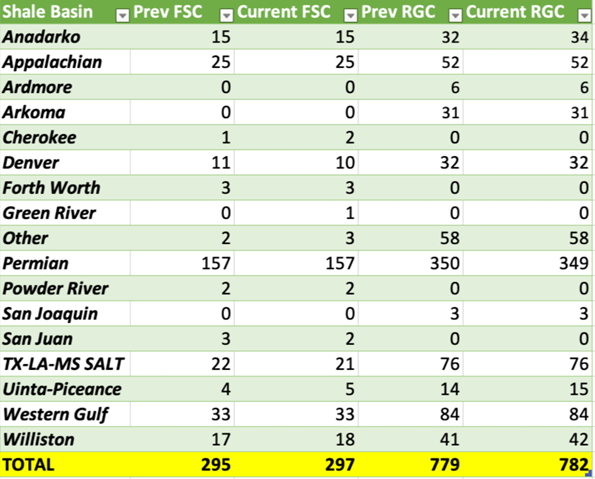

[ihc-hide-content ihc_mb_type="show" ihc_mb_who="14,16,20,23,24" ihc_mb_template="1"] We had another bump in activity that was driven by the smaller basins. As we outlined last week, we could get one more push higher to about 297, and now that it’s here- we will see a drop next week as we head into the Thanksgiving Holiday. Seasonality will kick in aggressively over the next few weeks with the slowest period in the year is the 6 weeks between Thanksgiving and New Years. Now the drop will be “less severe” vs other years given we are starting at a lower point vs other periods. DUC counts showed an “official” bump as companies focus more on manufacturing mode. The below chart should be of no surprise to our readers as we have been calling for a flatline in DUC drawdowns and small build to increase heading into year-end. This will provide a strong base for 2023 to see production move gradually higher to about 12.7M barrels per day. One of the biggest overhangs will remain crude demand, but I expect to hear more about cuts originating from OPEC over the next 2-3 weeks. The market remained volatile across the paper markets after a missile landed in Poland killing two people. Governments have tried to calm the markets by claiming it originated within Ukraine and intercepted an incoming ballistic missile attack. This swift moves just demonstrate how jumpy the commodity world is in regard to the Russia-Ukraine situation. We have seen a meaningful amount of crude struggle to find buyers, which is growing to about 40M. This will prompt KSA to issue another round of OSP cuts, and other incentives in an attempt to clear the excess in their market. We expect to see differentials to weaken further to clear additional cargoes in ME and WAF, while Forties finds some support. Johan Sverdrup cut prices again as some crude grades still struggled in the European markets: BP offered Johan Sverdrup for Dec. 6-8 at Dated -$4.20/bbl, FOB, vs -$3.20 on Thursday The Russian price cap is set to take effect on December 5th that will limit the use of European and U.S. banks for shipping, insurance, and transactions unless the price crosses below the designated price. There will be multiple ways around this process with countries either opting out of the price cap or paying above the allotment through other means of barter or banks outside the European/US sphere. According to Janet Yellen: “The United States is happy for India to continue buying as much Russian oil as it wants, including at prices above a G7-imposed price cap mechanism, if it steers clear of Western insurance, finance and maritime services bound by the cap, U.S. Treasury Secretary Janet Yellen said on Friday.” We have said from the beginning that the U.S. would not stop Asia (especially India and China) from purchasing crude from Russia. This will support the current volumes already moving from Russia into the Asian region: India has reduced current purchases of Russian crude in the near term, but we expect them to pick back up as we head into the middle/end of December. While the paper markets bounce around, the physical market has been weakening on a differential basis as oversupplies grows in West Africa and the Middle East. Europe increased their purchases of CPC, Libya, and U.S. blends based on softer prices and elevated shipping rates. We expect to see LLS remain about $1.50-$2 below Brent with WTI holding about $7 below Brent- helping to move volume to the coast and into Europe. New shipments of crude from the U.S. to Asia (mostly South Korea and Japan) have slowed due to shipping rates, which will keep U.S. crude heading to Europe. A portion of Shell’s Zydeco crude pipeline went down today, which caused some disruptions within the U.S. In Midland, the grade is trading at the weakest premium to US oil futures in ~three weeks Light Louisiana Sweet crude, a substitute for WTI, gained $2 to $6/bbl above US oil futures, highest premium since May December loading WTI crude cargoes are at ~$4.50/bbl under ICE futures, from $3-$3.50 discount last week Heavy sour Colombia crude prices are weakening as demand from China, traditionally the top buyer, remains subdued amid lockdowns, according to people with knowledge of the situation. Weaker differentials of Canadian crude, the top supplier to US Gulf refiners, also weighing on prices Castilla loading in December priced at a discount of $14 to $15 per barrel vs ICE Brent; that compares with -$12/-$13 for November December Vasconia at discount of around -$6 vs -$5 for November Colombia’s state oil company Ecopetrol created a new subsidiary, Ecopetrol US Trading LLC, to market crude oil and oil products in the US; Ytd Colombian oil exports to the US rose to ~193k b/d up 34% compared with same period of previous year, according to ship-tracking data compiled by Bloomberg TransCanada announced Force Majeure on Keystone, which will cut about 590k barrels a