In the intricate dance of global economics, recent developments have set the stage for both anticipation and apprehension. The Eurozone, while witnessing a modest GDP uptick, grapples with contractions in its powerhouse economies, Germany and France. China’s deflationary signals contrast with its burgeoning trade surplus, painting a complex picture of its economic health. Meanwhile, the United States faces market volatility amidst escalating trade tensions and policy shifts. These intertwined narratives prompt a critical question: Are we on the brink of a global recession, or is this merely a prelude to a resilient economic renaissance?

Eurozone

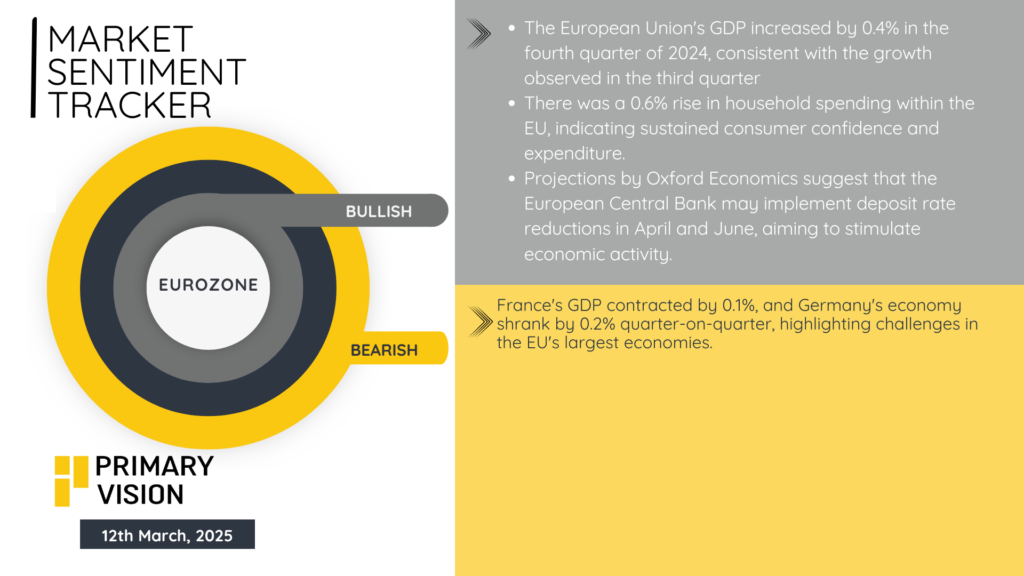

In the fourth quarter of 2024, the Eurozone’s GDP experienced a modest uptick of 0.2%, surpassing initial estimates of stagnation. This slight growth is primarily attributed to an upward revision in Ireland’s economic performance, where the economy expanded by 3.6% instead of the previously estimated contraction of 1.3%. However, this regional growth masks underlying challenges, as major economies like Germany and France faced contractions of 0.2% and 0.1%, respectively.

The European Central Bank (ECB) responded to these mixed signals by reducing interest rates by a quarter percentage point, bringing the deposit rate to 2.5%. This monetary easing aims to stimulate growth amid concerns over potential trade conflicts with the U.S. and increased defense spending within Europe. ECB President Christine Lagarde emphasized the negative impact of tariffs on economic confidence and investment decisions.

Despite these efforts, the Eurozone continues to grapple with sluggish growth, with the ECB projecting a modest 0.9% expansion for 2025, mirroring the previous year’s performance. Persistent challenges, including reduced household consumption, limited government spending, and an industrial recession, contribute to this subdued outlook.

China

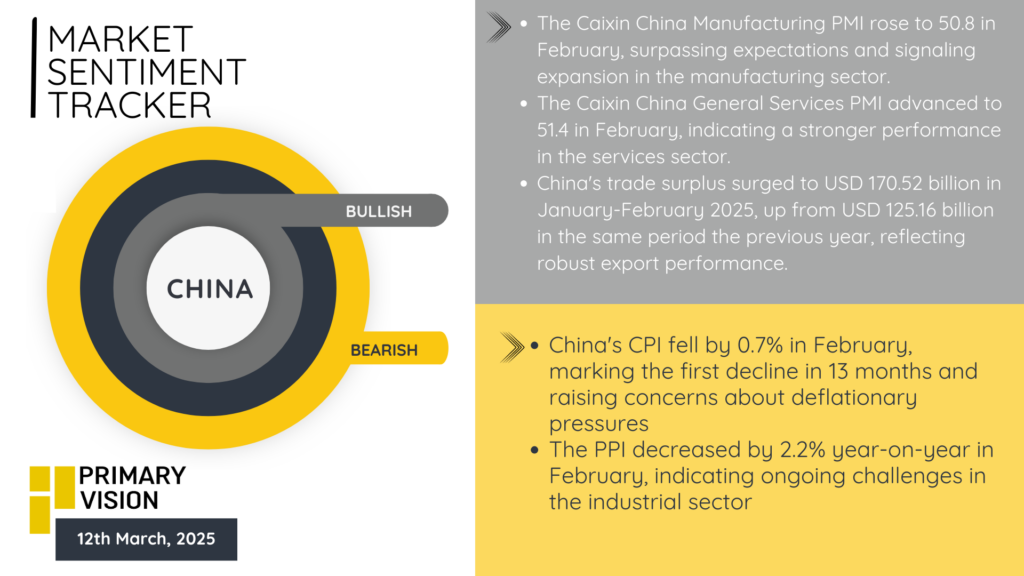

China’s economy is exhibiting signs of deflationary pressure, as evidenced by a 0.7% year-on-year decline in the consumer price index (CPI) for February, marking the first decrease in 13 months. Concurrently, the producer price index (PPI) fell by 2.2%, indicating persistent challenges in the industrial sector.

This deflationary trend is partly driven by cautious consumer behavior amid concerns over employment and income stability. Retailers are resorting to frequent flash sales and steep discounts to stimulate demand, further exacerbating price declines. Analysts warn that this shift toward value-oriented consumption could destabilize traditional retail sectors and intensify deflationary pressures.

In response, the Chinese government aims to bolster household spending and has adjusted its inflation target downward. However, high youth unemployment and job insecurity continue to constrain consumer spending, posing risks to sustained economic growth.

United States

The United States is facing increasing recessionary fears, as reflected by a significant sell-off on Wall Street. Major indices experienced notable declines, with the Dow Jones Industrial Average dropping over 2%, the S&P 500 falling by 2.7%, and the Nasdaq decreasing by 4%. Contributing factors include ongoing trade tensions, particularly China’s retaliatory tariffs on U.S. agricultural imports, and concerns over the current administration’s economic policies.

These developments have heightened investor uncertainty, leading to increased market volatility. The potential for further economic instability is underscored by the administration’s stance on trade tariffs and the possibility of a recession. Additionally, the volatility index, a measure of market fear, has risen, reflecting the growing apprehension among investors.

The global economic landscape is characterized by a mix of modest growth and significant challenges. While the Eurozone shows slight GDP growth, underlying issues in major economies and cautious consumer behavior persist. China’s deflationary trends highlight vulnerabilities in consumer demand and industrial stability. In the U.S., escalating trade tensions and recession fears are contributing to market volatility. These factors collectively underscore the need for vigilant economic policies and adaptive strategies to navigate the evolving global economic environment.