As oil markets brace for volatility in 2025, OPEC+ members are finding it hard to comply to production limits. While the issue of non-compliance may appear simple, the reality is far more complex. Take example of two chronic over producers, Kazakhstan and Iraq. Their overproduction simply doesn’t correspond to their non-compliance but is symptomatic of internal political pressures, structural constraints, and strategic imperatives that make OPEC+ discipline difficult, if not impossible, to uphold. Their actions pose serious questions for the future of the alliance, and for global oil price stability.

Iraq: A Fractured State Dependent on Oil

Iraq’s persistent overproduction is rooted in its extreme fiscal dependence on oil revenues and a fragmented internal political structure. According to the IMF, Iraq needs oil prices above $92 per barrel to meet its budgetary obligations—a figure that highlights how tightly public sector spending is tethered to oil exports. With over 90% of government revenue coming from hydrocarbons, any dip in prices forces Baghdad to ramp up production just to sustain its current expenditure levels.

However, the bigger complication is Iraq’s lack of centralized control over its own oil sector. The semi-autonomous Kurdistan Regional Government (KRG) in northern Iraq operates under a 2007 regional oil and gas law, which allows it to negotiate independently with international oil companies and export crude without Baghdad’s approval. Despite a 2022 ruling from Iraq’s Federal Supreme Court declaring this law unconstitutional, the KRG has resisted compliance, defending its legal autonomy. In 2023, the International Chamber of Commerce ruled in favor of Baghdad, ordering Turkey to stop facilitating KRG exports via the Iraq-Turkey pipeline and to pay $1.5 billion in damages. This temporarily suspended Kurdish exports, but by 2025, negotiations remain stalled over revenue sharing, cost recovery, and the status of production-sharing contracts. As of April 2025, Kurdish oil exports have not resumed, depriving both Erbil and Baghdad of critical income and further pushing Iraq’s federal government to maximize production elsewhere.

Thus, Iraq’s overproduction is not just opportunistic—it’s an institutional response to fragmented sovereignty, budgetary fragility, and legal deadlock. With no easy path to a unified oil policy, Iraq’s non-compliance with OPEC+ is almost baked into the system.

Adding to this complexity is Iraq’s fragmented bureaucracy, where overlapping institutions and ministerial turf wars complicate quota enforcement. The Ministry of Oil, State Organization for Marketing of Oil (SOMO), and regional authorities often have differing interests, resulting in data discrepancies and weak quota discipline.

Kazakhstan: Strategic Defiance Backed by Foreign Capital

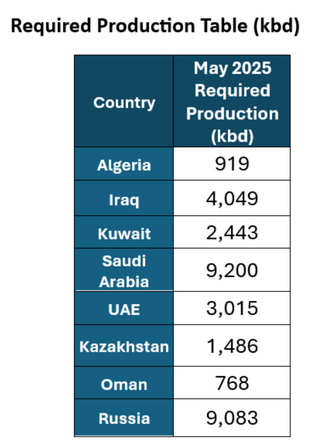

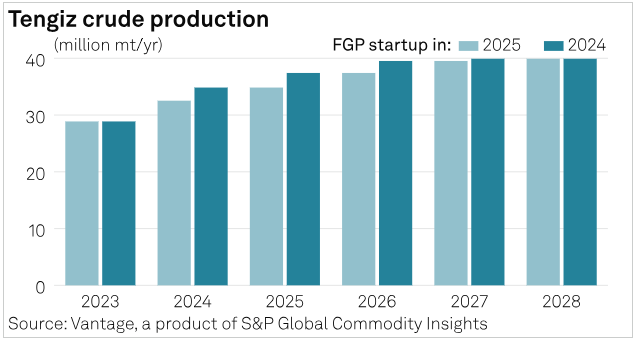

Kazakhstan’s overproduction, by contrast, stems less from crisis and more from calculation. In April 2025, Kazakhstan produced around 1.814 million barrels per day, well above its OPEC+ quota of 1.473 million bpd. The excess supply is primarily driven by the expansion of the Tengiz oil field, operated by Chevron and ExxonMobil. Because these mega-projects operate under rigid production-sharing agreements (PSAs), the Kazakh government has limited ability to reduce output – at least from its three large oil projects – without renegotiating complex contracts—an economically and politically costly endeavor.

Moreover, Kazakh authorities have openly signaled a shift in posture. Energy Minister Erlan Akkenzhenov stated in April that national interests would take precedence over OPEC+ commitments, a message clearly aimed at preserving momentum for domestic growth. This policy is rooted in broader national priorities: Kazakhstan’s 2025 Development Plan emphasizes infrastructure development, economic diversification, and regional gasification projects, many of which are financed directly or indirectly through oil revenue.

