Near And Long Term Drivers

We have already discussed Baker Hughes’s (BKR) Q4 2024 financial performance in our recent article. Here is an outline of its strategies and outlook. In 2025, a number of challenges await BKR, including lower growth in European and Chinese economies and geopolitical uncertainties. On the other hand, the demand spurt would emanate from higher power consumption, which would accelerate natural gas and LNG demand. This would stimulate demand for its natural gas-levered products and solutions.

BKR maintained its estimate of 800 MTPA of liquefaction capacity by 2030 in LNG and 100 MTPA of FIDs between 2024 and 2026. Project FIDs would increase from 17 MTPA in 2024 to 80 MTPA in 2025 and 2026. In gas infrastructure projects, it booked orders for MGS (master gas systems) and Jafurah (unconventional gas field) in Saudi Arabia, Hassi R’Mel in Algeria, and the Margham Gas Storage Facility in Dubai. It has pipeline expansion projects in the Middle East, Africa, North America, and Latin America.

In the energy efficiency and decarbonization technologies initiatives, BKR targets $1.4 billion—$1.6 billion of new energy orders in 2025. The company is excited about net power and direct air capture solution Mosaic. By 2030, it expects the target to soar to $6 billion—$7 billion. In the short term, however, the political uncertainties regarding clean energy policies will remain.

International Drivers And Challenges

In the international markets, BKR expects “reduced activity levels” in some regions, except Brazil, some parts of the Middle East, and Sub-Sahara in Africa. Offshore, it sees a steady outlook for subsea trees and FPSOs. SSPS (Subsea Production Systems) orders can rise following strong subsea tree order flow.

Global upstream spending on crude oil can decline slightly in 2025. In North America, spending is anticipated to decrease by a “mid-single-digit range” due to operators’ capital discipline and optimization of their newly consolidated acreage. However, BKR can outperform in North America due to its production-weighted portfolio mix.

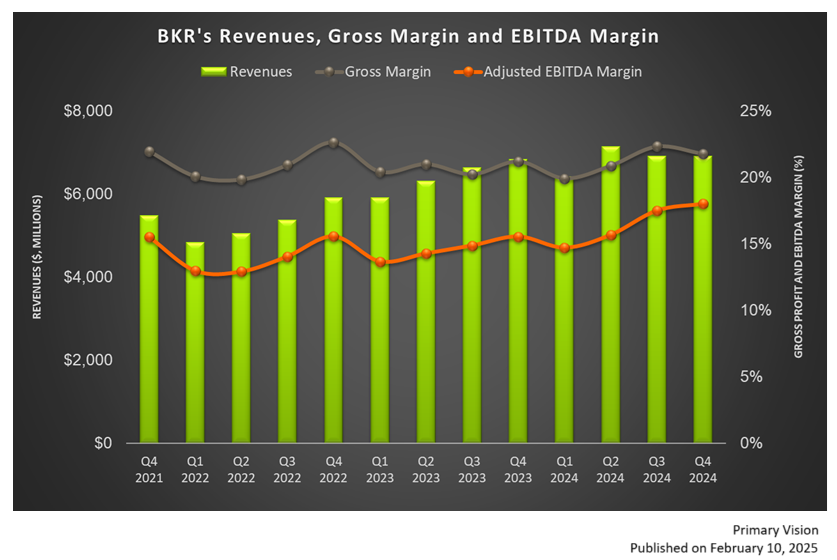

Some of BKR’s near-term challenges include capacity reduction in Saudi Arabia and the LNG moratorium in the United States. So, it expects its revenues to decrease by 11.7% in Q1 2025 compared to Q4 2024.

Segment Forecast

In IET, it expects that adjusted EBITDA will decrease by 28% quarter-over-quarter. The factors that will affect BKR are backlog conversion in GTE, aero-derivative supply chain tightness and gas technology, operational execution in industrial technology, and changes in foreign exchange. In OFSE, its adjusted EBITDA can decline by 14.6% due to seasonal decline for international OFS and SSPS.

Q4 Financial Results

As discussed in the Q4 short article, In the IET segment, revenues increased by 19% quarter-over-quarter, driven primarily by Gas Technology. Operating profit went up by 23% in Q4. Revenues in the Oilfield Services & Equipment segment were relatively weak in Q4. It also expects “2025 to demonstrate another strong year of EBITDA growth, led by our IET segment.”

BKR’s cash flow from operations increased by 9% in FY 2024 compared to a year ago. Debt-to-equity (0.35x) as of December 31, 2024, improved compared to a year ago.

Relative Valuation

Baker Hughes is currently trading at an EV/EBITDA multiple of 10.9x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 10.1x. The current multiple is slightly higher than its past five-year average EV/EBITDA multiple of 10.1x.

BKR’s forward EV/EBITDA multiple contraction versus the current EV/EBITDA is steeper than peers because the company’s EBITDA is expected to increase more sharply in the next four quarters. This typically results in a higher EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is higher than its peers’ (HAL, SLB, and FTI) average. So, the stock is reasonably valued versus its peers.

Final Commentary

Baker Hughes’s near-term outlook is fraught with the possibility of lower growth in European and Chinese economies and geopolitical uncertainties. It also expects reduced activity levels” in many international regions, including capacity reduction in Saudi Arabia and the LNG moratorium in the United States. So, the company’s financial performance can deteriorate in Q1.

Despite the challenges, the company’s management anticipates higher demand for its natural gas-levered products and solutions. It won several natural gas projects in Q4. In clean tech-initiated solutions, it expects sharp growth in net power and direct air capture solutions. As a result, its EBITDA growth can recover by the end of 2025. Also, the company’s cash flows increased in FY2024 while its leverage improved compared to a year earlier. The stock appears to be reasonably valued versus its peers.

Premium/Monthly

————————————————————————————————————-