The U.S. shale sector will be subject to many developments as the gap between the policy direction of the current U.S, administration and the upcoming one along-with the priorities of the industry itself combined with the wider geopolitical and economic factors will make up for an exciting 2025. In recent months, the sector has displayed a remarkable ability to adapt to changing circumstances, although challenges such as depletion, policy changes, and evolving market demands loom large. With President-elect Donald Trump set to assume office and the Biden administration exiting with restrictive energy policies, the shale sector faces a pivotal juncture. The top three priorities are: balancing production discipline, shareholder priorities, and innovation.

The shale industry has evolved significantly since its explosive growth phase in the 2010s. While it benefited from technological advancements and high oil prices during that period, it also endured a downturn in 2020 that forced a fundamental restructuring. Today, the focus has shifted from unbridled expansion to disciplined growth and capital efficiency. Large public companies dominate the sector, following years of consolidation that saw major players like ExxonMobil and Chevron acquiring smaller operators and securing vast resources in prolific basins such as the Permian.

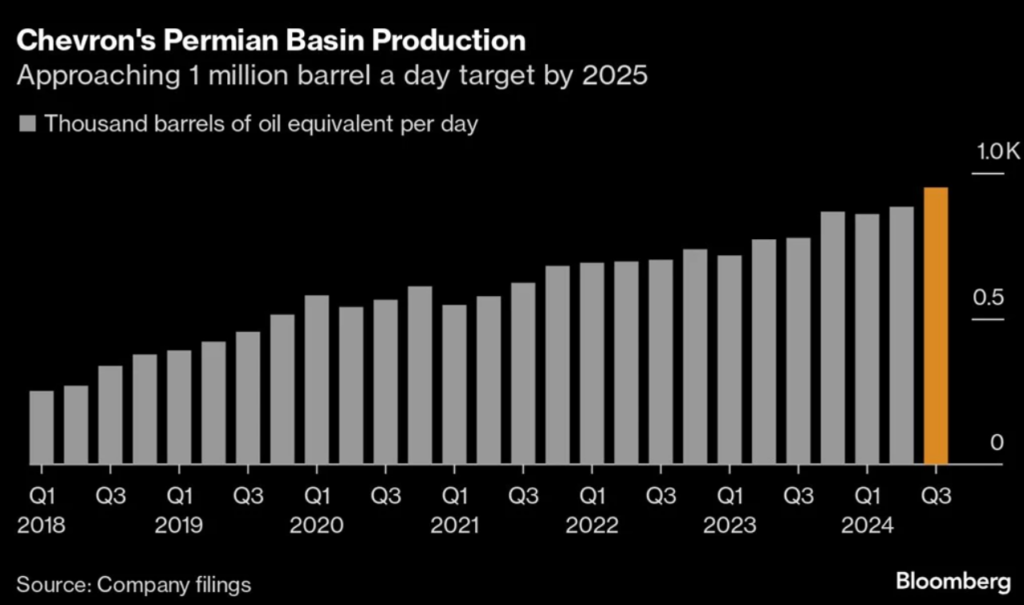

This consolidation has fundamentally altered the industry’s approach to drilling. Unlike the “drill, baby, drill” mantra that defined shale’s earlier years, today’s producers prioritize shareholder returns and stable financials. For example, Chevron recently announced that its 2025 capital expenditure for the Permian Basin would be lower than in 2024, signaling a deliberate approach to managing resources and optimizing profitability. Similarly, ExxonMobil executives have emphasized that explosive production growth is not part of their strategy, aligning instead with economic prudence.

