- Expect a delivery delay of NEX’s electric frac fleets and decommission of ~150,000 horsepower.

- Natural gas price’s continued weakness means some frac fleets could be released in Haynesville, resulting in a significant decline in production.

- However, NEX’s return-focus strategy has improved the return on invested capital by 30%.

- In FY2023, the company expects to generate $500 million in free cash flow.

Company Strategy And Challenges

In the Q4 earnings call, NexTier Oilfield’s (NEX) management partially changed its bullish stance. While it remains convinced about the ongoing demand-side recovery, the supply side has faced more challenges than previously anticipated. Capital discipline, supply chain issues, and inflation will cause new builds to delay further. Therefore, even if pricing gains traction due to the demand-supply mismatch, NEX will likely see a delivery delay of its electric frac fleets, at least until Q2 2023. In the fracking industry, natural gas-fueled assets are expected to earn a premium return because of price increases and limited frac capacity expansion.

Over the next year and a half, it plans to decommission ~150,000 horsepower. This is because it focuses on allocating capital to the highest return investment while disinvesting older equipment. While the strategy will improve returns, it will offset revenue growth potential.

The natural gas price’s continued weakness over the past few months means NEX has adjusted its basin strategy effectively. In the Marcellus, limited takeaway capacity has constrained activity there compared to other gas basins. Because the breakeven well economics is at a lower point, the basin activity will likely be relatively steady despite the drop in natural gas prices. A more drastic outcome is set to visit Haynesville, where NEX’s management believes 14 frac fleets could be released, resulting in a significant decline in production.

Given NEX’s importance on gaining capital efficiency, which we discussed in our previous article, it delivered an annualized ROIC of 46% in Q4. Overall, the return on invested capital has improved by 30% over the past year through capital reduction. It has invested in counter-cyclical measures and rationalized its asset base. It sold $50 million of non-core assets in FY2022. Also, as a part of the strategy, earlier, it deployed the legacy Tier 4 dual-fuel fleet and upgraded the Tier 4 dual-fuel fleet through the Alamo operations in Q1 2022, as I discussed in one of my previous articles.

Q1 2023 Forecast And Projects

NEX’s management thinks returns can stay high because the market will remain undersupplied and consolidated. The industry is currently undergoing a conversion to natural gas, which would ease pricing and improve margins. Given the industry factors, NEX’s management expects revenue to increase by ~6% sequentially. In FY2023, the company expects to generate $500 million in free cash flow. As a result of attrition and horsepower deployment throughout the year, the FY2023 capex budget remains unchanged versus the previous guidance at $350 million. Much of the budget is geared toward 1H 2023 as it plans to invest early to maximize returns.