day in the near term due to weather. This will result in some additional Cushing draws, but they will be short lived as it was weather driven. We expect some of the recent premiums into Cushing to dissipate as demand still remains lackluster. Heavy Cold Lake crude’s discount to WTI continues to narrow on Wed. at US oil trading hub as other sour grades gained at the Gulf Coast after TC Energy cut Nov. shipments on its Keystone pipeline Heavy Canadian oil sands grade Cold Lake’s discount to WTI narrows $2.60 to $11.40/bbl at Cushing, according to Link Data Services. Western Canadian Select at the US Gulf narrows $3 to $10/bbl discount Discount at Hardisty, Alberta, was unchanged at $28.60/bbl: data compiled by Bloomberg US sour crude grades gained on Wed. Mars discount to WTI narrowing $1.95 to a 25c, strongest price since April Poseidon’s discount narrows $2 to $1.25, also strongest since April Prices strengthened since TC Energy announced to shippers on Monday cut to November shipments on Keystone pipeline due to weather-related disruptions These premiums will fade as Keystone operation normalizes into December. WTI Crude cargoes will stay a bit softer to account for slower demand into Asia, and the rise in shipping costs. Europe also increased buying from CPC as the second mooring came back online and Kazakhstan ramped up crude to 9-month highs. “November seaborne flows of CPC crude were surprisingly revised up and are now planned at 5.422 million tons, or 1.43 million barrels a day, according to the final loading program seen by Bloomberg. That’s the highest in eight months and a steep increase from the 1.08 million barrels a day shipped in in October.” The ramp in CPC and Libya exports has left more crude in West Africa and the Middle East. The pace of West African crude sales for December loading is much slower than normal as demand from key buyers in China, India and Europe has weakened, and freight rates rose to multi-month highs: About 7-10 out of 36 Angolan cargoes for December have yet to find a home, while new loading program for January is expected to be released later todayMost Angolan cargoes are typically cleared at this time of the month Nearly half of 46 Nigerian cargoes for December are still available Equinor offered 950k bbl of Pazflor for Dec. 23-24 at Dated - $2.80/bbl, FOB: trader monitoring Platts window Compares with its previous offer at -$2.05 on Thursday Unipec offered 650k bbl of Lokele for Dec. 29-30 at -$6.90/bbl Co. withdrew offer for 920k bbl of Djeno for Dec. 13-14 at -$5.85 Glencore offered 950k bbl of Doba for Dec. 10 loading at -$5.35/bbl They have fallen by anywhere from $.50-$1.50 from the beginning of the month and with Angola’s schedule announced for January they will have to fall further. West African Floating Storage Based on current buying, we will see floating storage in WAF move back to the highs and promote steeper price cuts to account for lack of demand and elevated shipping rates. The Middle East is also seeing a big spike in floating storage that is “unseasonal” as they struggle to clear cargoes above contracted volumes. This is putting more volume on the water with little demand coming from the U.S. and Europe. By KSA maintaining elevated OSPs for Europe and U.S., they reduced flows to the West- but weak demand and elevated Russian flows have hindered Asian demand. We expect to see more discounts or incentives to get more cargoes out of floating storage. Middle East Crude Floating Storage Another shift in the market is the presence of Russian refined products hitting the market- especially in the Middle East. Asia is saturated with crude and product- so more is being directed into the Middle East. “While the flow of Russian fuels is set to pick up, there’s a possibility Asia can’t fully digest all the excess, contributing to lower prices and a rise in volumes stored at sea, especially as slowing economic growth may dent demand.” Local markets for naphtha and high-sulfur fuel oil, HSFO, are already oversupplied, in part due to an influx of Russian products. Highlighting that situation, the prompt time spread for HSFO is in contango, setting up a bearish backdrop. Countries such as UAE have increased their imports of Russian refined products where they co-mingle it with their locally created volumes to be exported into the West. Another option, which Saudi Arabia has done, is to import cheap refined product from Russia and consume it locally- slatting all regionally created product for the export market. The below chart puts into context just how much things have shifted, and we expect to see more fuels heading into the region- especially as we get closer to the introduction of the price cap. OPEC reduced their demand estimates again by 520k barrels a day following sluggish data from around the world. “Due to a weaker economic backdrop and China’s strict anti-Covid measures, the Organization of Petroleum Exporting Countries