Frac’ing Outlook and HAL’s Strategies

We have already discussed Halliburton’s (HAL) Q1 2023 financial performance in our recent article. Here is an outline of its strategies and outlook. Halliburton, followed by natural gas price’s crash over the past six months, has reduced its exposure to the gas market by 30%. This somewhat contrasted with other oilfield services companies like Liberty Energy (LBRT), which continues to transition from diesel to natural gas. It retired a Tier 2 diesel fleet to reduce maintenance costs and focused more on electric fleets. The company’s management expects North American upstream capex to grow ~15% in 2023, and the highly efficient equipment and services market will remain tight.

So, HAL is guided by the same overriding principle of deploying fuel-efficient energy and power generation because they typically lead to high-return opportunities and offer mobile power generation technology. Since 2019, the company estimates that its pumping utilization has increased by 60% in North America. It has also invested in differentiated products and services to improve margins. Halliburton has been using its SmartFleet intelligent automated fracturing system since 2020. It deploys fiber optics to see, measure and act on real-time downhole measurement. The company has introduced Zeus electric fracturing system, which offers grid power solutions. It can use as all-electric or half-electric and half-dual fuel frac spreads, which can be transitioned to electric at their own paces. The company deployed its e-frac fleets on multiyear contracts in North America.

New technology update

Halliburton has combined iCruise and iStar – its drilling and logging-while-drilling platforms with LOGIX, its automation platform in the offshore reservoir section in Norway. It also recently employed its wireline imaging technology (STRATA Examiner) to increase reserve estimates for a Mediterranean Sea campaign. It also demonstrated an offshore automated cementing system in the North Sea. Various operators, including Hess, Repsol, and Petrobras have recently used Halliburton Landmark’s DecisionSpace 365 applications.

HAL’s Q2 forecast

In Q2, Halliburton expects software sales to soften due to the typical seasonality. But improvements in global drilling activity can slow down the deceleration. So, its Drilling and Evaluation division can increase by “low to mid-single digits” in Q2 compared to Q1. The operating margin in this division can decline by 50 to 100 basis points.

The Completion and Production division revenue can increase “low to mid-single digits,” while the operating margin can improve by “25 to 75 basis points.” You can read more about Halliburton’s outlook in our article here.

Natural Gas Price Dictates Frac Spread Strategy

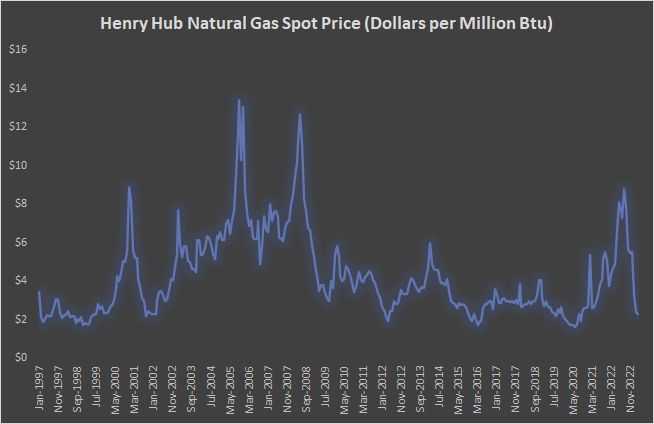

In the US, the Ukraine-Russia conflict and lower winter demand in Europe pushed the natural gas price to an abysmally low level. In the past year, until March 2023, it declined by 53%. Despite the ongoing weakness, HAL’s management expects an additional LNG export capacity amounting to 6 billion cubic feet per day would resolve the current issues over the next couple of years. Due to the short-term price fragility, HAL will likely move three frac spreads from gas to oil basins.

