- The Arcadia segment’s margin growth is limited in the near term but will gradually improve by the end of 2023.

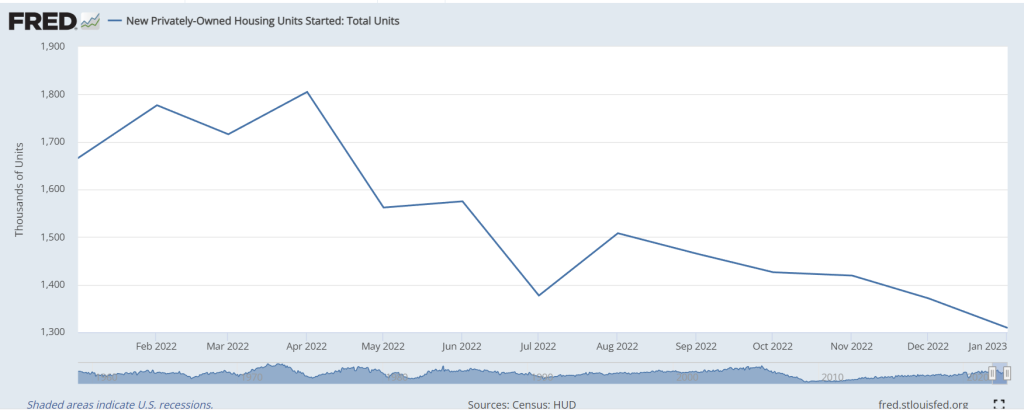

- However, declining new privately-owned housing units in the past year is a worrying sign.

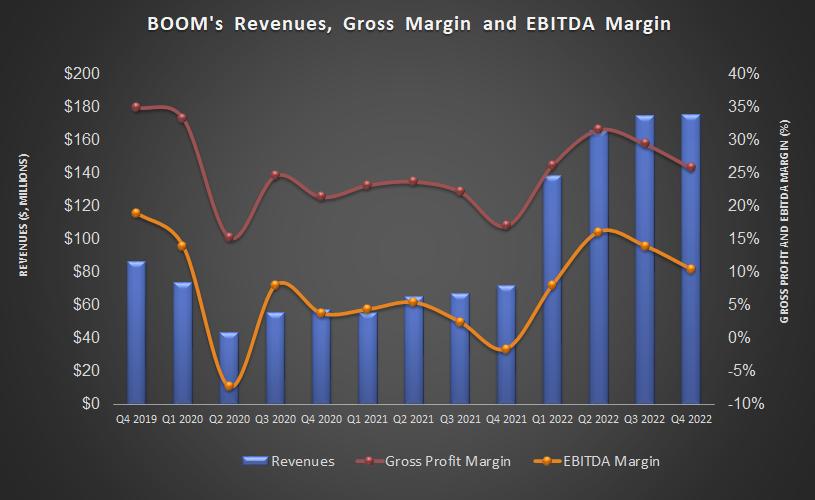

- At DynaEnergetics, inventory write-offs and reserves offset improved product mix and price increases.

- BOOM’s cash flows turned positive in FY2022 while its leverage remains low.

