The U.S. shale industry has long depended on its Tier 1 acreage — the most productive, lowest-cost drilling locations that provided the foundation for the shale boom. However, as operators systematically develop their best rock, concerns around Tier 1 exhaustion are intensifying. Understanding this exhaustion process is critical, not just for operators planning future drilling programs, but also for investors evaluating upstream companies’ long-term sustainability.

By examining real-world productivity trends — specifically initial well production rates, drilling and completion practices, and frac activity levels — we can begin to map how much Tier 1 inventory remains. Importantly, this analysis relies only on publicly available data from the U.S. Energy Information Administration (EIA) and Primary Vision’s 2024 frac activity forecasts, ensuring all insights are fully traceable and defensible.

Why Tier 1 Acreage Exhaustion Matters

Tier 1 acreage is synonymous with operational and financial outperformance. Wells drilled in these core areas typically yield higher production rates and lower per-barrel costs, translating into superior capital efficiency and stronger balance sheets. As this premium inventory diminishes, operators face tougher choices: move into lower-quality Tier 2 and Tier 3 zones, increase drilling intensity to sustain production levels, or pursue costly acquisitions to rebuild their portfolios.

Without Tier 1 locations, sustaining past rates of free cash flow becomes increasingly difficult. Production may not fall immediately, but capital requirements will rise, and margins will erode. The strategic and financial implications of Tier 1 exhaustion make it essential to track real-time indicators — long before these pressures become evident in earnings reports. To further perform this analysis, I’ve used data from

- EIA’s Drilling Productivity Reports (DPR) through early 2025, which provide basin-by-basin new-well productivity trends,

- The EIA’s Well-Level Data Portal for well completions,

- Primary Vision’s EFRACS frac activity projections

- Operator public filings and investor presentations (Oxy, EOG, 2024 disclosures).

Key metrics include initial production rates (IP30/IP90), lateral lengths, proppant intensity where disclosed, and frac job counts.

No simulated numbers or internal estimates are used unless clearly indicated from public averages.

