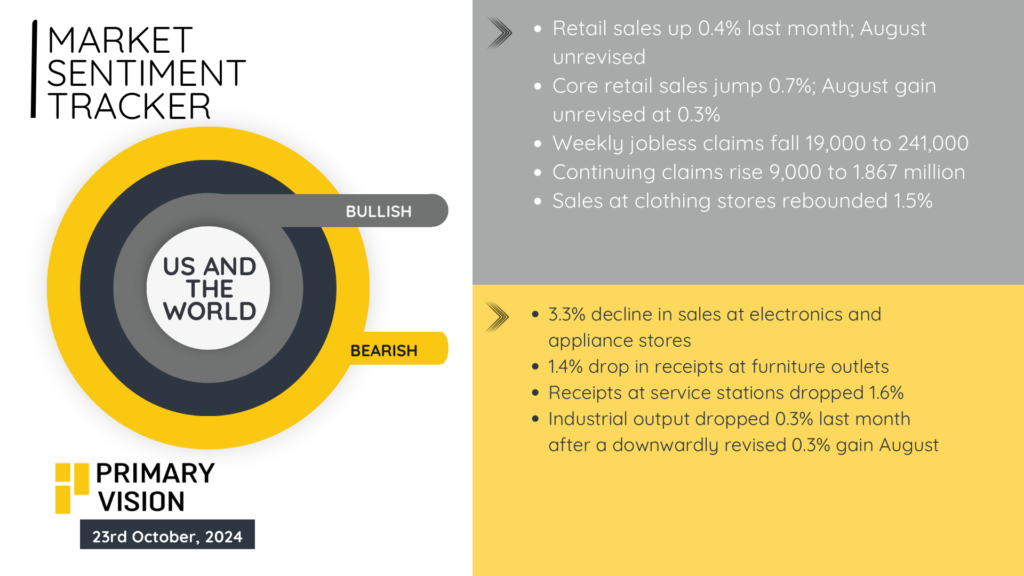

Retail sales rose 0.4% in September, maintaining momentum from the unrevised August figure, while core retail sales jumped 0.7%. Weekly jobless claims saw a notable drop, falling by 19,000 to 241,000, though continuing claims rose slightly to 1.867 million, indicating some underlying labor market softness. Notably, sales at clothing stores rebounded by 1.5%, providing a positive bump, but other areas painted a more mixed picture. Sales at electronics and appliance stores slumped by 3.3%, and receipts at furniture outlets also fell by 1.4%.

Receipts at service stations tumbled 1.6%, reflecting continued pressure from falling gas prices. Meanwhile, industrial output slipped by 0.3%, following a revised 0.3% gain in August. This suggests that while consumer spending holds up in specific areas like clothing, sectors like durable goods are struggling, hinting at potential slowing in broader economic momentum as we head toward the final quarter of the year.