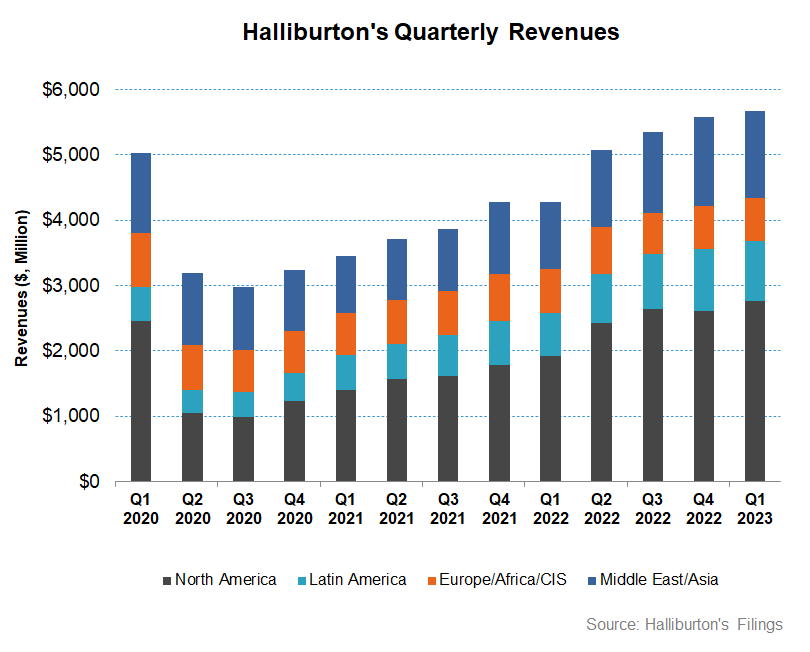

Key Q1 Drivers

Geographically, only North America witnessed steady growth (6% up), while Latin America saw the steepest decline (3% down). In North America, pricing traction increased well construction services, stimulation activity, and various product lines in the Gulf of Mexico. Revenues from Latin America, on the other hand, declined by 3%. In many other regions, the company’s topline weakened due mainly to the sale of its Russian operations and decreased activity in Norway.

Between the two operating segments (Completion & Production and Drilling & Evaluation), the C&P segment shrank its operating margin by 120 basis points. In contrast, the operating margin was steady in the D&E segment in Q1 2023 compared to a quarter earlier.

Cash Flow & Balance Sheet

HAL’s cash flow from operations turned significantly positive in Q1 2023 compared to a negative CFO in the previous year, led primarily by the year-over-year revenue rise and improvement in working capital. However, capex, too, increased, and as a result, free cash flow (or FCF) remained in the negative territory, although it improved over Q1 2022.

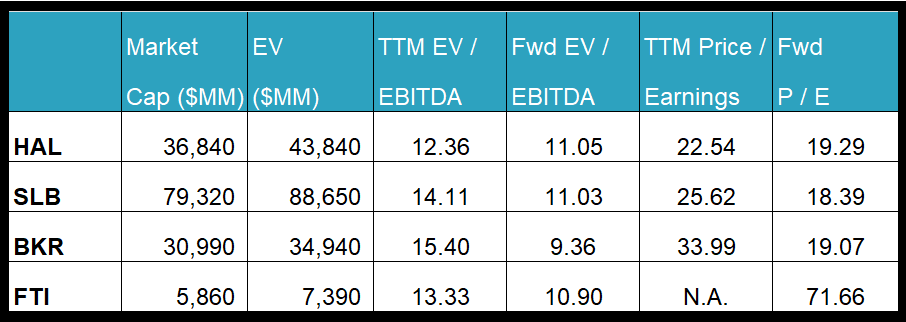

HAL’s debt-to-equity of 0.94x is higher than many of its peers (SLB, BKR, and FTI). The company’s management expects to generate strong free cash flow in 2H 2023. It plans to return ~50% of annual free cash flow to shareholders. With that aim, it repurchased $100 million of common stock in Q1.

Relative Valuation

Halliburton is currently trading at an EV-to-adjusted EBITDA multiple of 12.4x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 11.1x. The current multiple is slightly higher than its five-year average EV/EBITDA multiple of 11.5x.

HAL’s forward EV-to-EBITDA multiple contraction versus the adjusted current EV/EBITDA is less steep than peers because the company’s EBITDA is expected to increase less sharply in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is lower than its peers’ (SLB, BKR, and FTI) average. So, the stock is reasonably valued versus its peers.

Final Commentary

The natural gas price’s free fall over the past several months forced Halliburton to re-evaluate its strategy. It has decided to move three frac spreads from gas to oil basins. Instead, it has invested in differentiated products and services to improve margins and frac spread utilization. The company focuses more on the electric frac system like the Zeus electric fracturing system, which can use as all-electric or half-electric and half-dual fuel frac spreads. It will also integrate its digiFleets, dual fuel fleets, and CNG supply chain through the Siren acquisiton and launching a new division called Liberty Power Innovations

In Q2, it may face hurdles from lower software sales the typical seasonality, although improvements in global drilling activity can push performance higher. So, the management expects its topline and margin to improve. With strong free cash flow in 2H 2023, it plans to return ~50% of annual free cash flow to shareholders. The stock is reasonably valued versus its peers at this level.