The Industry Drivers

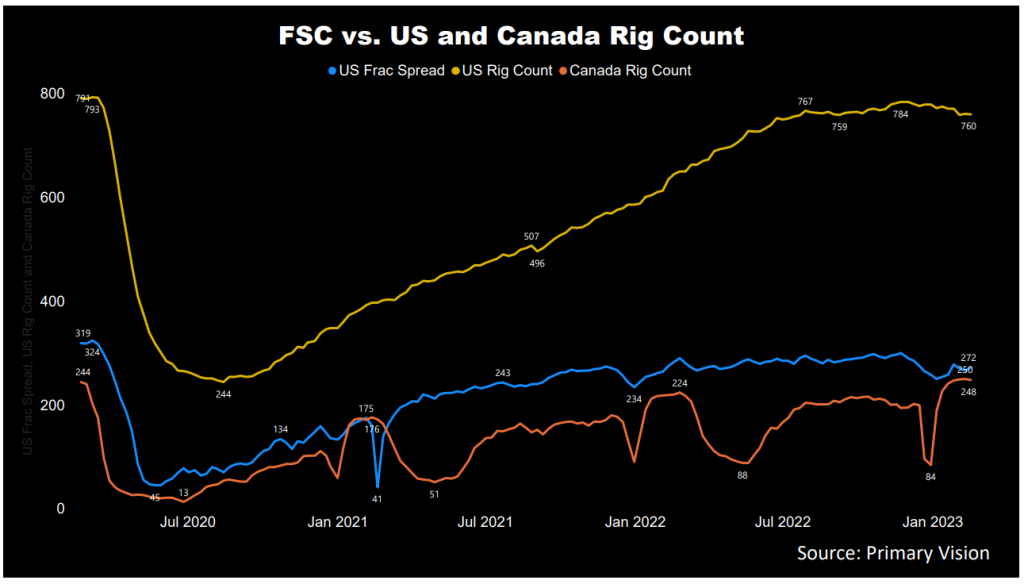

According to Primary Vision’s forecast, the frac spread count (or FSC) reached 266 by the second week of February and has inched marginally down over the past year. Over the past month, we saw 14 frac fleets removed from the count in the US. A falling frac count is negative for NEX’s growth. The drilled wells increased by 42% in the past year until January 2023, according to the EIA’s latest Drilling Productivity Report. After a continuous fall for several months, the drilled but uncompleted wells (or DUC) have reversed the trend and have risen for the past two months. The West Texas Intermediate (WTI crude oil) price remained volatile, with a downtrend in recent months as the supply side remains restricted.

