Industry Outlook

We discussed our initial thoughts about SLB’s (SLB) Q1 2023 performance in our short artcile a few days ago. In this article, we will take a deeper dive into the reasons and its current outlook. SLB’s industry outlook carries several similarities to Baker Hughes’s (BKR), which we have already discussed in our article on BKR. SLB sees the current capex cycle as durable and less sensitive to commodity price swings, despite the short-term economic and demand uncertainties. The weight of energy security and structural investments will pave the way for long-cycle projects in the Middle East, international offshore basins, and natural gas projects. On the other hand, the North American market has higher short-cycle exposure and, therefore, will be impacted more by an anticipated activity plateau and production volume shrinkage in the short term.

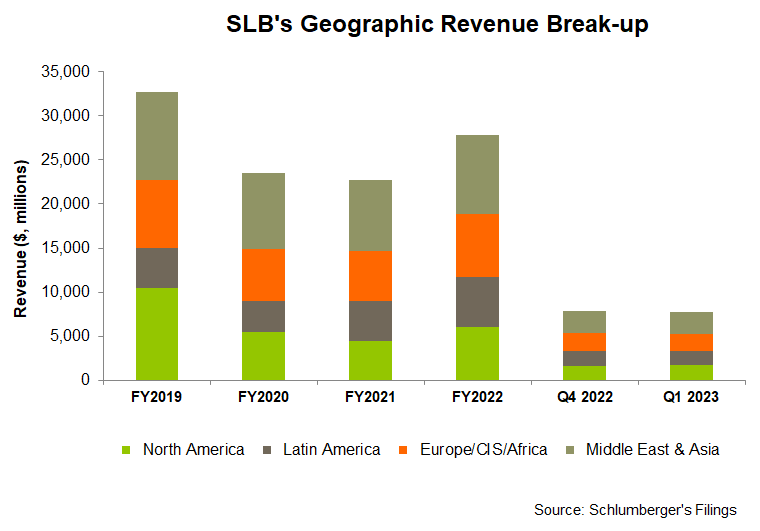

Because international activity accounted for 78% of SLB’s Q1 2023 revenues, it is essential to understand the outlook of the company’s operations outside the purview of the US. The Middle East is going through an investment upcycle, supporting capacity expansion projects over the next four years. In 2023, its revenue is set to increase massively in the Middle East. The other rapid growth point is international offshore, with more than $200 billion in new projects through the next two years. Similarly, in Latin American countries like Guyana and Brazil, large development projects are ramping-up and starting to scale.

In West & South Africa and the East Mediterranean, exploration and appraisal activities gather momentum as these countries see new licensing rounds and new blocks awarded. Following balanced growth in various international markets, SLB’s management is confident of a multi-year durable offshore investment.

Backlog & New Energy Order

The industry growth, as outlined above, can translate into opportunities for improved reservoir performance (exploration & appraisal activity) and long-term growth potential for SLB’s Production Systems division. In this division, SLB’s management expects FY2023 cumulative bookings to be ~$10 billion – $12 billion. Out of this, it has already booked over $3 billion in Q1, while the current momentum supports strong bookings through at least 2025. So, SLB’s exposure to the deepwater subsea market would push topline growth and a significant installed base for services.

SLB has undertaken various initiatives in New Energy, including Carbon Capture and Sequestration (or CCS) activities. Currently, the company participates in around 30 such projects globally. The CCS initiative has received a shot-in-the-arm from the US Inflation Reduction Act. The company expects to receive more such awards in the coming quarters worldwide.

Q2 and FY2023 Forecast

We expect the solid international growth to offset much of SLB’s slowdown related to the ongoing weakness in natural gas prices. In FY2023, the management anticipates revenue growth of more than 15% and an adjusted EBITDA growth in the “mid-twenties.”

In Q2, the company expects revenue growth of “mid-to-high single digits” compared to Q1. Its operating margins can expand by 50 to 100 basis points, led by improved activity levels in the Middle East & Asia Area and the momentum in the offshore markets.