The Arcadia Segment Dynamics

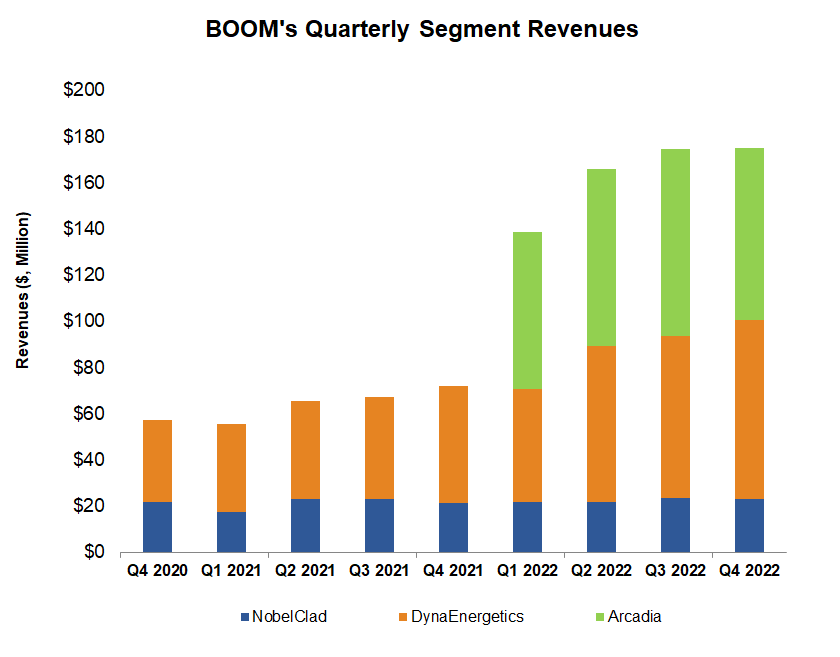

In December 2021, DMC Global (BOOM) acquired 60% ownership in Arcadia, a leading US supplier of architectural building products, and added the capability for high-end homes using Arcadia’s engineering-built products for commercial buildings and residential real estate. In Q4 2022, sales increased by 31% in this segment versus a year ago, driven by price increases, mainly aimed at blunting the raw material cost hike. Much of the price rise transpired in 2H 2022, while the effect will trickle because of the lag between a spike in aluminum prices and product price increases.

Investors may note that Arcadia Custom, which serves the high-end residential market, will continue to have backlog priced before the repricing until 2H 2023. However, healthy demand and order backlogs favor a stronger topline in this business. So, Arcadia’s margin growth is limited in the near term but will gradually improve by the end of 2023.

What’s Happening in DynaEnergetics And NobleClad?

Let us now discuss BOOM’s perforating product suite. Read our previous article to understand why BOOM’s integrated perforating gun system has a distinct advantage over the assembled products available in the market. Recently, BOOM added three large customers in North America, resulting in a 40% higher fully integrated DS perforating system in 2022 compared to 2019. Increased demand for North America’s well-completion industry and capacity expansion at its manufacturing capacity in Texas facilitated the increase. Although positive, the impact on the operating margin for the DynaEnergetics segment was relatively low due to inventory write-offs and reserves. With improved product mix and price increases, the management expects to grow by a margin to the low 30% range in 2023. In Q4, the segment gross margin was 28%.

In NobleClad, the Order backlog increased 16% sequentially in Q4 due primarily to robust demand from the liquified natural gas industry for its Cylindra cryogenic transition joints. The segment plans to participate in the vendor selection phase in some large projects. However, there is no certainty at this point that such initiatives will be successful. So, the topline and margin expansion is somewhat uncertain here.

