The global oil market is entering 2025 with significant challenges. Analysts are increasingly bearish, citing a surplus supply, tepid demand growth, and rising geopolitical tensions. The outlook for Brent crude prices hovers in the low $70s per barrel, down from an average of $80 this year, reflecting a market grappling with both structural and cyclical shifts. OPEC+ has delayed the easing of its voluntary production cuts until April 2025, but even this cautious strategy may not be enough to offset the broader headwinds.

The OPEC+ decision to extend production cuts reflects the group’s recognition of fragile market conditions. The cuts, initially planned to begin unwinding in January 2025, have been deferred to the second quarter, with a phased approach lasting until September 2026. However, the International Energy Agency (IEA) forecasts a supply surplus of 950,000 barrels per day (bpd) next year, even if these cuts remain in place. If OPEC+ follows through with its plan to gradually lift output starting in April, the surplus could swell to 1.4 million bpd. Such an imbalance underscores the growing gap between supply and demand fundamentals.

Source: December Oil Market Report, IEA

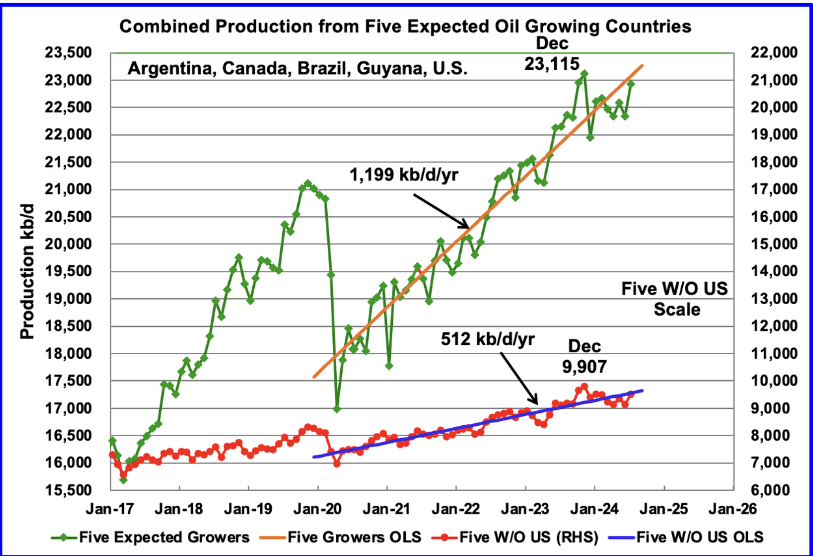

On the demand side, the picture is equally uninspiring. The IEA predicts global oil demand will rise by 1.1 million bpd in 2025, a relatively modest gain compared to historical averages. This forecast has been steadily revised downward, driven largely by China’s lackluster economic recovery. Despite Beijing’s efforts to stimulate growth through monetary easing and targeted fiscal measures, consumer and industrial activity remains subdued. Compounding the issue is the structural shift toward renewable energy and electric vehicles, which continue to erode long-term demand for fossil fuels. Non-OPEC production growth exacerbates these challenges. The United States, Brazil, and Guyana are expected to lead the supply increase, collectively adding significant volumes to the market. U.S. shale producers, in particular, continue to defy expectations, with output climbing to record levels despite cost pressures and environmental scrutiny. This influx of non-OPEC supply not only threatens to overwhelm the market but also undermines OPEC’s ability to dictate price dynamics effectively.

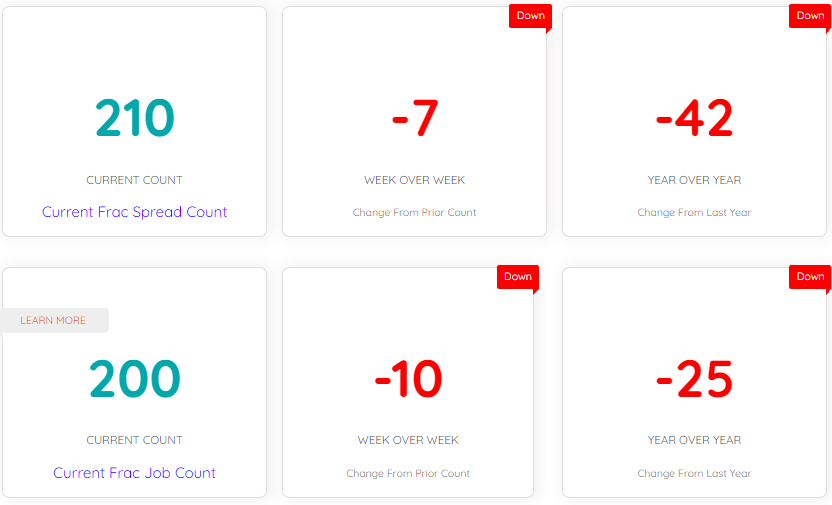

The U.S. Energy Information Administration (EIA) forecasts that Brent prices will average $74 per barrel in 2025, down slightly from its previous estimates. The agency anticipates inventory builds throughout the year, particularly in the latter half, which will likely exert further downward pressure on prices. We at Primary Vision echo this sentiment, noting that inventory surpluses and strong non-OPEC supply growth will outweigh the impact of OPEC+ production policies. It is important to learn that our Frac Spread Count is falling but the production is still stable – this speaks about the country’s technological dividend about which we shall discuss in a separate article.

Geopolitics adds another layer of complexity to the market. The incoming Trump administration has proposed sweeping trade tariffs, with rates as high as 60% on Chinese imports and 25% on goods from Canada and Mexico. Such measures could disrupt global trade flows, depress industrial activity, and weigh heavily on oil demand. Additionally, uncertainties surrounding Trump’s foreign policy, particularly in the Middle East, could lead to unforeseen supply disruptions or shifts in alliances that ripple across energy markets. The potential for heightened tensions with Iran or policy shifts in the Russia-Ukraine conflict only adds to the murkiness of the outlook.

China remains another critical variable. While recent stimulus measures have provided a temporary lift, the country’s long-term growth trajectory is clouded by structural challenges, including high debt levels and an aging population. Should Chinese demand falter further, the impact on global oil markets would be profound, given its status as the world’s largest crude importer. Analysts have flagged the risk of escalating U.S.-China trade tensions, which could further dampen economic activity and, by extension, oil consumption.

As such OPEC+ finds itself in a precarious position. While the group’s cautious approach to managing supply has helped stabilize prices in the short term, it faces mounting pressure from both internal and external factors. Member states are grappling with fiscal deficits and the need to fund ambitious energy transition plans, while the rise of non-OPEC supply threatens to erode their market share further. The delicate balance between supporting prices and maintaining competitiveness will likely dominate discussions within the group in the months ahead. Analysts are not ruling out wildcards that could disrupt the current trajectory. A potential escalation in the Middle East, stricter U.S. sanctions on Iran, or a major supply disruption could quickly shift the balance in favor of higher prices. Conversely, a sharper-than-expected slowdown in China or an escalation of trade wars could deepen the bearish outlook. The market’s inherent volatility, coupled with these uncertainties, ensures that forecasting oil prices will remain a fraught exercise.

As the global oil market heads into 2025, the interplay of supply dynamics, geopolitical risks, and economic uncertainty creates a challenging environment for both producers and consumers. While OPEC+ continues to wield significant influence, the group’s ability to stabilize prices in the face of mounting headwinds will be tested. For now, the consensus remains cautious, with prices likely to hover in a narrow range, reflecting the delicate balance between optimism and apprehension.