A Slowdown Expected In Q4: NINE Energy’s (NINE) financial results improved in Q3. But, its management expects revenue and profitability to decline in Q4. Typical headwinds like budget exhaustion, adverse weather, and holiday slowdowns can contribute to the sales slowdown in Q4. However, improved commodity prices and resetting of customer budgets can result in moderate activity pick-up in 2025. The company has a strategy of providing an asset-light business and will focus on increasing profitability in the medium term. Read more about this in our recent article here.

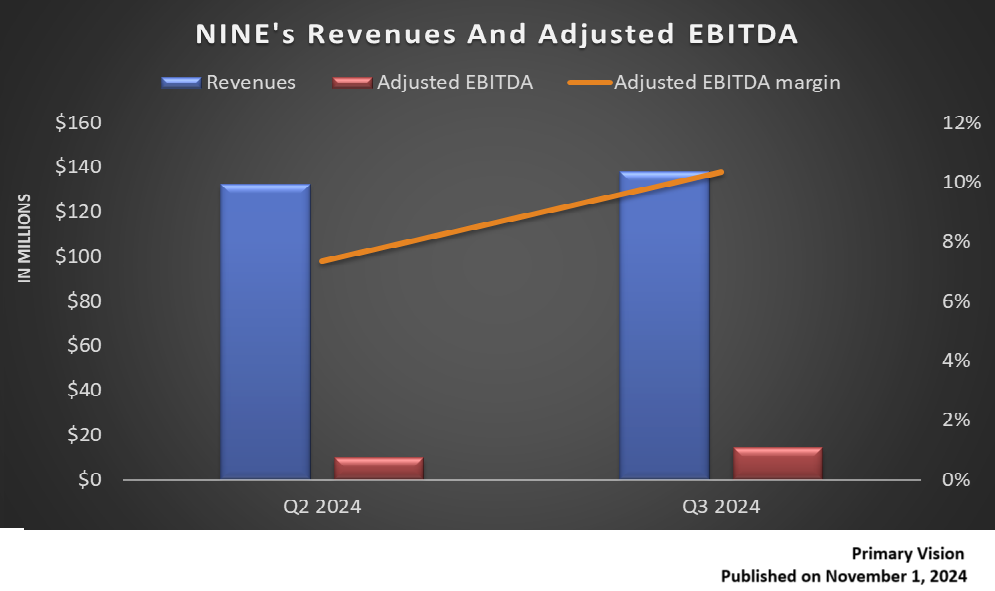

Revenue And EBITDA Margin Recovered In Q3: Quarter-over-quarter, NINE’s revenues increased by 4.3% in Q3, while its adjusted EBITDA margin expanded by ~300 basis points. Lower rig count adversely affected NINE’s performance in Q3. Despite that, the cementing business outperformed its other operations, increasing by 12% during Q3. Also, better utilization, increased international tool sales, and cost-saving initiatives led to the topline and EBITDA margin expansion in Q3. On the other hand, low natural gas prices kept activity levels in Northeast and Haynesville low.

Negative Cash Flows And Equity: NINE’s cash flow from operations turned negative in Q3 compared to a positive CFO a quarter ago. As a result, free cash flow also turned negative in Q3. Due to negative shareholders’ equity, its debt-to-equity remained negative as of September 30, 2024. During Q3, it repurchased shares worth $1.4 million. Negative cash flows, a high net debt ($303 million), and negative equity render the stock financially risky.

Thanks for reading the NINE Take Three, designed to give you three critical takeaways from NINE’s earnings report. Soon, we will present a second update on NINE earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.

Premium/Monthly

————————————————————————————————————-