Analyzing The Q4 Drivers

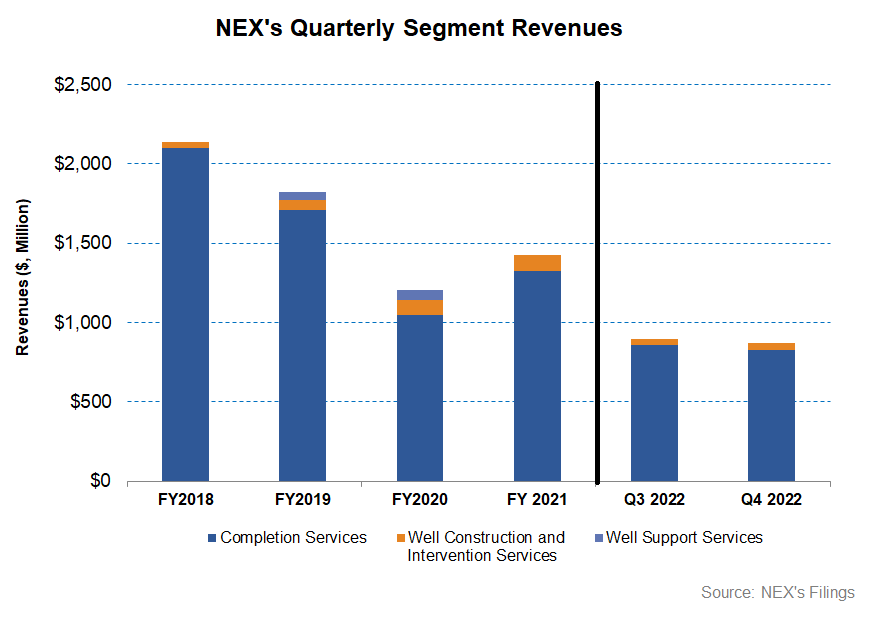

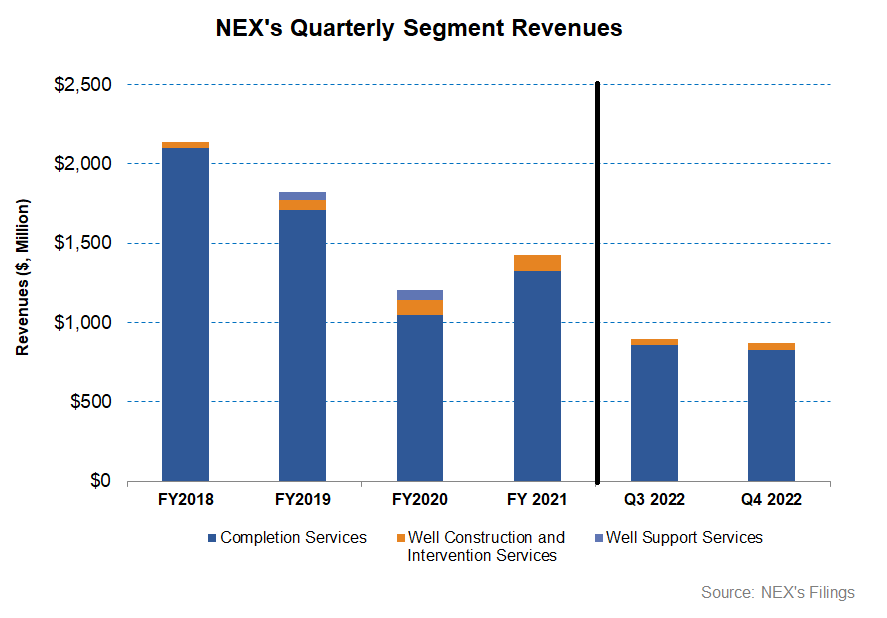

In Q4 2022, NEX’s revenues decreased by ~3% compared to Q3 2022. Lower sales reflected the company’s strategy to shift to lower-revenue-but-higher-return work. However, strong revenues from services and pricing offset some of the revenue losses.

Sequentially, revenues decreased by 3% in the Completions Services segment in Q4. Despite that, the adjusted gross profit expanded by 11%. However, revenues and gross profit in the Well Construction & Intervention Services segment increased by 7% and 38%, respectively. Higher demand and pricing in the Cement product line caused the rise in revenue and profitability in this segment.

Cash Flows And Capex

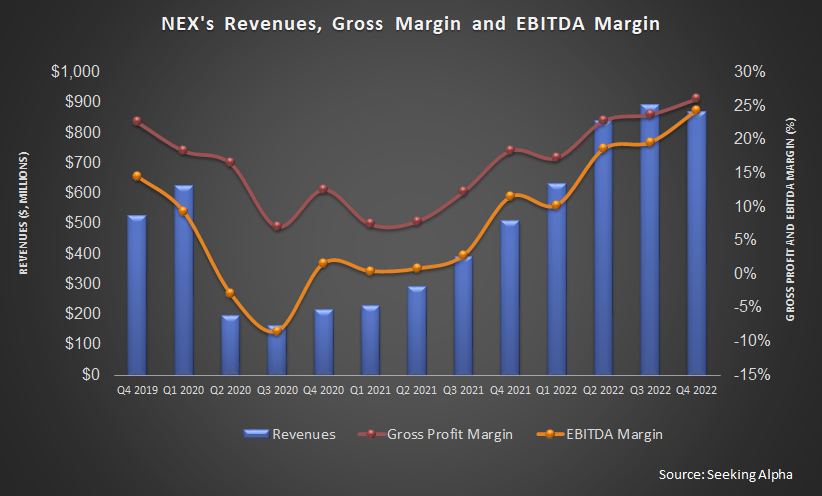

In FY2022, NexTier Oilfield’s cash flow from operations (or CFO) turned significantly positive ($454 million) compared to a negative CFO a year ago. Steeply higher revenues and a lower cost structure led to the CFO’s rise. In the past year, free cash flow also turned strongly positive ($229 million).

NEX’s 2023 capex budget is $350 million, 89% higher than a year ago. The FY2023 capEx budget remains unchanged versus the previous guidance. In FY2023, the company expects to generate $500 million in free cash flow. In FY2023, it plans to grow free cash flow to adjusted EBITDA ratio by 40% to 50% compared to FY2022.

The company plans to return at least 50% of this free cash flow to shareholders. The company’s liquidity totaled $634 million as of December 31, 2022. Its debt-to-equity ratio (0.44x) improved compared to a quarter earlier.

Learn about NEX’s revenue and EBITDA estimates, relative valuation, and target price in Part 2 of the article.