Analyzing The Q1 Drivers

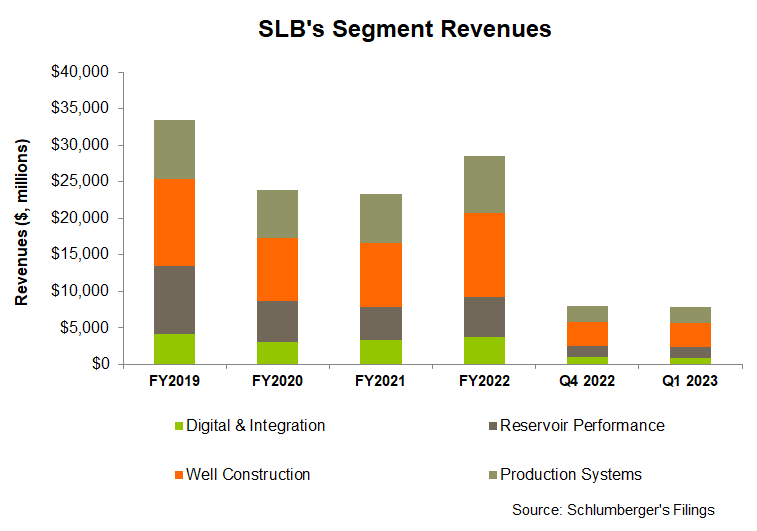

The company’s Digital & Integration segment saw the steepest quarter-over-quarter revenue decline in Q1 (12% down), followed by Reservoir Performance (3% down). Lower revenues from APS projects, lower digital & exploration data license sales, and seasonality in Europe and Asia adversely affected the company’s Digital & Integration segment revenue and income in Q1 2023.

On the other hand, Well Construction saw a stable topline due to continuous onshore and offshore activity in North America, Latin America, and offshore Africa. Higher drilling, measurement, and integrated well construction activity expanded the operating margin in Q1.

Cash Flows, Balance Sheet & Shareholders’ Returns

SLB’s cash flow from operations witnessed a spectacular rise in Q1 2023 over the previous year, led primarily by the year-over-year revenue rise. Capex, too, increased, and as a result, free cash flow (or FCF) remained in the negative territory, although it improved over Q1 2022. It spent $244 million on investments, primarily related to the Gyrodata acquisition. In FY2023, the company expects capex to increase by ~11% compared to FY2022.

SLB’s debt-to-equity (0.70x) remained nearly unchanged from a quarter ago. The net debt or equity structure did not change much during Q1 2023 from the previous quarter. SLB’s annual dividend is $1.00 per share, amounting to a 2.01% forward dividend yield. During Q1, it repurchased shares worth $230 million. This is part of its target to return $2 billion to shareholders between dividends and stock buybacks in 2023.

Relative Valuation

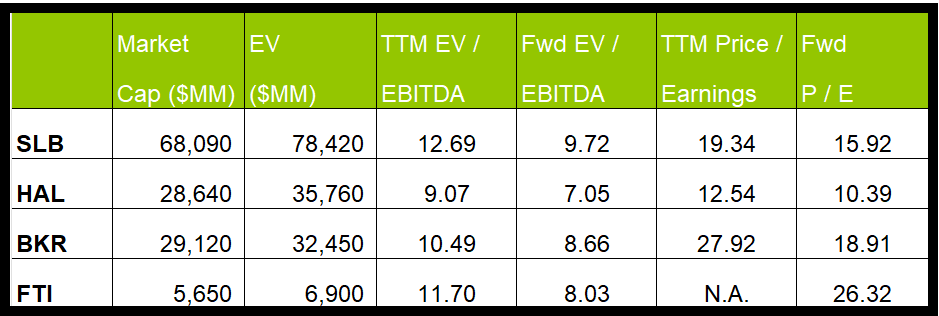

SLB is currently trading at an EV-to-adjusted EBITDA multiple of 12.7x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 9.7x. The current multiple is lower than its past five-year average EV/EBITDA multiple of 12x.

SL’s forward EV-to-EBITDA multiple contraction versus the current EV/EBITDA is nearly as steep as its peers because its EBITDA is expected to increase as much as its peers in the next year. This typically results in a similar EV/EBITDA multiple compared to its peers. The stock’s EV/EBITDA multiple is higher than its peers’ (HAL, BKR, and FTI) average. So, the stock is relatively overvalued versus its peers.

Final Commentary

A near dichotomy runs through SLB’s near-term outlook. On the one hand, the company’s North American market, with higher short-cycle exposure, will be impacted more by an anticipated activity plateau and production volume shrinkage. On the other, energy security and structural investments will pave the way for long-cycle projects in many of its international operations, particularly in natural gas projects. SLB is predominantly international activity-focused, following balanced growth in different international markets, so a multi-year durable offshore investment will likely follow the current transition. A rapid growth point is international offshore, with more than $200 billion in new projects through the next two years. Plus, it has undertaken various initiatives in CCS activities, participating in several global projects.

Despite the robust growth opportunities, investors need to be wary of the pitfalls in SLB’s operating performance. In Q1, it recorded lower digital & exploration data license sales, while seasonality in Europe and Asia affected performance adversely. Its free cash flows remained in negative territory. Also, the stock is relatively overvalued at this level compared to its peers.