lowered estimates for the amount of crude it will need to pump this quarter by 520,000 barrels a day, following a similar-sized downgrade a month ago.” Saudi Arabia reduced total production, but we expect to see Iraq and UAE produce above their new quota. We expect to see exports from the GCC to be down about 1M barrels a day, but more to clear the glut of floating storage and utilize onshore tank space. The cost of shipping as ballooned with a record amount of crude in transit pushing rates higher. We expect to see more reductions on total crude demand in the near term as 2022 and 2023 estimates of demand remain well above our expectations. Crude oil in transit (graph below) will stay at these elevated levels as tankers indicating China remain at seasonally adjusted all time highs. Crude Oil in Transit China Super Tanker Crude Imports In summary, physical crude markets will weaken further as countries attempt to clear floating storage. We expect to see the discount of Dubai to Dated Brent to increase as the region looks to clear more crude. The current spread is at $8.35, and we expect the premium of Brent to widen a bit more back to about $9 to clear some of these crudes. The discount of Dubai to WTI has also intensified, which has helped stop flows of U.S. crude into Asia and pushed more into Europe. Timespreads in Europe weakened with more pressure coming through as European refiners run below normal utilization rates and more crude becomes available from CPC and Libya. We see some near-term support in F3-G3 at about $1.10, but will see it sitting range bound at about $1.15-$1.25. As we look further out on the curve, we see support at spreads around $1. Even as demand fades, supply curbs will help keep pressure to the upside and anything at the $.80 level would be a good pickup looking further out on time spreads. We saw some trades in Forties and chains out of Europe trade up to about $2.55 above dated Brent, which was a premium of $.65 above last trade. The “right” clearing price will fall a bit further as West Africa discounts grow, and Middle East crudes get more aggressive in the market. WTI and Brent futures will remain volatile, but I think we see some support at these levels with WTI bouncing up to $84 with support at $79. Brent will move back to $90 with support remaining at $87 with some movement back up. We still remained very concerned about crude prices as we head into 2023 as the recession intensifies around the world. Longer term- we will see prices for WTI move closer to $70-$72 and Brent down to about $75-$77. The below chart helps to put into context a slowdown in the crude space. We have seen prices weaken further in the physical market as floating storage remains elevated around the world. There is more downside risk to industrial activity as we move through the end of the year and into Q1’23. This will lead to more degradation on diesel demand- especially in Asia. The slowdown in Europe, U.S., and China takes time to work through the supply chain, and we can already see there is a negative move coming. This will weigh on diesel/ MGO (Marine gasoil) further, but it’s already pulling down industrial activity which consumes a large part of diesel. India’s exports took a big turn down, and we think that pressure remains and weigh on internal demand there as well. The CAPEX forward look has worsened again, which ties closely to companies tapping their credit lines (chart on that later on). It supports our view that diesel and inherent industrial demand will weaken further and put more downside pressure on crude demand. The OECD Leading Indictors have turned steeper into contraction resulting in more pressure on global trade and underlying demand. The new export orders are showing how the cracks are growing, and it is hitting the global economy at a bigger level. Key export nations are seeing a marked shift lower in activity, which will weigh on underlying demand. Another key problem is- the slowdown is going to continue well into next year based on all of the long lead indicators. The Freightos Baltic Index from China/E.Asia to the US East/West coasts increased at the beginning of November but SONAR’s TEU Volume/Capacity indices were signaling that this attempt by carriers at a General Rate Increase (GRI) would be unsuccessful. Overnight, the FBXD dropped another $406 to $1919 per 40-foot container (FEU) on the China/E.Asia to the US West Coast lane; a new low for 2022. For perspective, this same lane was priced at $1942 per FEU on Nov. 1st, 2016.” All of the data is showing how everything is being driven lower on the pricing and demand side. Volumes are dropping through a floor around the world, and we are getting more cautious commentary from key distributors, such as Target, Maersk, Amazon, and other consumer facing entities. The consumer has remained somewhat resilient over the last few months, but the shift has started to accelerate. From the Target earnings