Near And Long Term Outlook and Drivers

We have already discussed Baker Hughes’s (BKR) Q3 2024 financial performance in our recent article. Here is an outline of its strategies and outlook. After Q3, Baker Hughes maintained its negative outlook on North America as it expected upstream capex to decrease by “mid-single-digits range.” In international markets, it expects “high-single-digit growth” in FY2024. However, the uncertainty in the crude oil market can extend beyond 2024, leading to volatility in oil prices. Planned growth in deepwater production can result in higher crude oil production in 2025. Global upstream spending, however, can remain unchanged. The management expects “relatively soft oil fundamentals in 2025.”

By 2040, BKR expects natural gas demand to grow by ~20% and global LNG demand to increase by 75%. So, there will likely be a significant increase in gas infrastructure equipment orders because the use of natural gas within power generation and industrial applications can grow. The company maintained its estimate of 800 MTPA of liquefaction capacity by 2030 in LNG. Currently, 200 MTPA of LNG capacity is under construction, while additional FIDs can follow.

Strategy Explained

Over the past few years, BKR has become less cyclical because it could generate durable earnings and free cash flow across cycles. Re-occurring IET service revenue, improved cost structure, and untapped market opportunities led to such sustainable earnings across cycles. Brownfield activity in the market has increased as customers optimize recovery from existing fields. The trend will likely last in the medium-to-long term and will require mature asset solutions. The company’s integrated offering and innovative technologies to enhance total field recovery can see increased demand. Against this backdrop, BKR received an award for a multi-year well intervention and completion contract in the Middle East in Q3.

Energy efficiency and decarbonization technologies are significant as the focus shifts to lowering emissions. On decarbonization, BKR focuses on CCUS, hydrogen, geothermal, clean power, and emissions abatement. Policy support and technological advances will likely give the necessary momentum to decarbonization efforts. Given these factors, BKR’s management is confident of achieving its 2030 orders target of $6 billion-$7 billion.

Q4 Outlook

BKR expects to record Q4 2024 EBITDA of ~$1.26 billion, or 4% higher than Q3. The IET segment can achieve 12% EBITDA growth in Q4, driven by backlog-to-revenue conversion, productivity enhancements, and process improvements. Backlog conversion in gas technology equipment and improved project execution in industrial technology and climate technology solutions will lead to growth in this segment.

On the other hand, the OFSE (Oilfield Services & Equipment) segment can see a 2% EBITDA decline in Q4 due to activity uncertainty in Saudi Arabia, Mexico, and North America. The extent of the impact will depend on SSPS backlog conversion, cost-reduction initiatives, and the amount of year-end product sales.