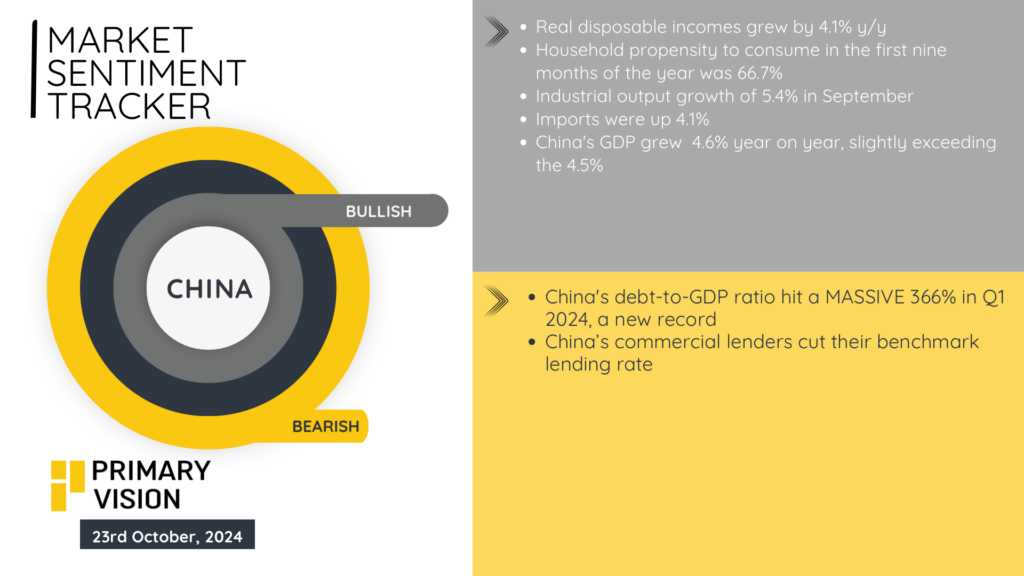

Real disposable incomes in China rose by 4.1% year-on-year, reflecting solid household earnings growth, while the propensity to consume was at 66.7% for the first nine months. Industrial output showed impressive gains, growing by 5.4% in September. Import growth of 4.1% further signals recovery in demand for foreign goods. China’s GDP rose by 4.6% year-on-year, slightly above expectations. However, concerns loom over the country’s staggering debt-to-GDP ratio, which reached an unprecedented 366% in Q1 2024, raising alarm about the sustainability of growth. To support the economy, China’s commercial lenders have cut their benchmark lending rates. While these figures suggest robust economic activity, the rising debt level and structural challenges, such as the real estate downturn, remain potential risks for long-term stability. Overall, despite the current positive performance, economic headwinds persist as China continues to manage its debt burden amidst efforts to maintain growth.

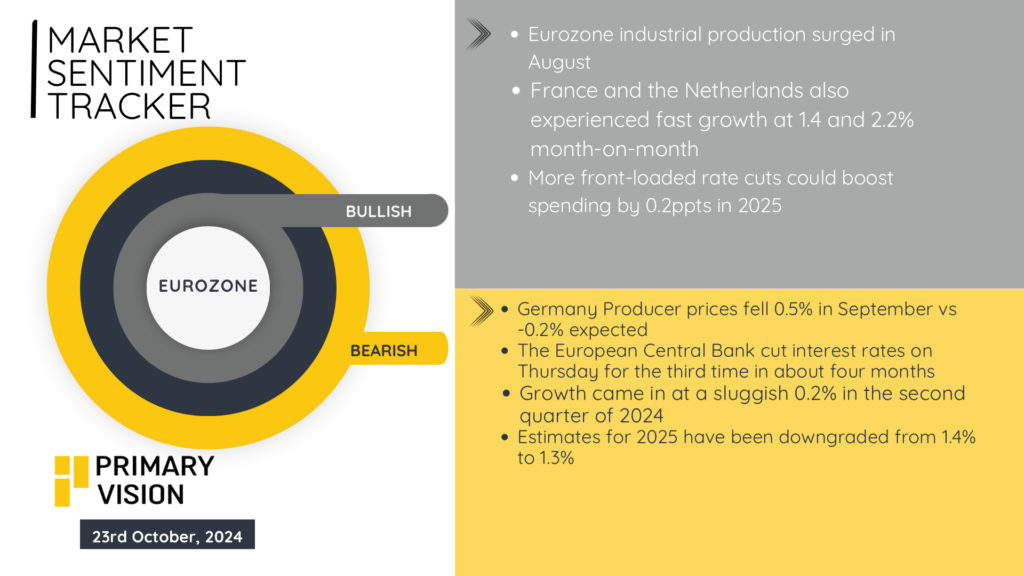

Eurozone industrial production surged in August, with France and the Netherlands showing notable growth at 1.4% and 2.2% month-on-month, respectively. Despite this uptick in output, Germany’s producer prices fell by 0.5% in September, a sharper decline than the expected 0.2%, highlighting ongoing inflationary pressures. Meanwhile, the European Central Bank cut interest rates for the third time in four months, signaling a strong focus on boosting growth amid economic fragility. Growth across the region, however, remained sluggish at 0.2% in Q2 2024, and estimates for 2025 have been downgraded from 1.4% to 1.3%, indicating that while short-term measures such as rate cuts may boost spending, the broader outlook remains tepid. The potential for front-loaded rate cuts to add 0.2 percentage points to 2025 spending suggests cautious optimism, but economic recovery across the region still faces significant headwinds, particularly in terms of sustaining price stability and industrial momentum.