call: “As we look specifically at third quarter results, they demonstrate how our business continues to serve our guests even in the face of an increasingly challenging backdrop. Because of a deepening level of trust we've established with our guests over the last several years, our topline continues to benefit from growth in guest traffic and unit share gains across all of our core categories. This is particularly notable, as consumers are showing increasing signs of stress and pulling back from discretionary purchases. And it reinforces the value of having a balanced multi-category portfolio, which allows us to satisfy our guests' ever-changing wants and needs.” “More specifically, consumers are feeling increasing levels of stress, driven by persistently high inflation, rapidly rising interest rates, and an elevated sense of uncertainty about their economic prospects. With higher rates of inflation continuing to erode their purchasing power, many consumers this year have relied on borrowing or dipping into their savings to manage their weekly budgets. But for many consumers, those options are starting to run out. As a result, our guests are exhibiting increasing price sensitivity, becoming more focused on and responsive to promotions and more hesitant to purchase at full price.” When we look at retail sales, the volumes adjusted for inflation remain flat and are starting to trend down a bit more. “In nominal terms, US Retail Sales still appear to be booming, rising 7.5% over the last year & hitting a new high in October. But after adjusting for inflation, the story changes. Real Retail Sales peaked in March 2021 & are down 0.3% over the last year.” There is another look at the control group that shows things have remained flat, but as pressure mounts (inline with Target outlined) we expected to see a bigger contraction as we head through the rest of the year. The biggest contraction is likely to be in Q1’23. The below breakdown of inflation helps show where inflation keeps showing up, and many of the key ones impacting the consumer aren’t going anywhere. We are still at the very start of the winter, and yet we are already seeing a spike in electricity prices. This isn’t going to slowdown as baseload power falls short and demand grinds higher. The cost to the consumer is moving in one- very dangerous- direction. The most recent leading indicator for the U.S. shows growing pain as the data shows a move lower, and if you look at the last time we have been at these levels- we were either in a recession or rapidly moving into one. Companies are also taping their credit lines at an accelerating rate as the bond market closes or becomes too expensive to access. These types of shifts are leading indicators of a company’s willingness to hire, invest, deploy CAPEX, and overall spending. This is something that happens when companies are looking to tighten belts. The general theme so far of the regional Fed data shows more slowdowns. Even though the Empire Manufacturing data showed a bounce- the trend is still lower with a “lower, high” and points to more pressure lower. When we look at all the leading indicators embedded in the Empire State data- the picture becomes a bit clearer. When we look at “Expected Business Conditions” and “Expected New Orders”- the data is showing the worst ever. “Outlook for new orders from Empire Manufacturing PMI has fallen to lowest (most negative) in history of survey.” The Philly Fed shows something even worse on the current and future outlook of the data. “The Philly Fed index faltered in November to a contractionary -19.4 from an already bleak -8.7 reading in October. The data go back to 1968, and guess what? In expansions, this index averages +13.3. In recessions, it averages -18.3. We are now at -19.4.” It also points to a big revision in earnings power for companies. The forward-looking data shows something similar (again). Kansas City is no different. Even as some of these entities roll over, prices paid and received remain in expansion with some actually showing additional price appreciation. This is supportive of our view regarding stagflation vs deflation. It also puts MAXIMUM pressure on the consumer that is seeing their earnings power get depleted. The Chinese data points to more issues ahead as the local consumer points to even more propensity to save. It also confirms everything we have been saying, and points to more pain ahead as the “end to the COVID Zero Policy” has hit many hiccups so far. China home prices fell for a 7th consecutive month, down 2.4% y/y, with less than 15% of cities having rising prices. Even though construction activity has bottomed, it was driven by a SIGNIFICANT amount of stimulus that is still not driving a meaningful investment cycle. It supports our view that “Supply” of credit isn’t the issue, but rather the lack of “Demand” in this time frame. We don’t see a big rebound in construction at this point. Chinese