Industry Outlook And NOV’s Strategies

We discussed our initial thoughts about NOV’s (NOV) Q1 2024 performance in our short article a few days ago. This article will dive deeper into the industry and its current outlook. In 2024, NOV’s management identified two primary drivers – developing unconventional basins and greenfield and brownfield offshore basins internationally. The large offshore projects have ramped up over the past three years, which can lead to increased demand for offshore production assets. The management trusts in seeing stable oil prices and a strong long-term outlook for natural gas and LNG demand. Evidently, international E&P operators require better drilling, stimulation, and production equipment and technologies, which NOV is well equipped to provide.

NOV estimates that the new international wells need corrosion-resistant flowlines, chokes, valves, and processing equipment. In the current environment, offshore E&P operators need to reactivate drilling rigs. The process can accelerate the corrosion, which needs to be retrofitted with drill pipe bits and drilling tools. Onshore, tendering, and drilling activity targeting natural gas has been robust in the Middle East and is rising in Latin America and Asia. Since NOV supplies many global offshore drilling fleets, the rig activation over the past few quarters has worked to the company’s advantage.

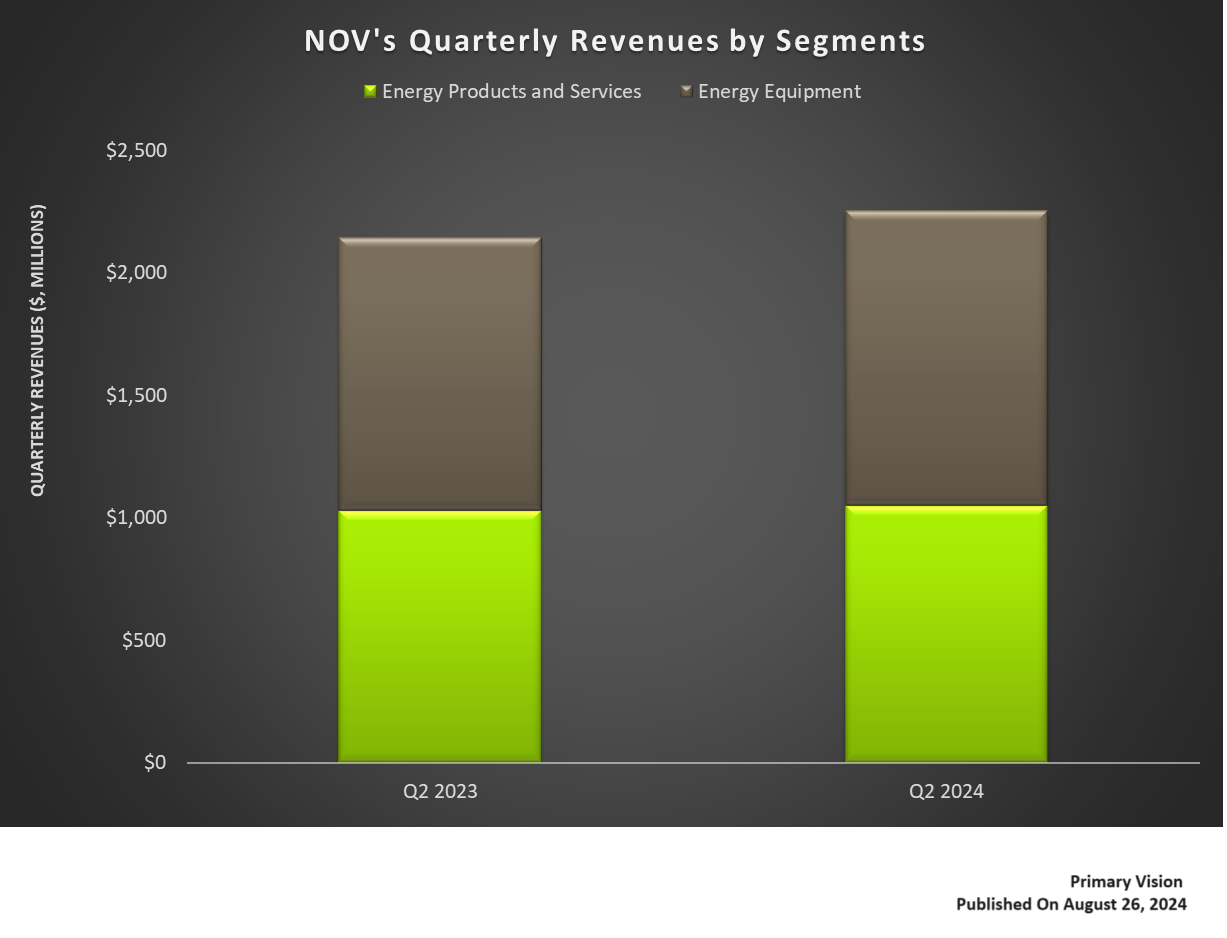

On top of traditional aftermarket spares and services, NOV generates a stream of recurring revenues from subscription services. Such services include monitoring offshore rigs, regular updates, and support from the NOVOS automation systems. It currently has 125 such systems deployed, 26 being installed, and another 63 in the backlog. In North America, the E&P merger and low natural gas prices have led to lower US onshore activity. Also, low natural gas prices and NGL prices reduced realized wellhead revenues in West Texas. This adversely affected wellbore construction and drilling propensity. As a result, fleet utilizations fall for the North American oilfield service companies. This was evidenced by NOV’s 8% lower revenues from the Energy Equipment segment in Q2 as the share of the North American mix declined to 25%.

Backlog

NOV’s book-to-bill ratio was 1.29x in 1H 2024. Despite the headwinds in North America, as discussed above, rising demand in offshore and international markets should keep the ratio above 1x in 2H 2024. However, order bookings can decline marginally in Q3. You can read more about the company’s recent key projects in our article here.

Acquisition And AI Benefits

