As the Permian Basin matures, operators face a more complex, cost-intensive environment. Efficiency gains remain essential, but they’re now a response to mounting challenges rather than a sign of smooth progress. The sector is being pushed—by geology, inflation, regulation, and consolidation—into a phase that demands more precision, more capital discipline, and more adaptability.

Recent studies have shown that the average gas-to-oil ratio in the Permian has started to climb steadily, from around 3,100 cubic feet per barrel in 2014 to nearly 4,000 cf/b as of early 2025. At the same time, water cuts are trending higher. Water-to-oil ratios, particularly in wells older than 18 months, now exceed 3:1 in much of the Midland Basin, up from an average of 2.1:1 in 2017. Operators are stepping outside of the Tier 1 rock that underpinned the early boom and into formations that are more gas- and water-prone. This shift could easily be seen as a warning sign—the beginning of resource exhaustion—but in reality, it’s forcing a wave of innovation.

However, innovation comes with its own challenges. This geological decline is forcing a heavier reliance on well design (which continues to evolve) to preserve returns. Average lateral lengths in the Midland Basin now exceed 10,000 feet, up from roughly 7,500 in 2018. Each additional 1,000 feet of lateral can boost estimated ultimate recovery by 15–20% in high-quality zones, but those gains don’t come easy. Managing torque and drag, maintaining wellbore stability, and geosteering through narrow targets require more sophisticated equipment and real-time systems. Rotary steerables, smart bits, and telemetry platforms are now a core part of the drilling toolkit. But companies are improvising: Ovintiv is achieving better results with its trimul-frac design, doubling daily completed footage and lowering per-foot costs by 15%. Devon Energy used AI-based bit optimization to improve drilling speeds by 18% in the last year alone. However, only around 30% of operators in the Permian are deploying these advanced digital tools at scale. Smaller independents continue to operate with limited real-time data, older rigs, and fewer automation options. The result is a widening performance gap—and a consolidation of technical advantage in fewer hands.

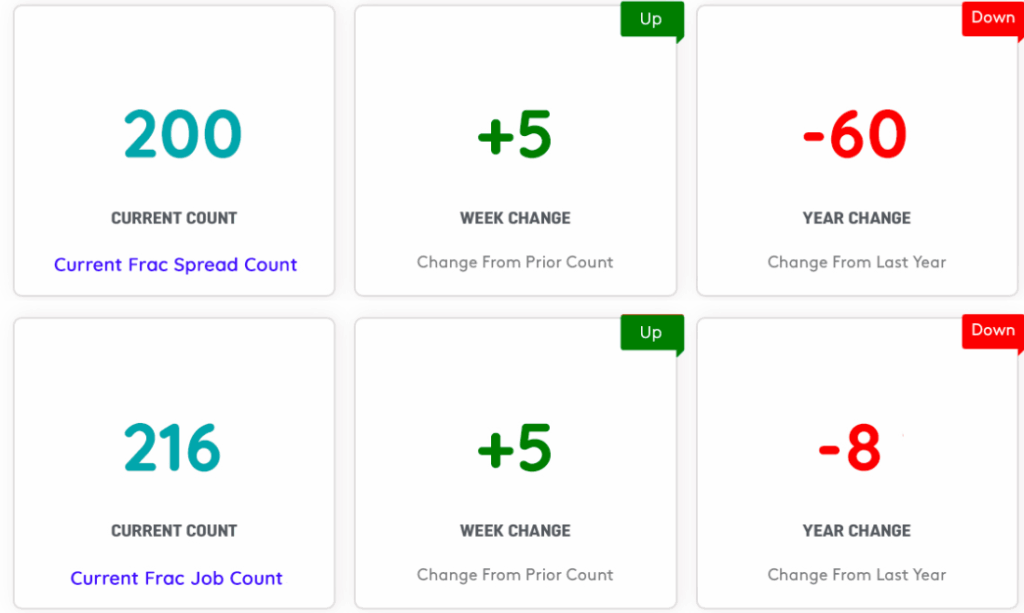

The technological improvements manifest in the recent FSC and FJC numbers. Despite the sell-off we see that both the metrics registered a gain of 5 but FSC is significantly down on YoY basis whereas FJC seems to be holding strong.