Q3 Financial Results

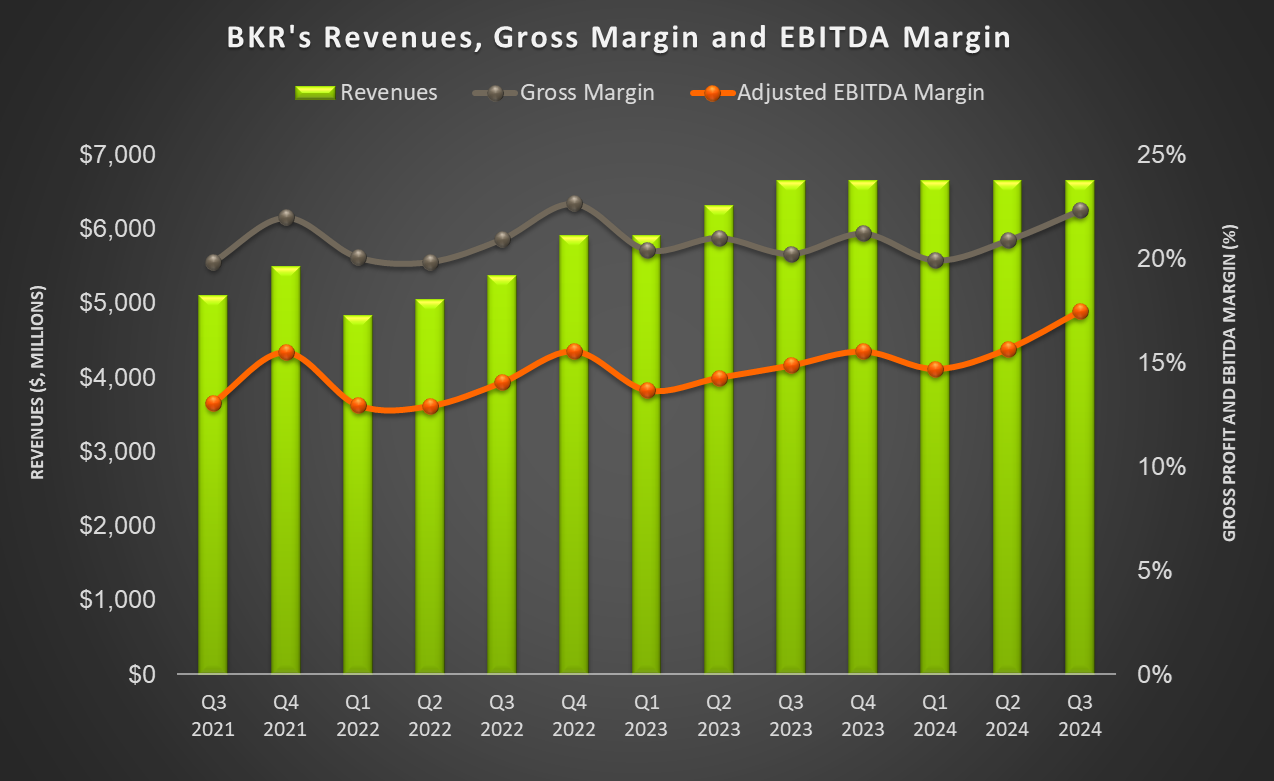

As discussed in the Q3 short article, In the Industrial & Energy Technology segment, revenues decreased by 6% quarter-over-quarter, while operating profit went up by 7%. Revenues in the Oilfield Services & Equipment segment were relatively steady in Q3. The company expects to become “less cyclical and capable of generating more durable earnings” with strong recurring IET service revenue, production-levered businesses, and an improved cost structure. BKR’s cash flow from operations remained nearly unchanged in 9M 2024. Debt-to-equity (0.37x) improved slightly compared to December 31, 2023. It repurchased shares worth $152 million in Q3.

Relative Valuation

Baker Hughes is currently trading at an EV/EBITDA multiple of 10.6x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 10.2x. The current multiple is slightly higher than its past five-year average EV/EBITDA multiple of 10.1x.

BKR’s forward EV/EBITDA multiple contraction versus the current EV/EBITDA is steeper than peers because the company’s EBITDA is expected to increase more sharply in the next four quarters. This typically results in a higher EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is higher than its peers’ (HAL, SLB, and FTI) average. So, the stock is reasonably valued versus its peers.

Final Commentary

Baker Hughes has divergent growth expectations from various geographies. While North America continues to display signs of weakness due to lower upstream capex, international markets will likely grow in the near term due to planned growth in deepwater production. However, a common factor between these markets will remain in the form of increased crude oil price volatility. So, BKR has executed strategies to become less cyclical because it could generate durable earnings through recurring IET service revenue, improved cost structure, and untapped market opportunities. In the medium-to-long term, significantly higher demand for natural gas and LNG will drive BKR’s prospects. It will also gain from investing in energy efficiency and decarbonization technologies.

In the short term, BKR will look to gain from backlog conversion in Gas Technology Equipment and improved project execution. Also, the company’s cash flows remained unchanged in 9M 2024 while its leverage improved compared to the beginning of the year. The stock appears to be reasonably valued versus its peers.

Premium/Monthly

————————————————————————————————————-