Recently, NOV acquired the remaining stake in Keystone Tower Systems. Keystone develops a proprietary spiral welding manufacturing technology for the wind industry. The technology allows access to more robust, more steady wind and utilizes more giant turbines. It invested in Keystone in 2019 and became the majority shareholder in 2023. It won a contract for 398-meter-tall wind towers from a major wind turbine manufacturer. NOV also provides AI solutions through its KAIZEN app. It has now begun applying the app to its operations across over 50 manufacturing facilities. The platform leverages NOV’s proprietary Max Edge devices and is expected to optimize capacity, improve machine tool utilization, and drive better absorption.

Q2 Financial Results

In Q2 2024, the Energy Equipment segment witnessed 8% year-over-year revenue growth, while the Energy Products and Services segment revenue increased by 2%. The Energy Equipment segment saw operating income rise tremendously (1.8x up) from Q2 2023 to Q2 2024. On the other hand, operating profit in the Energy Products and Services segment decreased. Its cash flow from operations turned significantly positive in 1H 2024.

The company has recently increased its dividend by 50% and expects to return at least 50% of the excess FCF to shareholders. During Q2, it repurchased 2 million shares at an average price of $18.50 per share, totaling $37 million. So, it has returned $67 million of capital to the shareholders in Q2.

Relative Valuation

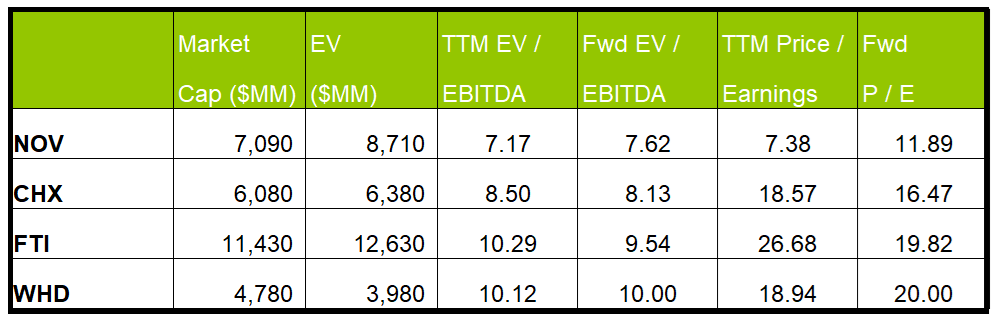

NOV is currently trading at an EV/EBITDA multiple of 7.2x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 7.6x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 29.5x.

NOV’s forward EV/EBITDA multiple expansion versus the current EV/EBITDA contrasts its peers because its EBITDA is expected to decrease compared to an expansion in the multiple for its peers in the next year. This typically results in a much lower EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple is lower than its peers’ (CHX, FTI, and WHD) average. So, the stock is reasonably valued versus its peers.

Final Commentary

NOV’s management is optimistic about international and offshore activity growth, mainly by international E&P operators and NOCs. These players require better drilling, stimulation, and production equipment and technology solutions. NOV’s expertise in retrofitting with drill pipe bits and drilling tools should boost NOV’s sales. The offshore E&P operators also need to reactivate drilling rigs. On top of that, the company generates a stream of recurring revenues from subscription services.

However, low natural gas prices and NGL prices reduced realized wellhead revenues. NOV also provides renewable energy solutions, which is evidenced by the completion of its acquisition of Keystone Tower Systems. It recently increased its dividend by 50% and expects to return at least 50% of the excess FCF to shareholders. The stock is reasonably valued versus its peers.