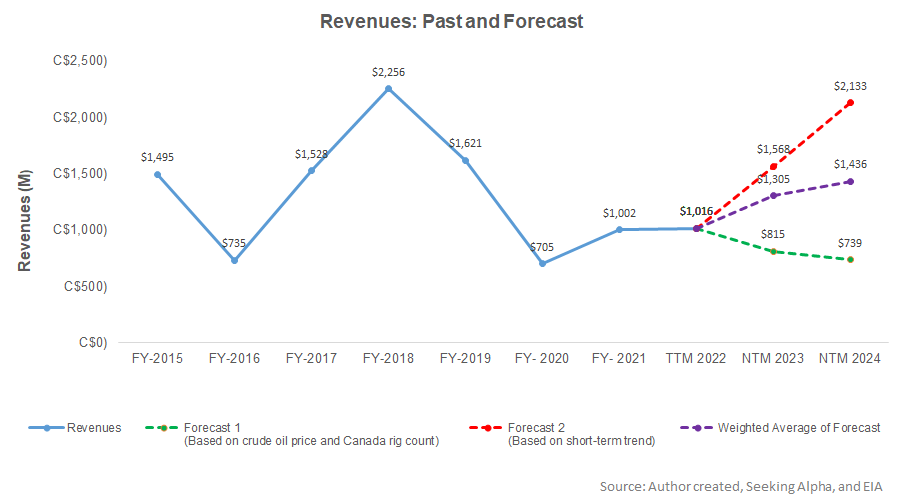

- Our revenue estimates suggest a moderate revenue rise in the following two years.

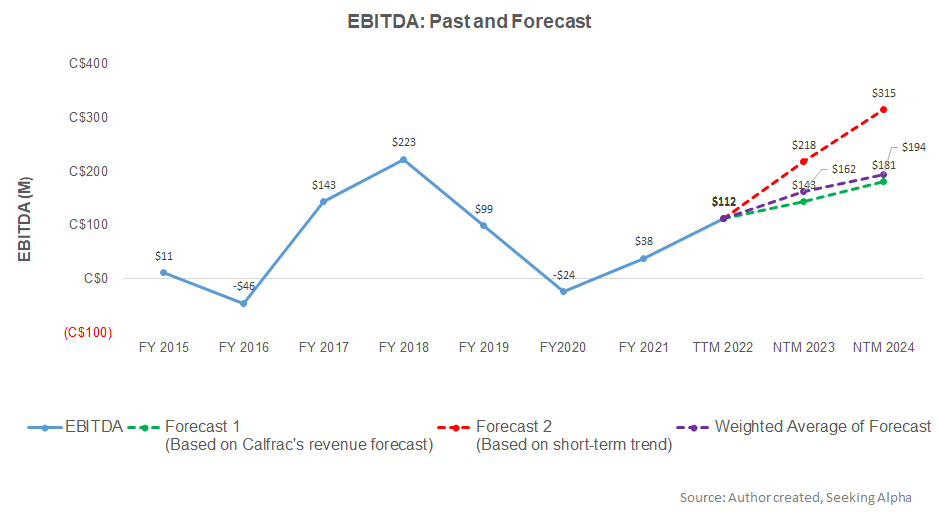

- EBITDA can increase significantly in NTM 2023 and decelerate afterward.

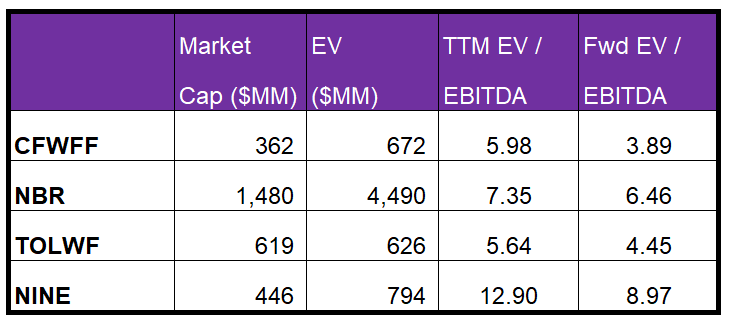

- The stock is relatively undervalued versus its peers.

