Below-par Expectations For Q4: In Q4, ProFrac (ACDC) expects to see its pricing and activity in the Stimulation Services segment deteriorate. However, additional integrated frac spread deployments and increased demand for electric and Tier 4 dual fuel (or DGB) frac spreads can lead to a recovery in Q1 2025. The Proppant Production segment, which was the worst hit in Q3 following the weakness in natural gas activity in West Texas, can continue to see pricing and volume shrinkage in Q4. Nonetheless, the company’s cost management initiatives can deliver a slightly better profit performance in 2025, particularly in crude oil-heavy regions.

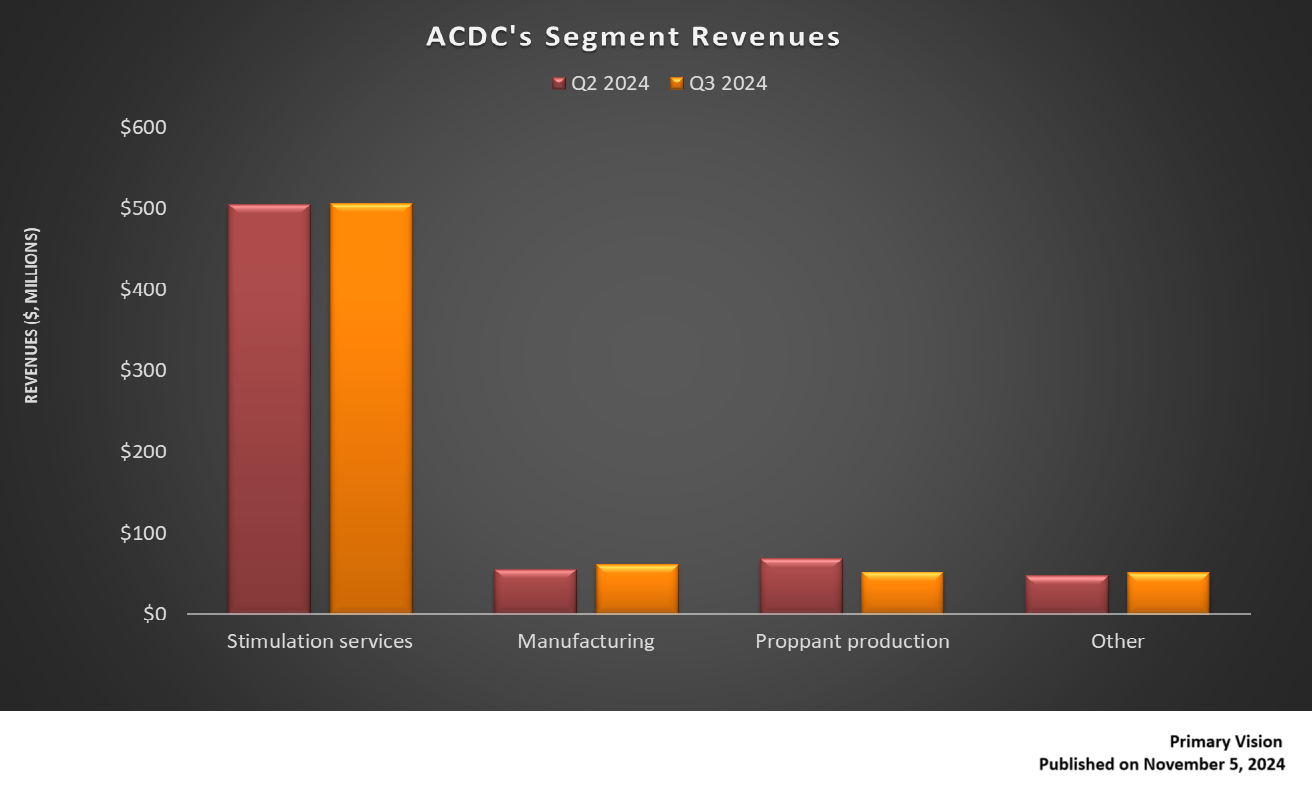

Segment Performance In Q3: From Q2 to Q3, ACDC’s revenues from the Manufacturing and Other segments increased (10% and 8% up, respectively), while its revenues from Proppant Production decreased significantly (24% down). Revenues from Stimulation Services remained unchanged. Quarter-over-quarter, the company’s adjusted EBITDA margin remained steady in Q3. Despite the weakness in completion activity in the US, ProFrac maintained a steady state due to its strong completion value chain and increased efficiency per active frac spread. Read more about ACDC in our recent article here.

Cash Flows Fell In 9M 2024: The company’s free cash flow declined steeply in 9M 2024 over a year ago due to a substantial cash flow from operations decline. In 9M 2024, its capex also fell. Its projected growth capex for FY2024 is $100 million, which it plans to spend on frac fleet upgrades, investments in next-generation technologies, and sand mine improvements.

Thanks for reading the ACDC Take Three, designed to give you three critical takeaways from ACDC’s earnings report. Soon, we will present a second update on ACDC earnings highlighting its current strategy, news, and notes we extracted from our deeper dive.

Premium/Monthly

————————————————————————————————————-