Mixed Outlook: ProFrac (ACDC) expects to see steady pricing in the Stimulation Services segment, which can lead to higher profitability per fleet because of a lower cost structure. It also expects a higher demand for electric and Tier 4 dual fuel (DGB) technologies. However, in the Proppant Production segment, it expects volumes and pricing to deteriorate.

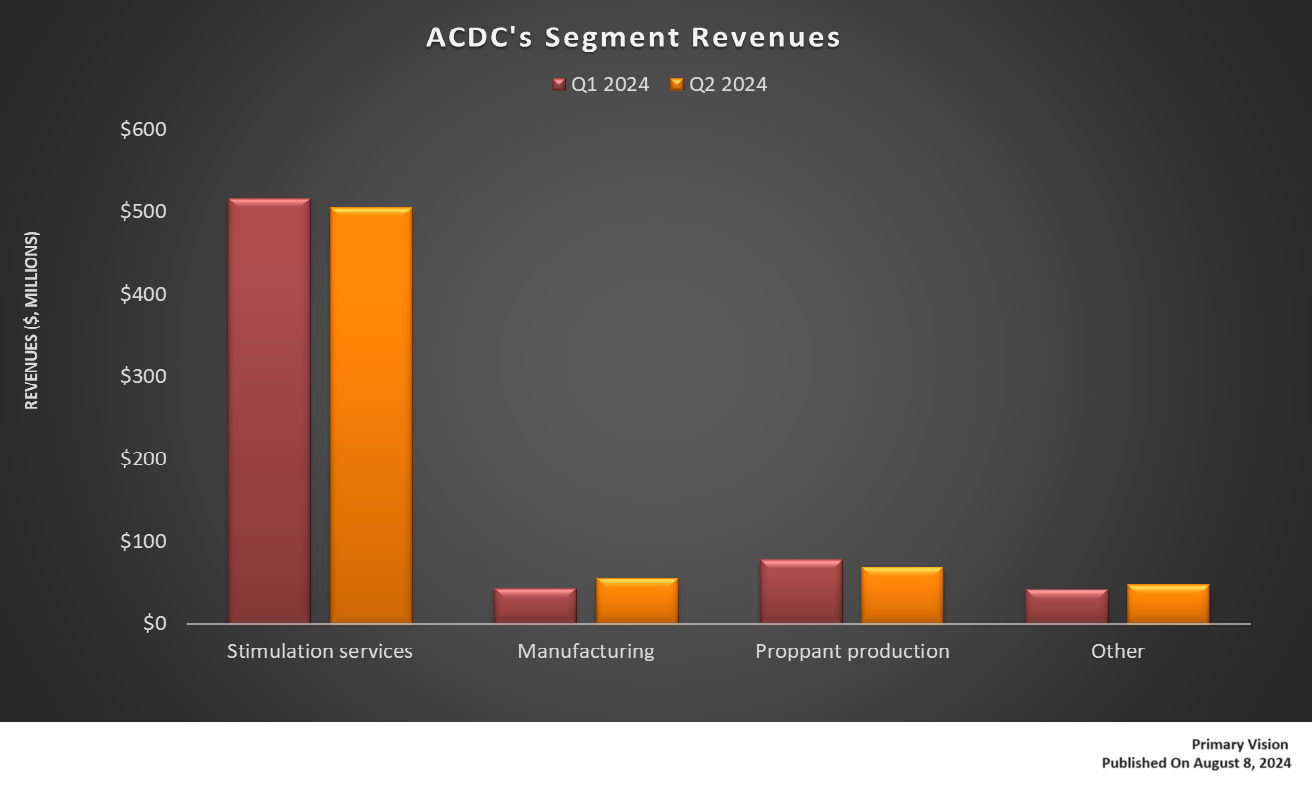

Segment Performance In Q2: From Q1 to Q2, ACDC’s revenues from the Manufacturing and Other segments improved (29% and 14% up, respectively), while its revenues from Proppant Production (11% down) and Stimulation services (2% down) fell. Quarter-over-quarter, the company’s adjusted EBITDA margin shrank by 410 basis points as operators reduced drilling and completion activity in natural gas basins. Read more about ACDC in our recent article here.

Cash Flows Fell In 1H 2024: The company’s free cash flow declined steeply in 1H 2024 over a year ago due to a substantial cash flow from operations decline. In 1H 2024, its capex fell from a year ago. Its projected growth capex for FY2024 is much lower than the maintenance capex.

Thanks for reading the ACDC Take Three, designed to give you three critical takeaways from ACDC’s earnings report. Soon, we will present a second update on ACDC earnings highlighting its current strategy, news, and notes we extracted from our deeper dive.