It is important to note that Kazakhstan has also started positioning itself as a stable, investor-friendly alternative to riskier oil jurisdictions like Libya or Venezuela. Overproduction, in this context, is not just revenue-maximizing—it’s signaling to foreign investors that Kazakhstan is a dependable long-term producer, even in a quota-bound environment.

While oil contributes about 26% of government revenue, it funds a disproportionate share of capital-intensive state projects. In 2024 alone, over 193 billion tenge was allocated to regional gas infrastructure projects, much of it sourced from energy sector gains. Furthermore, oil and gas account for nearly 75% of Kazakhstan’s exports, making the sector central to the country’s balance of payments and foreign exchange reserves. Furthermore, Kazakhstan’s centralized political system affords its leadership greater latitude to prioritize long-term economic objectives, such as sustaining elevated oil production levels, even if this approach leads to short-term diplomatic tensions within OPEC+. This contrasts with more pluralistic political systems, where domestic political pressures and public scrutiny can constrain such decisions

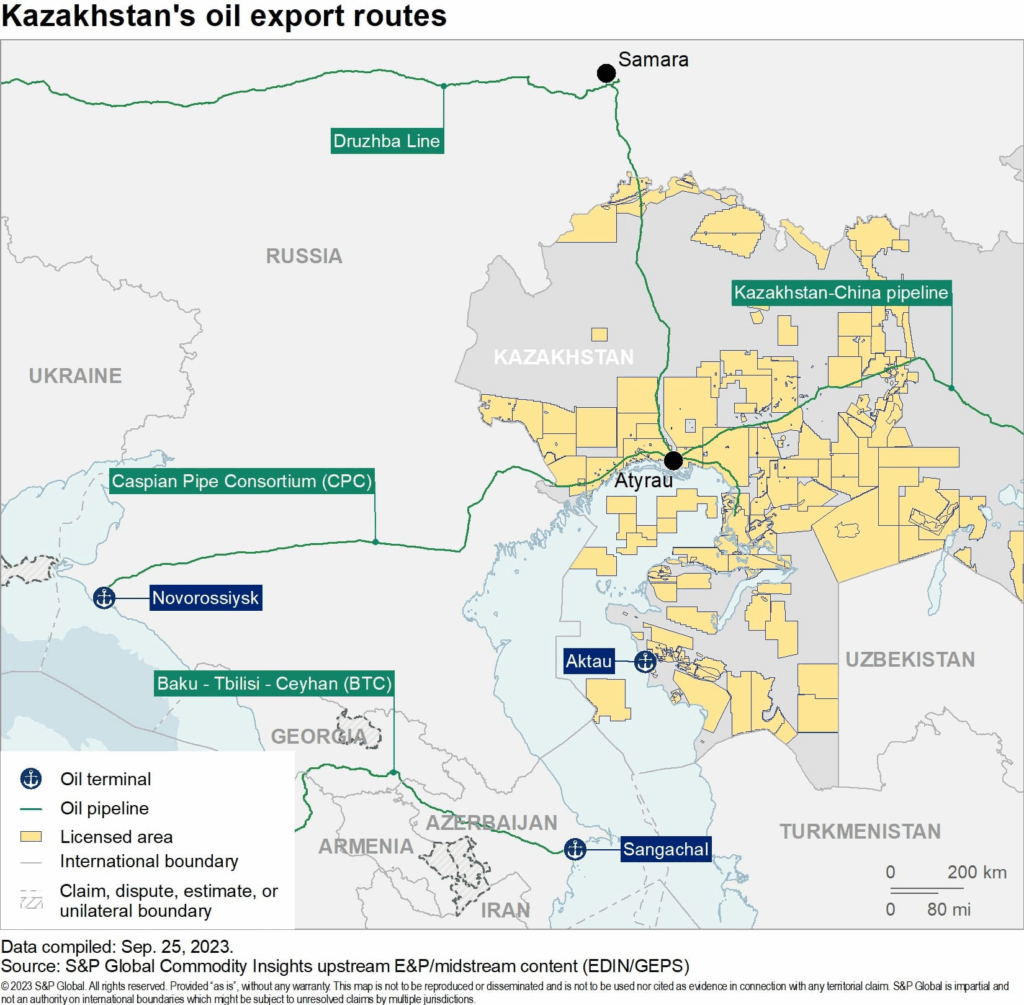

Finally, geopolitical constraints compound the picture. Kazakhstan depends heavily on the Caspian Pipeline Consortium (CPC) to export oil via Russia’s Black Sea coast. Disruptions to this pipeline—due to inspections, drone strikes, or diplomatic tensions—have threatened to choke off exports, compelling Kazakhstan to pump more oil when possible to hedge against future bottlenecks. Kazakhstan’s continued overproduction reflects a deliberate balancing act in its energy policy. The state is navigating a complex combination of foreign-operated oil projects, limited export infrastructure, and a development strategy that depends heavily on hydrocarbon revenues. These pressures make strict alignment with OPEC+ quotas less about compliance and more about managing structural constraints.