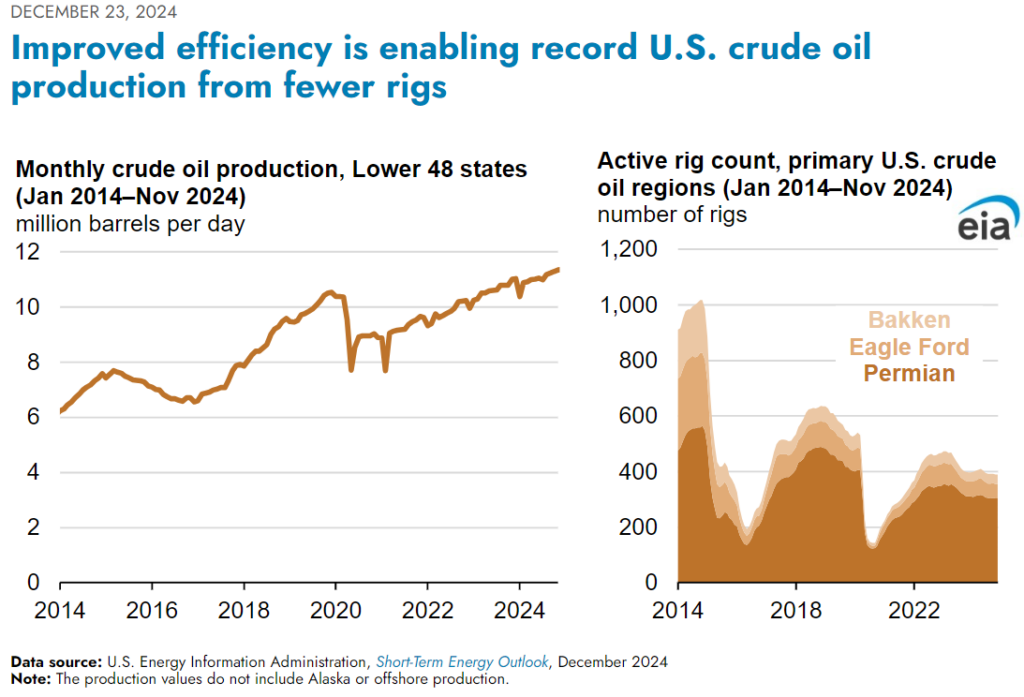

The consolidation and financial discipline are underscored by advances in technology and operational efficiency. According to the Energy Information Administration (EIA), productivity in shale wells has improved significantly, allowing producers to achieve higher output with fewer rigs. These efficiency gains help sustain production even as the active rig count declines. However, the emphasis on efficiency does not obscure the reality of resource depletion. Shale crude oil and dry gas production both peaked in late 2023, and output has since declined marginally. This trend highlights the natural limits of shale reservoirs and the need for enhanced recovery techniques.

