Frac’ing Update

In our short article, we discussed our initial thoughts about ProPetro Holding’s (PUMP) Q2 2024 performance a few days ago. This article will dive deeper into the industry and its current outlook. The company’s focus on the Permian Basin can partially offset the low growth potential in other US Basins. Despite the challenges, PUMP’s management is optimistic about the North American onshore market potential over the “next several years.” In this environment, the company will try to maximize cash flow generation. It plans to invest in fleet recapitalization. Also, the company sees higher demand for its next-generation natural gas-burning assets. After Q2, it had seven Tier IV DGB dual-fuel fleets that will accelerate diesel displacement.

In Q2, PUMP’s effective frac spread utilization was 15 compared to 12.9 in Q4 2023. The company will change the basis of frac utilization calculation. From reporting based on days worked, it will report the number of active frac fleets. During Q2, 14 hydraulic fracturing fleets were active, and the company expects to keep them unchanged at 14 in Q3.

Pricing And Sales-mix Strategy

PUMP’s management assesses that dual fuel electric assets pricing remains strong. However, in the Permian, diesel pricing in the frac market typically sets the note. Because a few oilfield services companies set pricing at an unsustainably low level, it can disrupt the diesel market. Lower rig count and competitive pricing across conventional diesel assets are the two primary concerns. Adverse weather also adversely affected Permian activity in Q2. For PUMP, though, diesel is an insignificant part of the mix.

PUMP has decided to accelerate the winding down of all investments in diesel equipment. The remainder of the natural gas-burning electric dual fuel market has stayed robust. The company faces challenges, too. It experienced a weaker Q2 in the wireline business compared to Q1 due to shifting customer schedules and significant weather impact, particularly in the Permian during May and June.

e-Frac Strategy

In Q2 2024, PUMP deployed a third FORCE electric frac spread, the latest of which was deployed with ExxonMobil as part of a three-year contract. It expects to deploy another e-frac with XOM in the next few months. The agreement includes wireline and pump-down services in 2024, with an option for a third FORCE spread by early 2025. The company continues to invest in its FORCE electric offering, which will replace conventional diesel equipment. It has placed an order for its fifth FORCE electric fleet to be fielded in 2024.

PUMP’s management expects the transformation of its frac spreads to more FORCE electric spreads, which will drive a rapid decline in associated maintenance capital spending. The multi-year contractual coverage can increase free cash flow and result in durable profitability. Its investments should yield earnings enhancement for the rest of 2024. Its Q2 results reflected another quarter of lower CapEx relative to its original budget, which will support the free cash flow generation.

M&A Strategy

PUMP’s previous acquisition of Silvertip (November 2022) has boosted its earnings and free cash flow. Its acquisition of Par Five Energy (December 2023) has been integrated into the legacy cementing business. In Q2, it completed the acquisition of Aqua Prop, which provides cost-effective wet sand solutions. ProPetro can remove unnecessary equipment off-location through this merger. As a result, the company’s integrated completions services is one of the best in the Permian Basin. It will continue to seek further M&A opportunities.

