NINE managed to hold its financial performance steady in Q4 despite the pressure in the industry. Its market share gains in cementing and cost-cutting exercises stabilized its EBITDA margin. Its management expects a steady recovery in 2025. However, its cash flows weakened in FY2024.

A Recovery Expected In Q1: NINE Energy’s (NINE) financial results remained steady in Q4. It anticipates US activity levels in 2025 to be “mostly stable.” Also, NINE’s management expects long-term demand for natural gas to increase, which should help the company’s operations as 30% of its sales are levered to natural gas basins. Despite a slow start, it expects revenue and profitability to increase sequentially in Q1. Read more about NINE’s recent past in our article here.

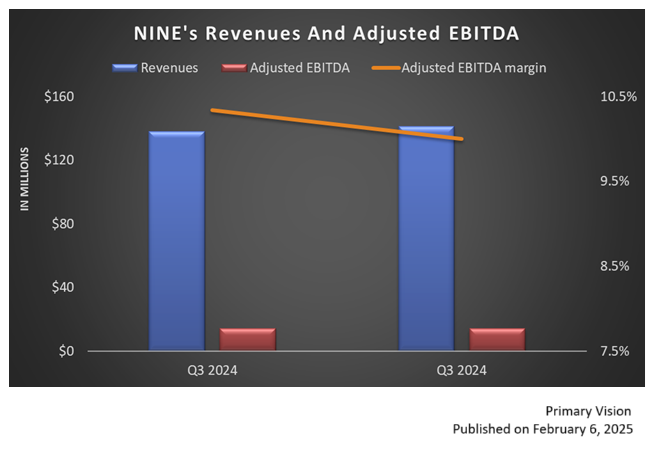

Revenue And EBITDA Margin Stabilized In Q4: Quarter-over-quarter, NINE’s revenues increased by 2.4% in Q4, while its adjusted EBITDA margin remained nearly unchanged. Despite a lower rig count in Q4, the company’s market share in cementing improved. The company’s market share gains and cost reductions led to the topline and EBITDA margin stability in Q4.

Negative Cash Flows And Equity: NINE’s cash flow from operations declined steeply (by 71%) in FY2024 compared to a year ago. As a result, free cash flow turned negative in FY2024. Due to negative shareholders’ equity, its debt-to-equity remained negative as of December 31, 2024. Negative cash flows, a high net debt ($293 million), and negative equity render the stock financially risky.

Thanks for reading the NINE Take Three, designed to give you three critical takeaways from NINE’s earnings report. Soon, we will present a second update on NINE earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.

Premium/Monthly

————————————————————————————————————-