Part 1 of this article discussed Calfrac’s (CFWFF) outlook, performance, and financial condition. In this part, we will discuss more.

Linear Regression Based Revenue Forecast

Based on a regression equation between the key industry indicators (crude oil price and Canada rig count) and Calfrac’s reported revenues for the past seven years and the previous four quarters, its revenues are likely to increase by 28% in the next 12 months (or NTM 2023) and by 10% in NTM 2024.

Based on the same regression models and the forecast revenues, I expect the company’s EBITDA to increase substantially (195%) in the next 12 months (or NTM) in 2023. The model suggests that the EBITDA growth rate will slow to 45% in NTM 2024.

Target Price And Relative Valuation

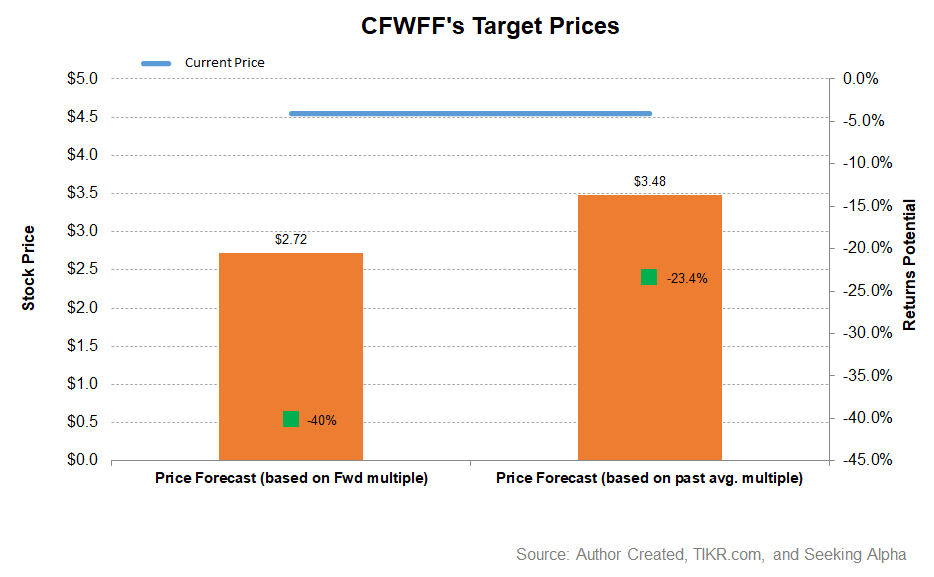

Based on revenues and EBITDA estimates derived from the model, the returns potential using the past average EV/EBITDA multiple (6.0x) is higher (23% downside) than the returns potential using the forward EV/EBITDA multiple (40% downside).

Calfrac’s forward EV-to-EBITDA multiple contraction versus the adjusted EV/EBITDA is steeper than its peers because its EBITDA is expected to increase more sharply in the next year. This should typically result in a higher EV/EBITDA multiple than its peers. However, the company’s EV/EBITDA multiple (6x) is lower than its peers’ (NBR, TOLWF, and NINE) average of 8.6x. The stock is relatively undervalued versus its peers.

What’s The Take On Calfrac?

The positive momentum in the oilfield services industry can carry on in 2023. Calfrac is optimizing the fracturing schedule for its operating crews, which resulted in the average adjusted EBITDA per fleet more than tripling in the past year. It also plans to reactivate the 10th pressure pumping fleet in Q4. In Canada, it is evaluating equipment expansion options to activate additional fleets. So, the stock outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

Although it deleveraged in recent months, its liquidity is not robust. However, its cash flow from operations turned positive in 9M 2022, resulting in a considerable improvement in FCF. Relative valuation-wise, the stock is undervalued versus its peers. Although the near-term returns from the stock look shaky, considering the valuation angle, investors can hold it with the prospect of higher returns in the medium to long term.