Q2 Results And Financial Metrics

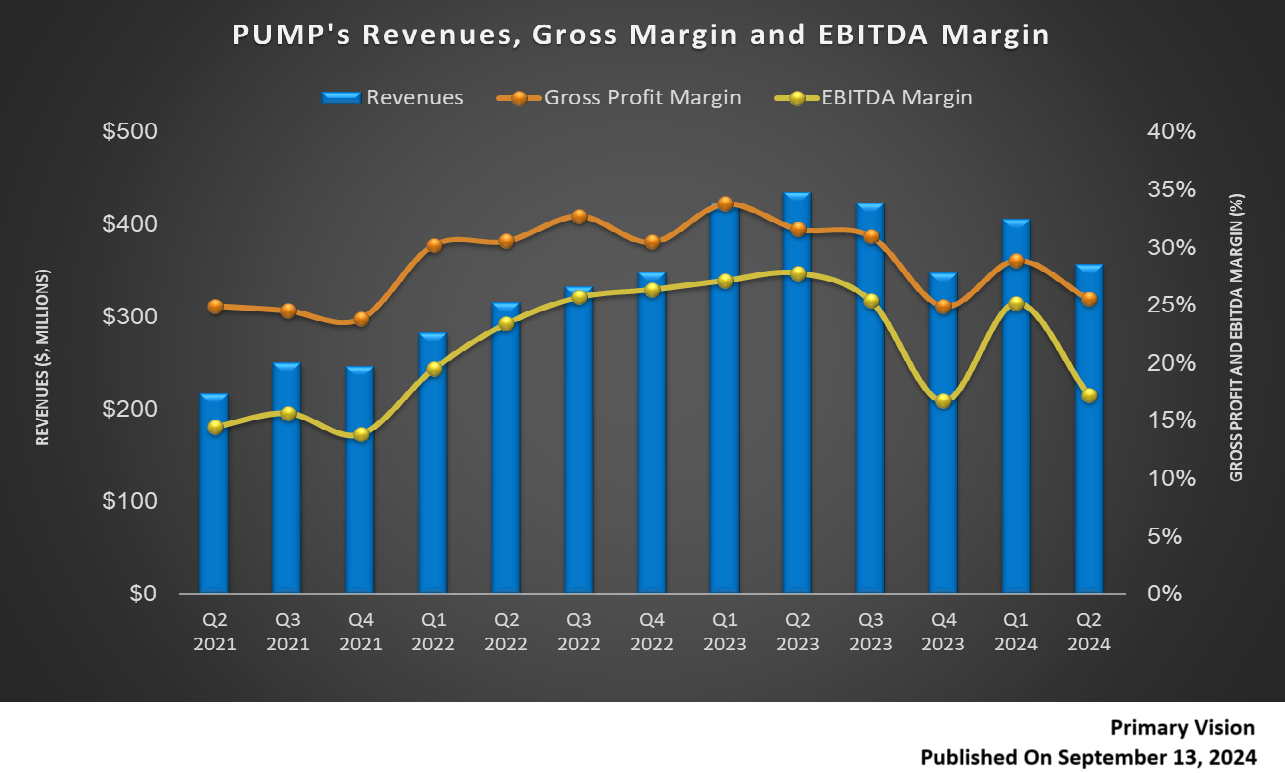

As we discussed in the Q2 earnings article, quarter-over-quarter, PUMP’s revenues from the Hydraulic Fracturing segment decreased by 12% in Q2 2024, while its adjusted EBITDA declined by 26%. Its revenues and adjusted EBITDA from the Wireline segment decreased by 19% and 36%, respectively.

PUMP’s cash flow from operations decreased modestly (by 4%) in 1H 2024 compared to FY2023. Its free cash flow, however, turned positive in 1H 2024 as capex fell. It reduced its prior capex guidance of $200 million-$250 million for 2024 down to $175 million-$200 million. By June 30, its liquidity was $145 million. It increased and extended share repurchases under the $200 million repurchase program authorized by its Board in April 2024.

Relative Valuation

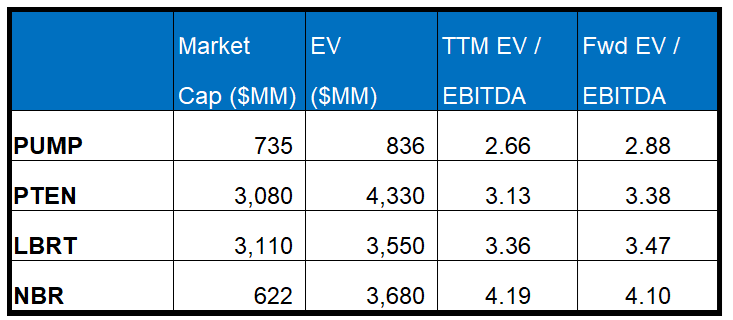

PUMP is currently trading at an EV/EBITDA multiple of 2.7x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 2.9x. The current multiple is below its five-year average EV/EBITDA of 4.6x.

PUMP’s forward EV/EBITDA multiple expansion versus the current EV/EBITDA is sharper than its peers because its EBITDA is expected to decrease steeply over the next year. This typically results in a lower EV/EBITDA multiple than its peers. The stock’s EV/EBITDA multiple is lower than its peers’ (PTEN, LBRT, and NBR) average. So, the stock is reasonably valued versus its peers.

Final Commentary

PUMP focuses on the Permian Basin to mitigate the growth concerns in other US Basins. In the diesel frac operations, pricing remains low. So, it plans to invest in frac spread recapitalization and dual fuel electric assets, where pricing remains strong. In Q2 2024, PUMP deployed a third FORCE electric frac spread and expects to deploy another e-frac with ExxonMobil in the next few months. The transformation in the frac mix to more electric fleets will help lower capex. This, plus the benefits from the prior acquisitions, has boosted its earnings and free cash flow. Its integrated completion service approach has brightened its prospects in the Permian. Its frac spread is expected to remain unchanged in Q3.

However, PUMP’s wireline business will remain weak in Q3 due to shifting customer schedules and significant weather impacts. Its cash flow from operations decreased marginally in 1H 2024, although FCF turned positive due to lower capex. With a robust FCF in sight, it increased and extended the share repurchases program. The combination of efficient frac spreads, M&As, and capital allocation strategies should enhance PUMP’s values in the market. The stock is reasonably valued compared to its peers.