FTI’s Strategies

We have already discussed TechnipFMC’s (FTI) Q2 2024 financial performance in our recent article. This article will dive deeper into the industry and its current outlook. In Q2, FTI had an inbound order of $3.1 billion. In Subsea, FTI grows through collaboration and long-standing partnerships. Its recent orders include IEPCI projects and an incremental order for flexible pipe from Petrobras.

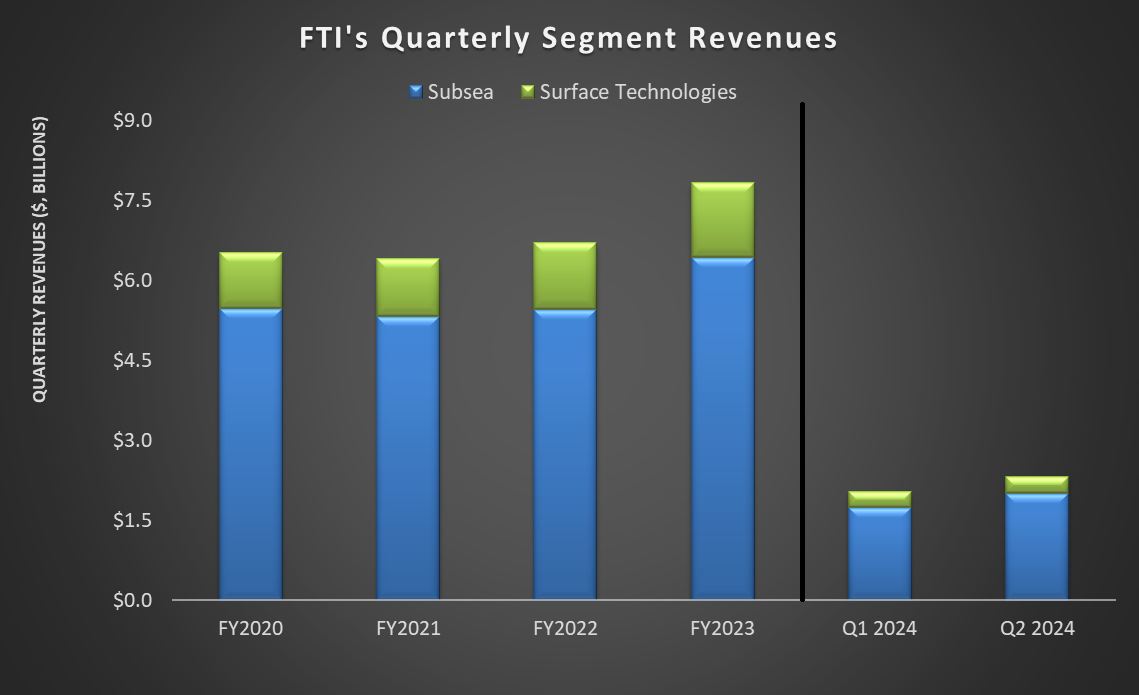

In Guyana, ExxonMobil’s Whiptail project was a key order that will utilize its Subsea 2.0 systems and manifolds. As a result of incremental orders and IEPCI project activity in the North Sea and Gulf of Mexico, its Subsea revenues increased by 16% quarter-over-quarter in Q2.

Outlook And Forecast

FTI’s backlog was $13.9 billion after Q2. The consistency of the project awards is reflected in book-to-bill remaining above 1x in ten of the last 11 quarters. The management expects to record an adjusted EBITDA of ~$1.35 billion (excluding the impact of foreign exchange). In Subsea, it expects the backlog to reach $10 billion by the end of 2024. This can translate into achieving $30 billion in orders over the three-year period ending 2025, which can drive backlog in the medium term. In 2025, the company expects Subsea revenue of $8 billion while adjusted EBITDA margin can inflate to 18%.

In Q3, FTI expects revenues and adjusted EBITDA margin to remain unchanged from Q2 in Subsea and Surface Technologies. For FY2024, it increased its revenue and adjusted EBITDA margin guidance. Now, it expects to generate subsea revenues of $7.6 billion—$7.8 billion and an adjusted EBITDA margin of 16.5% to 17%. Over the next four years, the subsea EBITDA margin can potentially see a 450 basis point improvement.