consumption growth has been incredibly weak over the last two years, and we don’t see this changing in the near term. Even when there weren’t lockdowns, we haven’t seen a reversal in spending- instead it has held steady in current depressed levels. The inherent industrial expansion (aka jobs) has relied on infrastructure and exports, both of which are under pressure. This uncertainty is creating additional hesitancy to spend. Real retail sales fell slightly to pre-pandemic levels, showing zero growth in over two and a half years and standing at 17% below trend. All of the surveys also confirm the unwillingness of the Chinese consumer with a higher propensity to save. China new home prices remain in contraction with only 15% of all cities showing a marginal increase, and this matters significantly for China where their citizens are the second most levered to home prices in the world. As asset values fall, it will keep pressure on their willingness to spend. Fixed asset investment also show a modest contraction with manufacturing still holding in a bit, but that will also weaken as more companies adjust supply chains by pull capacity out of China. The “onshoring” and “near-shoring” is something that will continue happening over the next few years. Some components are hanging around the 10 year average, but as real estate falls further- it will drag down other infrastructure spending. This is a big problem because the CCP has relied on infrastructure investments to offset the loss of exports in previous down cycles. The law of diminishing returns is hitting hard! China main activity indicators for Oct were generally weaker than expected, declining on a m/m basis . Real estate sector disappointed again as floor space started remained at 13-year lows while residential demand dropped back to cyclical lows. Overall construction activity was unchanged at cyclical lows and 23% below pre-pandemic trend while bottoming out on a y/y basis (-9.7% y/y vs -14.1% in Aug). It’s important to recognize that the below numbers is with A MASSIVE amount of government and PBoC support. They have pushed banks to lend more, reduce rates, and collateral requirements but it has done nothing to shift the market. It’s unlikely we see a bigger increase in lending or support for economic growth as the CCP (and Xi) pivot more towards total control and party loyalty. The focus on security and socialism/communism is at the forefront of the message. This will weigh on growth further and not less. There is also a significant limit to the amount of “new” cash that can be pushed in the market. They have already levered every balance sheet possible, and this will limit the amount of new stimulus and underlying liquidity the PBoC can push into the market. All the while, the “adjustment” to the zero COVID policy is going TERRIBLE as case numbers skyrocket. But problems quickly arose: In tandem with the above, the city abolished the requirement of having to show a negative test result to access public transportation, but test results are still required to enter certain public venues like hotels. Residents could only take tests at hospitals – but some hospitals require valid test results to enter! Some private companies still require employees to get tested every two or three days to limit the risk of being closed down under COVID controls (CLS.cn). On Monday, widespread confusion forced Shijiazhuang’s Party chief to publicly deny the city had given up zero-COVID (Sina): “We are by no means ‘lying flat’, nor totally letting it go, and this is absolutely not a so-called ‘full opening-up‘.” Cue the 180: On Tuesday, many public testing booths in Shijiazhuang reopened, and authorities vowed to keep at least 30 testing booths open in each of the city’s eight districts (163.com). Get smart: As long as zero-COVID remains the policy of the land, local authorities – and private businesses – must keep many restrictions in place to avoid prolonged lockdowns. Get smarter: Chaotic implementation of the recent policy adjustments will complicate policy review and design in Beijing, delaying further moves towards relaxing zero-COVID. Another important one to watch will be the slowdown in India exports with inflation remaining an underlying problem- especially in core CPI. We don’t see a lot of support in exports in the near term as global trade remains under a lot of pressure. There food situation remains a big overhang, which will support more pressure on the core CPI front. The world is facing a global food shortage that rivals the 1930’s and the “Dust Bowl.” “Even before COVID-19 reduced incomes and disrupted supply chains, chronic and acute hunger were on the rise due to various factors, including conflict, socio-economic conditions, natural hazards, climate change and pests. The impact of the war in Ukraine adds risk to global food security, with food prices likely to remain high for the foreseeable future and expected to push millions of additional people into acute food insecurity.”