The Industry Indicators

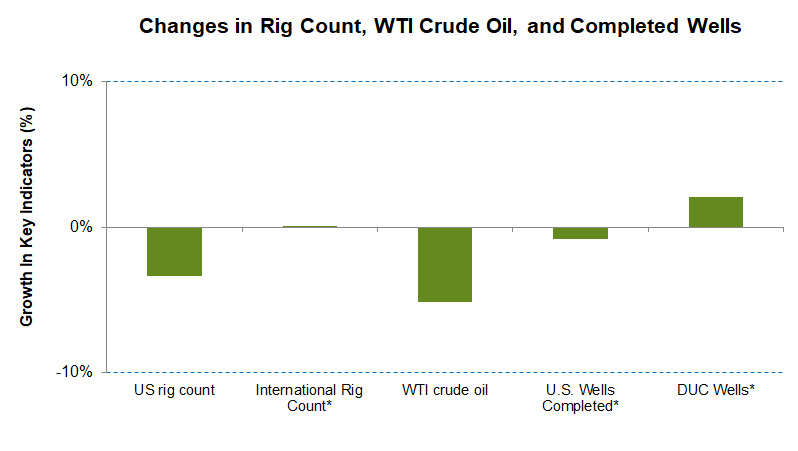

Most energy indicators moved sideways in Q4 and then weakened in Q1 following the global economic recession and the Ukraine conflict. Since the start of 2023, the crude oil price declined by 5%. The US rig count went down by 3.3% during this period. The international rig count was unmoved. However, the drilled-but-uncompleted wells grew in the key US shales after continuously falling for many months before that.

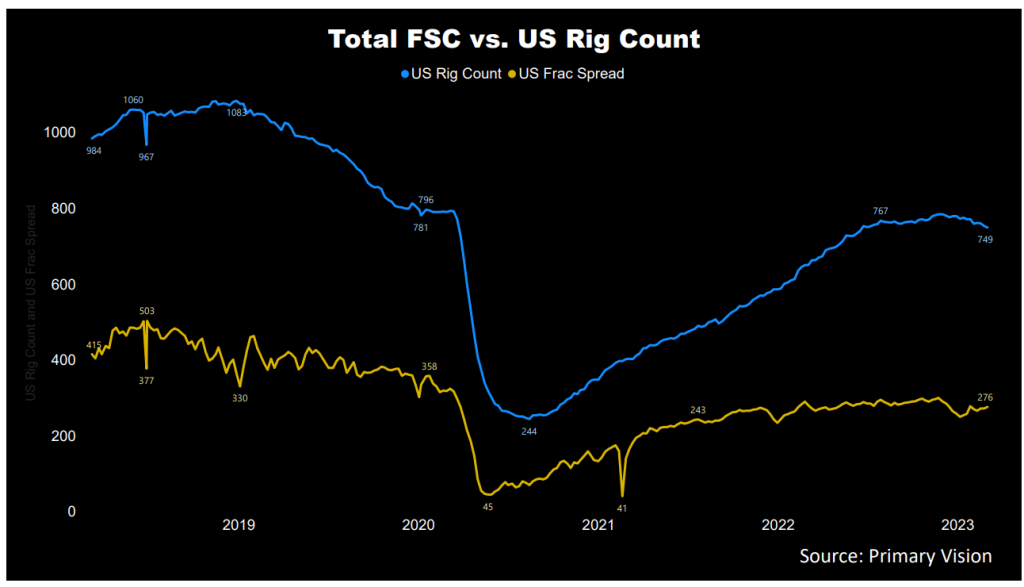

According to Primary Vision, the frac spread count has recovered in 2023 to 276 by the first week of March compared to the start of the year. The higher frac count can improve BOOM’s topline in Q1 2023.

According to the FRED economic data, the new privately-owned housing units declined significantly in the past year until January (21% down). The rising interest rates appear to be affecting most of the residential market chain. So, DMC’s Arcadia segment will likely suffer in the short term.

Q1 2023 Guidance

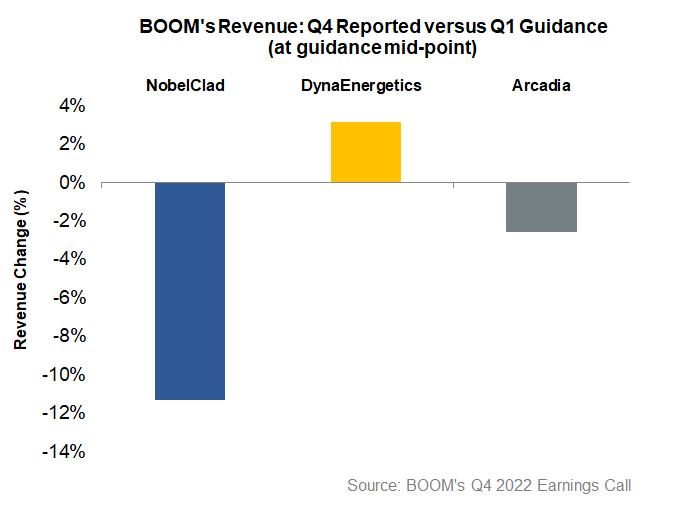

DMC Global expects the top line to decrease by 7% in Q1 2023. Revenues in the Arcadia segment can go down by 3% (at the guidance midpoint. DynaEnergetics segment revenues are expected to decline the most (11% projected fall).