What can be the implications?

The actions of Iraq and Kazakhstan expose a growing fault line within OPEC+. While countries like Saudi Arabia continue to push for disciplined output management to stabilize prices, others are finding compliance increasingly incompatible with domestic imperatives. What makes Iraq and Kazakhstan especially significant is not just the scale of their overproduction, but the legitimacy of their motivations—from political autonomy to economic resilience and export security.

This divergence in behavior points to a broader shift within OPEC+. What was once a more coordinated group of oil producers now resembles a coalition of sovereign states with differing economic priorities, legal structures, and geopolitical interests. As the group prepares for its next production review in May 2025, the key question is less about enforcement and more about whether OPEC+ can continue to function as a coherent and credible player in global energy governance.

Will Other OPEC+ Members Follow the Same Path?

The short answer is: some already are, and more may follow.

Several smaller or economically strained OPEC+ members—such as Nigeria, Angola, and Iran—have periodically overproduced or skirted compliance altogether. In Nigeria’s case, chronic underinvestment in upstream infrastructure and rampant oil theft had suppressed production for years, but as repairs are made and output rises, the temptation to exceed quotas will grow. Similarly, Angola’s planned exit from OPEC in late 2023 was a signal that rigid quota frameworks are incompatible with national development goals in many emerging producers.

Paul Hickin, Chief Economist and Editor in Chief at Petroleum Economist, shared an insightful observation: “the simple reality is that everyone wants to overproduce and they don’t because it’s usually in their own interests — it’s classic prisoners dilemma in game theory. Iraq have always struggled with compliance more than most probably because they have continued to grow output more than most. And now Kazakhstan is facing a similar issue with the arrival of Tengiz. Many of the others are complying involuntarily anyway apart from the key Gulf members and is why we are seeing a loss of patience and a slow return to what could be a market share war if those poor compliers don’t come into line“.

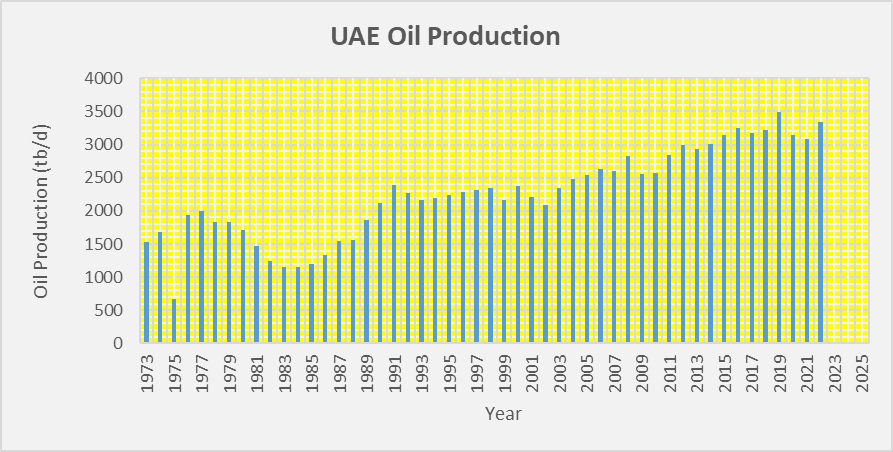

Iran, for its part, has long operated outside OPEC+ quota enforcement due to U.S. sanctions, creating a parallel oil economy that rarely aligns with official commitments. Now, with sanction evasion channels solidifying and Asian markets remaining receptive, Iran is expected to increase production regardless of OPEC+ agreements. United Arab Emirates (UAE) has been granted a higher production quota, allowing it to increase output by 300,000 barrels per day from April 2025 until September 2026 . This adjustment reflects the UAE’s significant investments in expanding its production capacity and its strategic importance within OPEC+. The UAE has repeatedly lobbied for higher baseline quotas, arguing that its massive investments in new production capacity entitle it to produce more. While it remains largely compliant for now, the UAE’s long-term energy strategy (“Operation 300bn” and ADNOC expansions) indicates a desire to monetize reserves sooner rather than later, especially amid global decarbonization pressures.

The deeper reality is this: as the global energy transition accelerates and long-term oil demand projections plateau, OPEC+ members are facing an existential dilemma—maximize income now or risk stranded assets later. This “race to pump” mentality undermines collective discipline, especially among producers who cannot afford to leave barrels in the ground.

All eyes will be on OPEC now – but I shall be looking at the global demand and supply indicators to see where we are actually headed.