[1] The UN Food and Agriculture World Food Price Index is still trending at the highest it has been in at least the last 29 years. When we look at other peak years (2011 and 2021), we are still at a record setting pace. The period of 2011 saw the start of the Arab Uprising (Wheat Wars), which all started on the back of food shortages and price spikes. Food prices remain above this pivotal level from 2011 with more pressure coming as the planting in Ukraine is non-existent and more countries withhold exports. India has been the latest to put up “gates” around wheat and rice exports to ensure there is enough volume for those at home. Diesel and fertilizer prices are still remained near historic highs, and as we head into a pivotal winter season will like rise back to the highs. Fertilizer is an energy intensive process, and as prices (such as natural gas and diesel) move higher again- facilities have to either pass on the cost or cut utilization rates. UN Food and Agriculture World Food Price Index In Europe, fertilizer production has been curtailed due to the huge spike in pricing as well as to preserve natural gas due to Russian sanctions. The U.S. is still one of the cheapest places to due business and local companies such as Mosaic are in a position to capitalize on their advantaged position. In comparison to previous shocks, the Mosaic (MOS) stock price has underperformed the recent increase in prices. The market in general is very different today vs previous spikes as weather patterns shift increasing drought in some areas and severe flooding in others. This drives up the price of food and incentivizes farmers to do whatever is possible to increase yield. Farmers can try to adjust crops or put down additional fertilizer to try to pump up yields. Mosaic Stock Price vs UN Food Price vs North America Fertilizer Prices The only problem is- the fertilizer market is facing additional supply issues! Russia accounts for more than 80% of the currently forecasted expansion of potash production. According to K+S, “Even in the optimistic case, global potash supply will not return to the level of 2021 before 2026.” They have the same base case that I have “all current sanctions remain in force, but some “friendly countries” (that Russia exports to) resume/continue partial trade with Russia. Not matter how you look at the market- potash capabilities will remain well below 2021. The shifting crops profitability will allow farms some freedom in flexibility to increase purchases to increase underlying yields that have struggled. The tailwinds on fertilizer consumption remains robust as populations continue to fall and arable land per capita drops. This is being complicated further as yields on the current land is also stagnating as the amount of people on the plant rise at a steady rate. The shift in crops and planting needs requires more potash to be consumed over the coming years, which will support pricing around the world. This is a positive tailwind for Mosaic and other producers, but the U.S. and Canada are in the best positions given the rising costs in Europe. When we look at the global market, Mosaic made some great observations regarding the dynamics underpinning the supply/demand of food: “Global grain and oilseed stock-to-use ratios remain at 20-year lows and early data continues to suggest there may be further downside to total production once the fall harvest is complete. It is important to remember that the market was tight when the year began well before the start of the war and issues over the last several months that further exacerbated the situation.” Mosaic operates in North and South America, providing a certain amount of geopolitical stability enabling them to increase total production to about 25M tons of finished product by the end of 2023. They have taken the initiative to expand production in key areas at only a step up of about $100M in new project costs, which is a clear double digit return even if fertilizer prices fall. There is concern around the world about the availability of fertilizer, which is causing some countries to horde and others to source product ahead of schedule. This is pulling forward tightness and providing support for pricing well into 2023. As described by Mosaic management: “With the strong demand in Q4 and getting into 2023, we continue to see the supply constraints for both Phosphate and Potash. On phosphate, we expect that Chinese export control will continue as we get into 2023 as the Chinese government to ensure the domestic supply availability and their farmers to be able to get fertilizers for their food production. And there's very little new capacities coming online in Phosphate production in 2023. Similarly to Potash, we envision Belarus and Russia's supply will remain constrained in 2023. And the alternatives as well [ph] will not be able to ramp up quickly to offset the