Next Growth Drivers

In Q2, FTI employed a production system in the Shell Sparta project in the Paleogene play in the U.S. Gulf of Mexico. Apart from new shale plays, FTI is also interested in basins that are relatively new to the mix. It anticipates robust activity in Guyana and Mozambique. Emerging natural gas basins, which are expected to be operational by 2028, include South Africa, Tanzania, Colombia, Mexico, and the Eastern Mediterranean. It also plans to deliver the first iEPCI, which will encompass an all-electric subsea system for a carbon capture and storage project.

Among new markets, CCS (Carbon capture and storage) can become the primary oil electric subsea system market. BP Northern Endurance Partnership Project is one such example. Here, CO2 will be sequestered from the emitter onshore and will be taken offshore and stored permanently. FTI’s primary market will be brownfield tiebacks in the oil and gas market. The company estimates that oil and gas production facilities are operating at 60%-70% of nameplate capacity because of reservoir declines. FTI’s tieback solutions can link stranded reservoirs back to these existing host facilities, which can have improved returns.

Key Q2 Metrics

Revenues in the company’s subsea operating segment rose 16% quarter over quarter in Q2. The top line in the Surface Technologies segment increased by 2.9%. Operating income in the subsea segment increased significantly by 70% in Q2. In contrast, operating income in the Surface Technologies segment decreased by 77%.

FTI’s cash flow from operations strengthened and turned positive in 1H 2024 from a steeply negative cash flow a year ago. Debt-to-equity (0.76x) also showed an improvement from FY2023. During Q2, it repurchased shares worth $100 million to improve shareholder returns. In FY 2024, it expects an FCF of $425 million-$575 million.

Relative Valuation

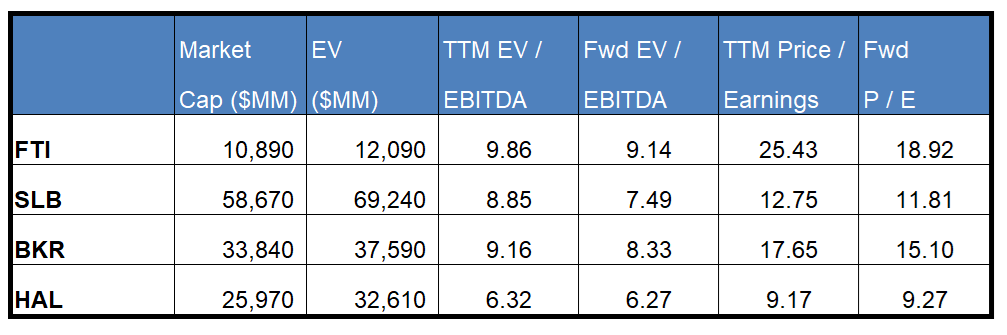

FTI is currently trading at an EV-to-adjusted EBITDA multiple of 9.9x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is 9.1x. The current multiple is higher than its five-year average EV/EBITDA multiple of 8.1x.

FTI’s forward EV-to-EBITDA multiple contraction versus the adjusted current EV/EBITDA is less steep than peers’ because the company’s EBITDA is expected to increase less sharply in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is higher than its peers’ (SLB, BKR, and HAL) average. So, the stock is relatively overvalued compared to its peers.

Final Commentary

In Q2, FTI received several orders and IEPCI project activity in Guyana, the North Sea, and the Gulf of Mexico. With a consistently healthy book-to-bill ratio, it expects the backlog to reach $10 billion by the end of 2024. It also expects its Subsea revenue and adjusted EBITDA margin to inflate in 2025. The Subsea margin can significantly expand over the next four years.

In addition to traditional shale plays, FTI anticipates growth opportunities from new and emerging shale plays in the GoM and internationally to become active drivers in the medium term. It also expects the brownfield tiebacks market to grow as reservoir nameplate capacity declines. With improved cash flows in 1H 2024, shareholder returns increased through share repurchase. The stock is relatively overvalued compared to its peers at this level.