Company-wide, the gross margin can expand by 150 basis points (at the guidance mid-point) due to the positive changes in the margin in DynaEnergetics and Arcadia. However, the expansion was limited by a less favorable project mix in the NobelClad segment. On the other hand, the management expects the NobelClad segment’s topline to improve marginally (by 3%) in Q1. The management also expects the SG&A expense to decrease in Q1 2023 compared to Q4 2022, which can positively impact net earnings in Q1.

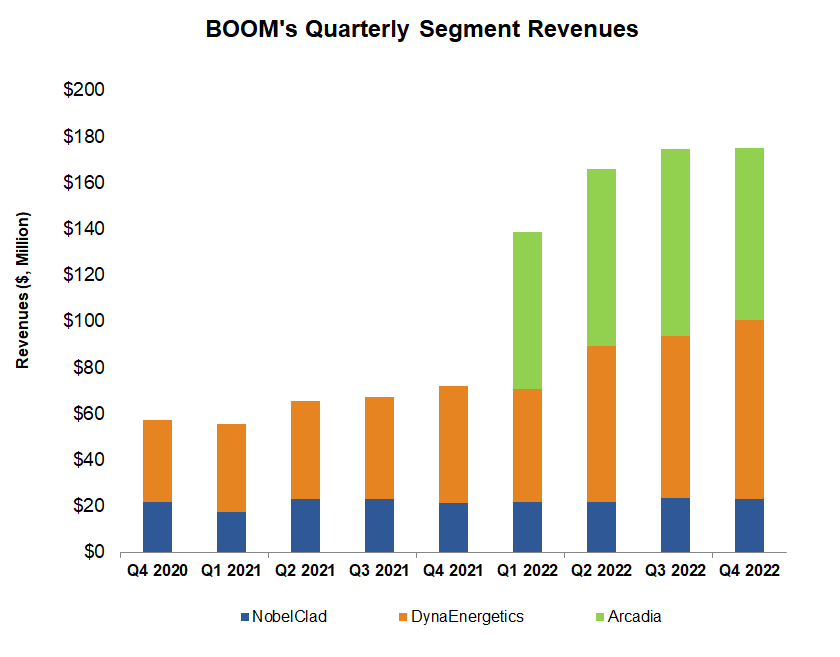

How Did The Segments Perform In Q4?

Increased demand in North America and a 56% higher growth in the DynaStage system led to DynaEnergetics segment revenue increased by 10% in Q3 2022 compared to Q2. The Arcadia segment revenues, in contrast, decreased by ~8% in Q4 due to the adverse effects of seasonality and maintenance. However, the segment’s average selling price improved year-over-year. In NobelClad, revenues decreased by 1.2% quarter-over-quarter in Q4 due to higher raw material costs.

Cash Flows And Balance Sheet

In FY2022, BOOM’s cash flow from operations (or CFO) turned positive compared to a negative CFO a year ago, led by significantly higher revenues during this period. Free cash flow also turned positive in FY2022. The company plans to repay the long-term debt associated with the Arcadia acquisition and for distributions to the Arcadia joint venture partner through higher cash flow generation.

BOOM had total debt of $133 million as of December 31, 2022. Its leverage (debt-to-equity) of 0.35x is lower than many of its peers, and its liquidity (cash plus available credit facility) was $75 million. So, the financial risks are limited due to positive FCF and low leverage.