continued constraints from that part of the world.” They see an uplift to margin of about $40-$50 a ton in a flat pricing environment, which is unlikely to occur given the broad shortfalls in the market. This comes from some of their costs improving while shortfalls persist providing a floor in prices with clear upside that falls directly to the bottom line. This puts a lot of upside potential to earnings as the price of fertilizer rises over the planting season. Prices have come down a bit, but it’s driven more by seasonality and less about a drop in demand. China posted a big shift higher in food prices, and the government has already said they will do everything in their power to defend against food inflation. This will support additional restrictions on exports of both food and fertilizer to bring prices lower and ensure farmers have availability of product. High food prices continue to boost CPI: Food prices jumped 7.0% y/y last month. The price of pork spiked 51.8% y/y – the fastest this year. The below chart puts into perspective of the issues facing Emerging Markets, and China is facing very similar problems. Emerging markets have already seen a bigger food price surge vs what they experienced during the Arab Spring or the Peasant Uprising. This will put more pressure on governments to try to maintain some semblance of normalcy through subsidies. The World Bank has been issuing near-term loans and grants to help countries to pay farmers, finance fertilizer and food purchases, and other investments to increase yield. Even as some of the below prices have fallen- they still remain above the pricing regime that brought about the Arab Spring. When we break this down into “real terms” when evaluating food prices- we are right back to levels not seen since 1974. Food prices are going to be pinned to a high as fertilizer prices recover back to the highs. Everything from diesel to fertilizer are sitting at near records that will keep farmer costs elevated, which will be passed on to the consumer. As we have said in the past, Food shortages don't happen suddenly- it takes time to work through storage and state reserves. It started out slow in the end of '19 but accelerated in '20-'21 with droughts/floods/pests/logistics... Ukraine-Russia is just the topper to a situation that started several years ago. The issues have been compounding since the end of 2019, and now we are in a terrible position with ANOTHER projected terrible year of crops BEFORE we even consider the impacts of Russia-Ukraine. The grains corridor that allowed about 4M tons of Ukraine grains into the market have been called into question after Russia announced they were “pausing” their involvement and followed that by saying they may not renew the deal. Not only are we losing flows of grains and food oils, but fertilizer as well from the embattled countries. The below chart helps to put into context just how much the world has relied on Belarus and Russia for the macro-nutrients our crops require. As yields slip further around the world (especially in the U.S.), we will need more nutrients to push yields to their maximum. The problem is- we have stretched our soil to the breaking point, and we will need to find solutions to address the weakening yields. Corn yields have essentially flatlined since 2013, while the world’s population just crossed to over 8B this week. As we have had yields flatline, the population has continued to rise putting stress on all forms of food production from fish to grain availability. When we zoom in a bit closer, you can see the issues the U.S. has faced since 2013 with little to no uplift over that time period. It isn’t just corn as winter wheat in the U.S. is off to it’s worst start in history. There is still some time to make up for the shortfalls, but it’s unlikely we can even eek out a modest yield given the slow start. The drought monitor in the U.S. just continues to show the underlying problems facing the U.S. The USDA world ending stocks (chart below) have drifted lower and given the broad drought issues plaguing core growing regions across the U.S., Argentina, Europe, and in most parts of Asia. India has put up gates limiting the export of wheat and rice with China purchasing as much food from the global market as possible. Alternative foods to the three above continue to move lower as well limiting the replacement products for individuals who can’t afford expensive soybeans or the rising price of wheat. Just now- there was a headline highlighting that barely prices have skyrocketed in Canada pulling more corn from the U.S. north. “Barley prices in parts of Canada have soared 30% since August and are trading near the record highs of 2021 when the nation’s harvest was the second-smallest since 1967.” According to Bloomberg, “Sky-high barley prices are turning Canada’s rare buying-spree of US corn into a habit. The price of the grain used to feed cows has soared due to pent-up