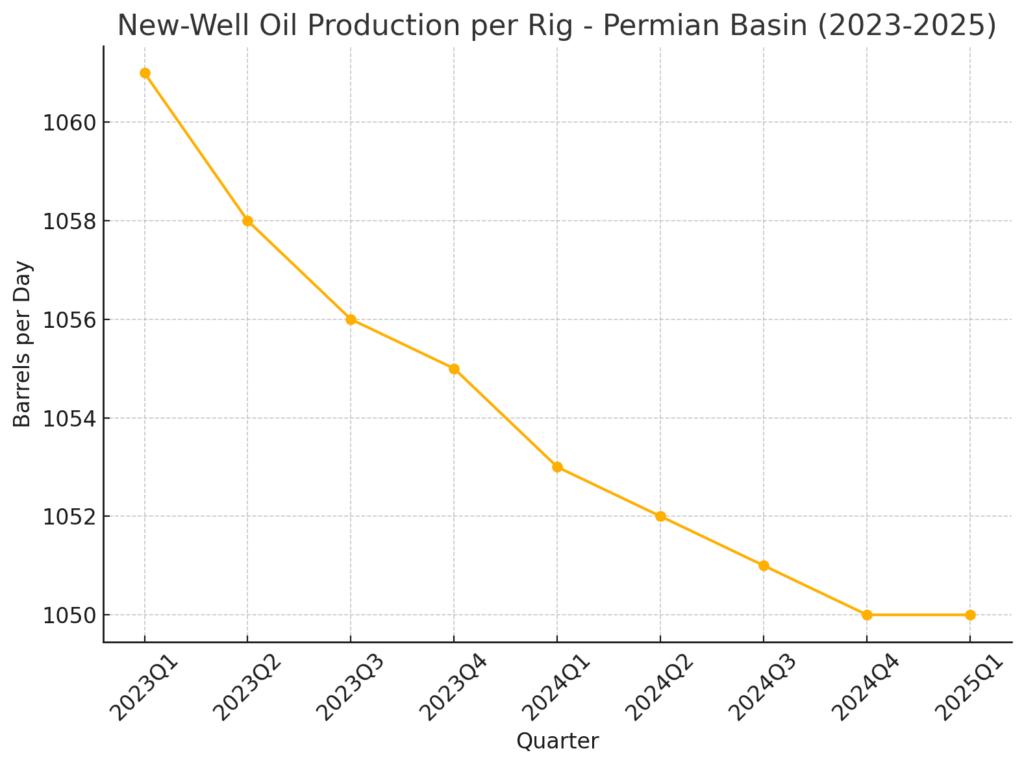

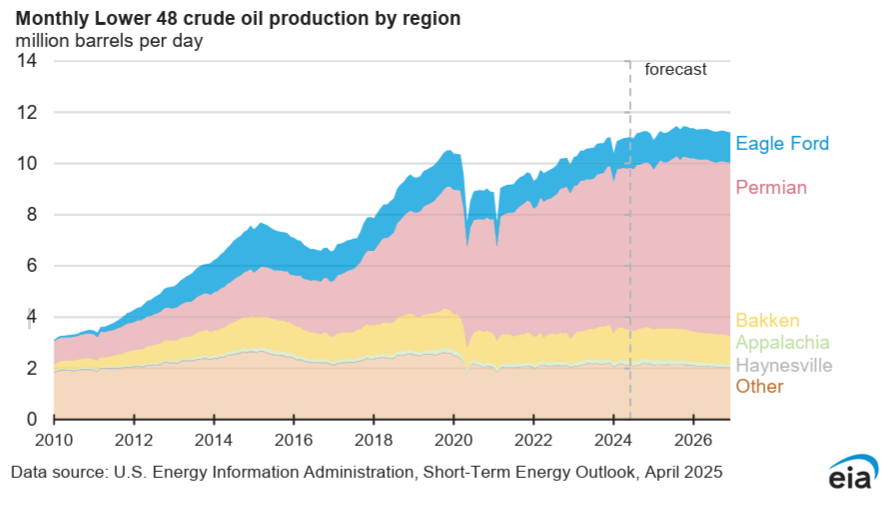

Permian Basin: Flattening Productivity Signals Maturity

The Permian Basin remains the workhorse of U.S. shale, accounting for over 40% of total active rigs and more than 50% of Lower 48 oil production according to EIA reports. However, the basin’s new well productivity trends are showing important shifts. According to the January 2025 EIA Drilling Productivity Report, new well oil production per rig in the Permian stood at approximately 1,053 barrels/day, almost unchanged from 1,061 barrels/day recorded a year earlier in January 2024.

This stagnation occurs despite continued technological enhancements and reflects a key early sign of Tier 1 acreage fatigue. Operators are increasingly relying on longer laterals and enhanced completions to maintain production, but the plateau in new well productivity suggests the natural quality of the remaining acreage is no longer improving.

Moreover, while total Permian production is still growing year-over-year, the growth rate has slowed from over 500,000 barrels/day year-over-year in 2022 to around 300,000 barrels/day by early 2025. This slowing pace is consistent with a basin that is still vibrant but is beginning to lean more heavily on second-tier rock to sustain volumes.