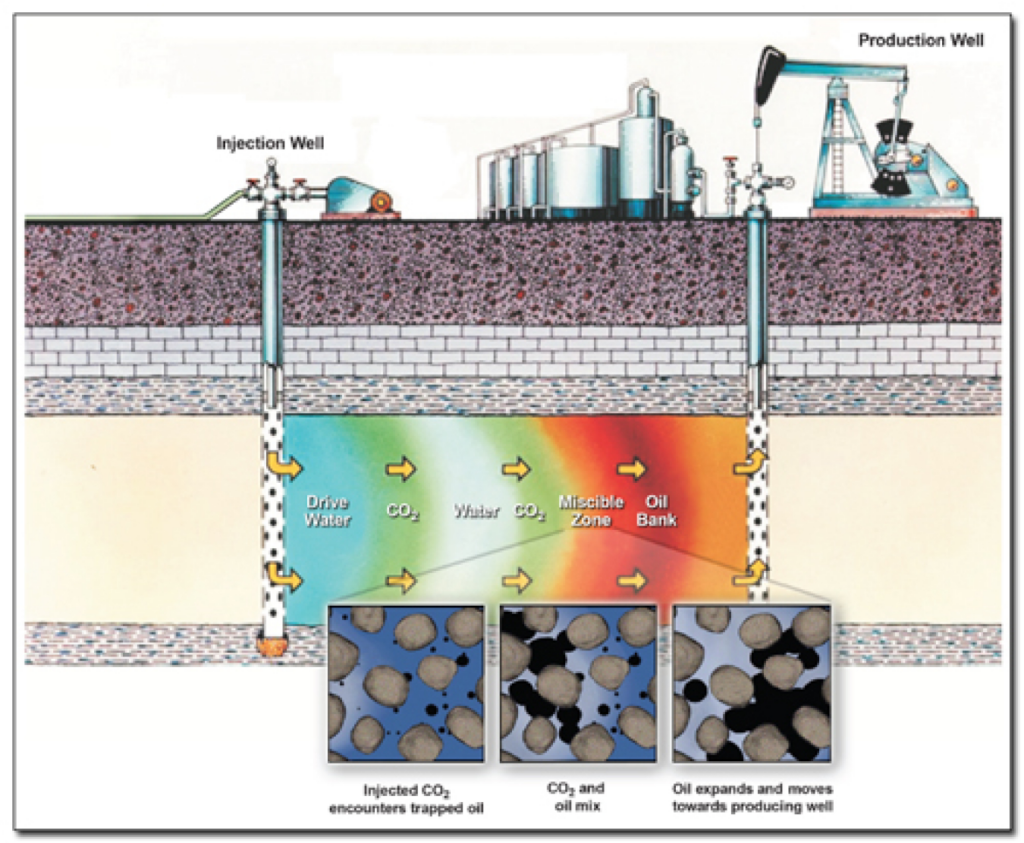

Depletion has become a growing concern for the sector. Historically, shale production followed three distinct phases: primary, secondary, and tertiary recovery. While primary and secondary techniques have extracted a significant portion of oil in place, tertiary methods, such as CO2 injection, are increasingly necessary to unlock remaining reserves. The Department of Energy estimates that next-generation CO2-enhanced oil recovery (EOR) technologies could recover more than 60 billion barrels of oil. While promising, these methods are capital-intensive and demand significant investment, underscoring the delicate balance between maintaining production and managing costs.

The policy environment further complicates the outlook for shale. President Joe Biden, in his final weeks in office, has enacted measures to permanently protect certain U.S. coastal waters from offshore drilling. This move aims to safeguard marine ecosystems but poses challenges for the incoming administration, which has signaled support for expanding domestic energy production. These policy swings create uncertainty for shale operators, who must navigate shifting regulations while maintaining their commitments to shareholders and stakeholders.

The Permian Basin remains the epicenter of U.S. shale production, accounting for significant contributions to both crude oil and natural gas output. Yet even this prolific region is not immune to the challenges of resource depletion and rising operational costs. Goldman Sachs projects that growth in Permian crude production will slow to 4% by 2026, reflecting a more measured pace of expansion compared to the explosive growth of prior years. This deceleration underscores the industry’s pivot toward sustaining production through technological innovation and efficiency gains.

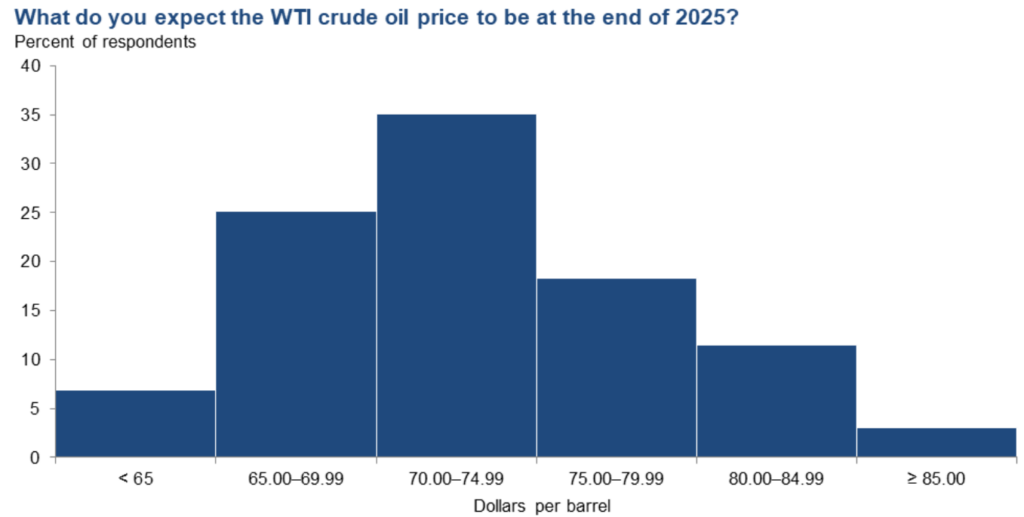

Despite these challenges, there are reasons for cautious optimism. The Dallas Federal Reserve’s latest energy survey indicates a slight uptick in business activity within the oil and gas sector, with firms expressing mild optimism about future conditions. Respondents expect West Texas Intermediate (WTI) crude prices to average $71 per barrel by the end of 2025, reflecting stability in market expectations. However, natural gas prices are anticipated to remain subdued, with long-term projections hovering around $3.63 per million British thermal units (MMBtu).

In this evolving landscape, technological innovation will play a pivotal role in shaping the future of shale. Advances in drilling and completion techniques, such as expandable casing patches and enhanced recovery methods, offer opportunities to optimize production and extend the lifecycle of existing wells. These innovations are particularly critical as operators contend with ageing wells and challenging reservoir conditions. Shale operators are also acutely aware of the need to align with broader sustainability goals. By improving recovery rates in existing fields, the industry can reduce the need for new drilling, thereby minimizing its environmental footprint. Moreover, efforts to integrate cleaner technologies, such as carbon capture and utilization, position shale as a transitional energy source in a decarbonizing world.