couple of weeks ago. This article will dive deeper into the industry and its current outlook. ACDC focuses on electric frac deployment. In Q1, it completed a pad in Midland to improve the efficiency of its West Texas frac spreads. E-spreads bring significant value through fuel savings, high reliability, and efficient operations. Much of the requests from its customers veer toward electric and Tier-4 Dual Fuel technologies that can trigger additional deployments in the coming months. Its pressure pumping utilization has significantly improved as downtime has been minimized. The company is currently building an e-fleet backlog and expects to have all the e-fleets deployed later in 2024.

By the end of Q1, ACDC estimated that 70% of its frac spreads operated for large customers on a dedicated basis. As the contract terms extended, its revenues and cash flows stabilized. In Q1, it generated ~11% sequential improvement in pumping hours per fleet, estimated by the company, which stands as one of the highest in ProFrac’s history. Efficiency across all its frac spreads was up nearly 30% in March compared to the quarterly average a year earlier.

Q2 Outlook

ACDC plans to generate “mid-to-high-teens” EBITDA per fleet in Q2. ACDC has a vertically integrated business model that benefits from a lower cost of scale, yielding robust returns. In Q1, the company generated $159 million of adjusted EBITDA. At Primary Vision, we estimate the company operated 39 active frac spreads. So, adj. EBITDA/fleet amounted to $4.1 million. This means the company expects a significant increase in profitability per frac spread in Q2. It also expects the total active frac spread count to increase in Q2, which means its adjusted EBITDA should increase.

Proppant Sand Performance

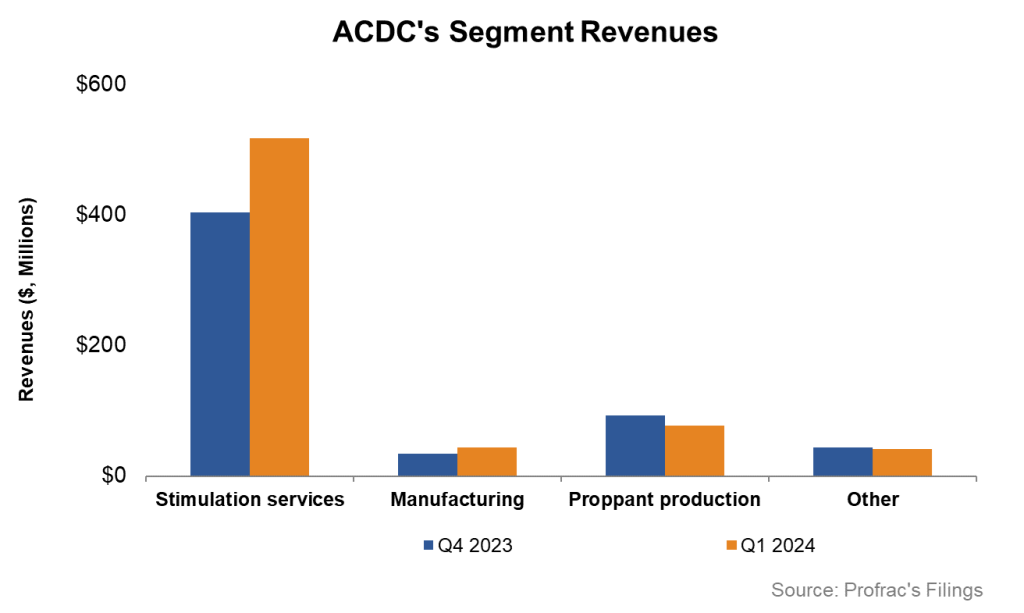

In Q1, ACDC’s Proppant Production segment suffered a setback as both its topline and EBITDA margin shrank compared to Q4 2023. weather and operational disruptions primarily caused the deterioration even though its sales pipeline expanded. To remedy this, the company took the initiative to improve the utilization of its mines.

In the La Mesa mine, completed in March, output has doubled as utilization reached 70%. Due to high demand in South Texas, it is working on a similar plant improvement. The management expects a month-over-month improvement in utilization in Q2. The volume recovery, however, would take time and can happen by Q4.

A Q1 Financial Discussion

Quarter-over-quarter, ProFrac’s revenues increased by 19% in Q1 2024, while its adjusted EBITDA margin inflated by 510 basis points due to increased activity level. However, ACDC’s cash flow from operations decreased by 66% in Q1 2024 compared to a year ago. In Q1, it spent $60 million on capex because of fleet deployments, upgrades, and mine optimization. Despite lower capex, FCF declined steeply in Q1 2024. In FY2024, the company plans to incur $175 million in capex (at the guidance mid-point), which would be 34% lower than a year ago.

Of the $1.05 billion of debt, the majority will mature after 2029, which means its financial risks are low in the near term. ACDC’s leverage (debt-to-equity) was 0.81x as of March 31, 2024. It had $167 million of liquidity as of that date.

Relative Valuation

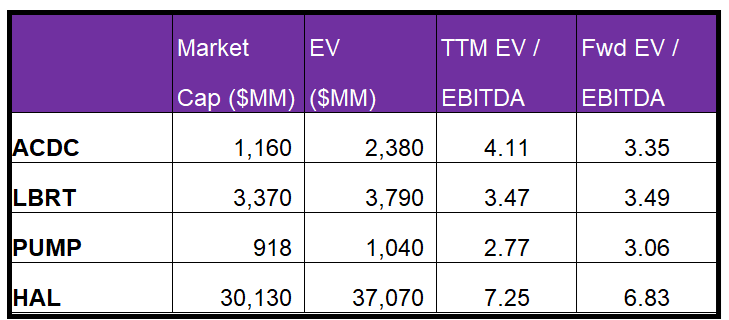

ACDC is currently trading at an EV/EBITDA multiple of 4.1x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is ~3.4x.

ACDC’s forward EV/EBITDA multiple contraction versus the current EV/EBITDA is steeper than its peers because its EBITDA is expected to increase more steeply than its peers in the next year. This typically results in a higher EV/EBITDA multiple than its peers. However, the stock’s EV/EBITDA multiple is lower than its peers’ (LBRT, PUMP, and HAL) average. So, the stock is undervalued versus its peers.

Final Commentary

ACDC’s completed a pad in Midland to improve efficiency in Q1. The preference for electric and Tier-4 Dual Fuel technologies can trigger additional deployments in the coming months. The company is currently building an e-fleet backlog and expects to have all the e-fleets deployed later in 2024. The company’s primary focus remains on improving the utilization of frac spreads and proppant mines.

Because ACDC operates 70% of its frac spreads for large customers on a dedicated basis, its revenues and cash flows have remained stable. Its pumping hours per fleet saw sequential improvement in Q1, which can significantly increase profitability per frac spread. However, the company’s proppant sand operations underperformed in Q1. The balance sheet can become a concern with lower cash flows and a relatively high leverage ratio. The stock is relatively undervalued versus its peers.