demand, driving cattle ranchers to turn to US corn as a cheaper substitute to domestic barley. The shift comes one year after a severe drought withered Canadian grain supplies, spurring a switch in trade flows that led the northern neighbor to become one of the biggest buyers of corn from the US Midwest. “We need corn to fill the hole,” said Jacob Bueckert, chair of the Alberta Cattle Feeders’ Association.” Logistics and supply chains have been shifting in a major way in an attempt to address the shortfalls. There just isn’t enough product to plug all the holes that are forming, which is driving up prices around the world- including food and fertilizer. The growing shortfall of fertilizer will be supportive of pricing and incentivize more activity out of North America. The natural gas shortages have forced over 70% of fertilizer production in Europe to shutter. “Around a third of European ammonia production which shut down over the summer has reportedly ramped up in October, although overall gas demand remained subdued, ICIS research shows. Other gas-intensive production lines, particularly in the petrochemicals sector, remain closed and unlikely to return online soon unless there is a substantial decline in feedstock costs and an improvement in economic factors. Overall daily average gas demand data for the EU and UK show that consumption increased some 11% in October ’22 compared to September ’22 but the uptick was lower compared to a 24% month-on-month rise over the same period last year.” [2] The shift in production is pulling more product from the U.S into Europe while Canada exports more AMS (ammonia) to backfill what is flowing across the Atlantic. Given the shortfalls in Europe and inherent profitability on exports, we will see these flows hold firm and create growing pockets of shortages. Europe doesn’t have the ability to bring back a large part of these plants given the inherent cost of natural gas and just broad shortfalls given the lack of piped natural gas. Not only is there a shortfall from current production, but large parts of the region also relied on Russian imports of Ammonia. The loss of product from Russia + what is missing from current utilization cuts will absorb whatever is available in the market (IE US) and keep the market tight. Basic needs are the crux of survival, and economic expansion can’t begin until people not only have enough to live, but excess that can be stored or sold to allow for growth. For example, if you are worried about your next meal, will you focus on growing a garden / foraging for food, or sitting at a library to study to become a doctor, engineer, writer, or another skilled job? Food insecurity has become a big problem around the world, with Africa and Asia seeing a steady rise in basic needs not being met. The below chart is from 2019, so when we factor in prices that are now back to highs, the pain is just getting worse. 2009 was when global food insecurity really started, and now that prices have pushed back to decade highs—alongside a global pandemic impacting salaries and subsidies—the pain is just beginning. It is important to note that even without COVID19, the world was already facing several “Biblical”-sized locust swarms, droughts, floods, swine and avian flu, army worm infestations, among other disruptions that were causing yield drops. As the chart above shows, COVID19 was the cherry on top that has made a bad situation much worse—limiting the movement of migrant workers, delaying plantings, harvests, and bottlenecks at ports. We have seen an increase in acres planted, but weather hasn’t been cooperative, delaying key planting across places like Latin America. Planted acres are now expected to fall as soils are depleted, and the cost to rejuvenate them becomes an insurmountable hurdle. These adjustments take seasons, and with China absorbing massive amounts of grains in the market and dealing with a new round of swine flu driving up prices, poor countries will be left paying up for goods to feed their people. Nationalism will also become a bigger issue as countries withhold exports, managing volumes and pricing, to make sure their citizens have enough to eat. We saw evidence of this at the outset of the pandemic, and restrictions still remain in place with export quotas and rising tariffs. Many countries are out of inventory and are relying on shipments to keep their population fed. Every crop is facing a unique problem and the farmers are desperate… more fertilizer application is the only near term solution. [1] https://www.worldbank.org/en/topic/agriculture/brief/food-security-update[2] https://www.icis.com/explore/resources/news/2022/10/31/10820515/insight-crashing-gas-spurs-fertilizer-ramp-up-petchems-still-shuttered/ [/ihc-hide-content] [ump-visitor ] To unlock the content you need a Enterprise Account! [/ump-visitor] [ump-logged-user ] This content is visible only for Enterprise Account! [/ump-logged-user]