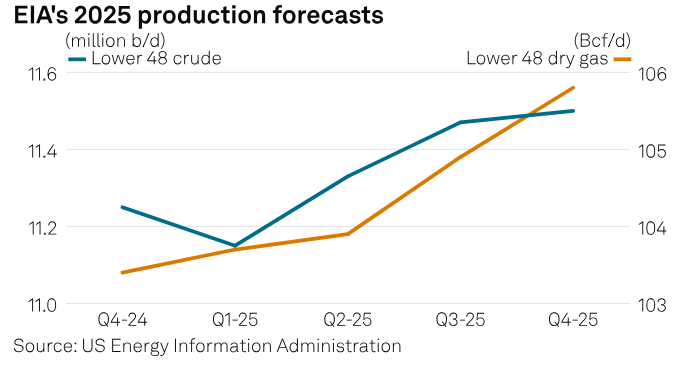

But beyond engineering gains, there’s a another structural issue taking shape: the quality of remaining inventory. Several large operators, including Pioneer and Diamondback, have openly acknowledged they are shifting into Tier 2 acreage. The implication is that more wells will be required to deliver the same volume of oil—and each well will be more technically demanding. In this context, efficiency isn’t optional; it’s existential. Costs are also rising again. Service costs per well are projected to climb 2.8% in 2025, reversing a brief drop in 2024. Diesel prices, which account for 10–15% of total frac fleet OPEX, remain elevated. The 25 % tariff on imported steel and the 10 % levy on specialized drilling equipment imposed in early April 2025 are already adding several dollars to well breakevens just as WTI hovers near $63 a barrel. With most shale producers needing $60–71 to justify new drilling, the margin for error is evaporating. Baker Hughes recorded the sharpest weekly rig decline since mid‑2023, and the International Energy Agency trimmed its 2025 shale‑growth outlook by 300,000 bpd the largest in recent 5 years. Boards, faced with higher input costs and price volatility, are slowing investment decisions—especially for longer‑cycle projects whose economics depend on stable margins. Wood Mackenzie now counts more than sixty large upstream FIDs that were slated for 2025–26 but are drifting to the right as executives wait to see whether tariffs, trade policy, and macro uncertainty ease. The risk is a policy‑driven supply crunch later in the decade—a time lag today that becomes tightness tomorrow.

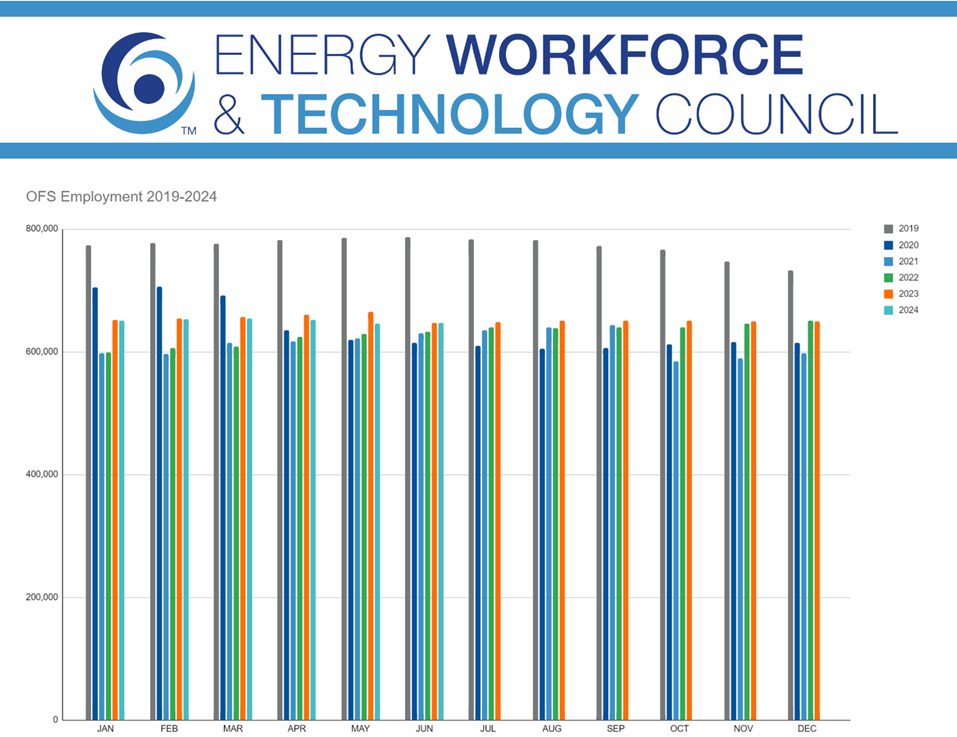

The Permian Basin’s oil and gas sector is also grappling with significant hiring and retention challenges as it enters 2025. Despite a robust labor market—evidenced by Midland County’s low unemployment rate of 2.8%—employers face a persistent talent gap. Employers say that the region sees an influx of underqualified candidates for specialized roles, while overqualified professionals often hesitate to apply due to perceived mismatches in work expectations and compensation. Compounding the issue, rising housing and living costs in Midland and Odessa deter potential candidates from relocating to the area. According to an analysis 16,000 employers in the oil and gas services sector, many of whom struggle to find technical expertise in fields like petroleum, electrical, and mechanical engineering.

The regulatory environment is becoming more burdensome as well. New EPA methane regulations enacted in January 2025 require continuous leak monitoring and quarterly inspections for all sites producing more than 3 barrels of oil equivalent per day. Compliance costs for mid-sized operators are estimated at $70,000–$110,000 annually per field, depending on monitoring technology. The SEC’s climate disclosure rule, which mandates Scope 1 and Scope 2 emissions reporting, is adding additional administrative overhead. Operators must now factor emissions intensity into development planning, procurement, and investor guidance. These requirements are disproportionately burdensome for private operators and non-majors, who lack the ESG infrastructure to comply without significant restructuring.

Success in Shale will now come down to a few clear moves: use data and automation on every well, spend only on projects that still make good money in tougher rock, build a workforce and supply chain that can handle labor shortages and higher costs, and treat methane limits and other climate rules as basic operating rules, not extras. Companies that do these things quickly will keep pumping profitably; those that stick with old habits will watch thinner rocks, higher bills, and tighter regulations squeeze them out—no matter what oil prices do.