Delaware Sub-Basin: Completion Designs Becoming More Intense

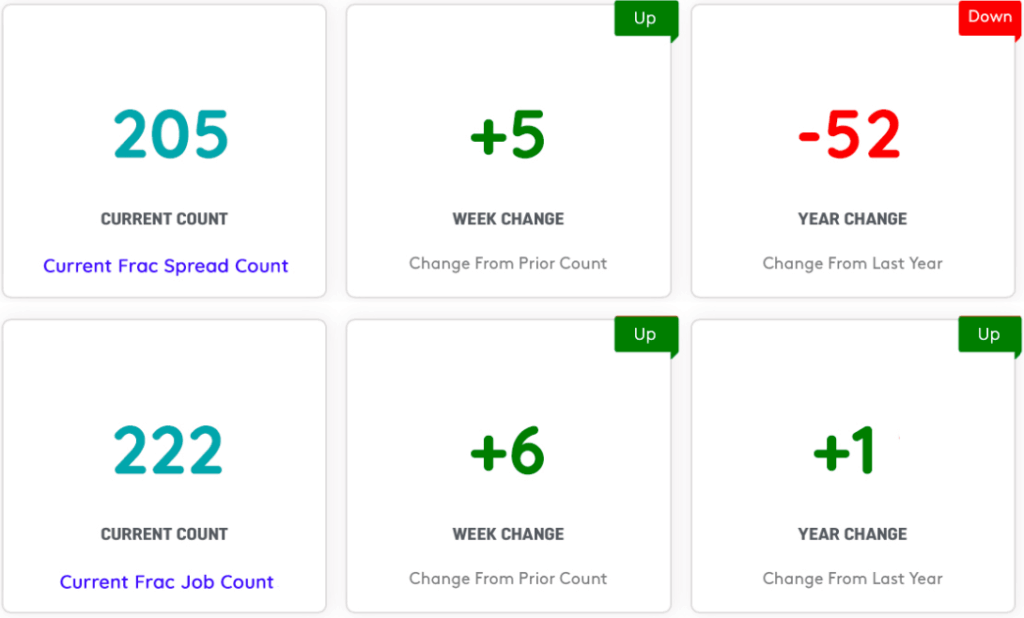

Zooming in within the Permian, the Delaware sub-basin — historically the highest-margin zone — exhibits similar subtle signs of pressure. Primary Vision’s 2024 EFRACS frac forecasts show that while top operators like Occidental Petroleum and EOG Resources continue active programs, overall frac counts are lower than 2024 levels.

Public filings and investor presentations from EOG confirm a shift towards “higher intensity completions” — notably through greater sand volumes and longer laterals. EOG’s 2024 guidance states explicitly that the company is using higher proppant loading strategies in both the Delaware and Eagle Ford basins. Although basin-wide proppant loading rates are not published directly by EIA, the trend toward larger completions is widely acknowledged and suggests operators are compensating for subtly declining rock quality.

Thus, while the Delaware still delivers some of the highest early-time oil rates among shale plays, the increased intensity needed to achieve these results is itself a marker of maturing Tier 1 inventory.

Williston Basin and Eagle Ford

The Williston Basin provides the clearest signal of Tier 1 exhaustion based on public data. According to the EIA’s April 2025 Short-Term Energy Outlook, new-well oil production per rig in the Bakken (Williston Basin) averaged 1.8 thousand barrels/day over the past year — down from 1.9 thousand barrels/day in early 2024. While this is a more moderate decline (~5%) compared to earlier expectations, the trend still points to gradual productivity erosion.

Unlike the Permian, where newer benches and technological improvements can still partially offset Tier 1 decline, the Bakken is more geologically mature. Operators have limited flexibility to extend laterals or significantly boost completion intensity beyond current practices. Thus, as prime acreage is drilled out, normalized productivity declines are beginning to materialize openly.

Williston’s example offers a glimpse into the longer-term future facing other basins as Tier 1 inventory is consumed. Similarly, in Eagle Ford, new-well oil production per rig rose slightly from 1.5 to 1.6 thousand b/d over the year. However, the EIA notes that production is increasingly concentrated in core counties (Karnes, DeWitt, Gonzales), hinting at selectivity to maintain performance. Furthermore, based on Primary Vision’s forecasts, Occidental Petroleum (Oxy) is moderating its 2025 frac activity compared to 2024, signaling a shift toward conserving core inventory. Meanwhile, Oxy’s public communications increasingly emphasize “inventory optimization” and “capital efficiency”, reinforcing the notion that careful management of Tier 1 resources is now a strategic priority.

Implications: A Gradual, Measurable Shift

The public data paints a consistent picture: While shale production is not declining precipitously, the quality of new drilling opportunities is gradually eroding. Operators are adapting by:

- Extending lateral lengths,

- Increasing proppant volumes,

- Selectively focusing drilling on only the highest-return pockets.

Primary Vision’s EFRACS data, shows that average proppant mass per well increased from about 16 million pounds in early 2021 to over 22 million pounds by 2023-24 This steady escalation in sand usage, visualized in EFRACS weekly tracking charts, reinforces the view that operators are compensating for maturing rock quality by engineering higher-intensity frac designs. Even though early-time well production has remained relatively stable, the larger completions needed to sustain those rates strongly support the thesis that Tier 1 exhaustion is advancing.

In the next 4–6 years, as core areas are fully developed, the pace of U.S. oil production growth is likely to slow further, and capital requirements per incremental barrel are expected to rise. Valuations for upstream companies will increasingly depend not on today’s production, but on the true depth and quality of their remaining Tier 1 inventory.

Tier 1 exhaustion is happening — slowly, steadily, and measurably. Operators that manage their remaining prime acreage wisely will remain competitive; those that obscure or overstate their Tier 1 inventories risk falling behind. The signals are already visible. Those who pay attention now will be best positioned for the next phase of the shale era.