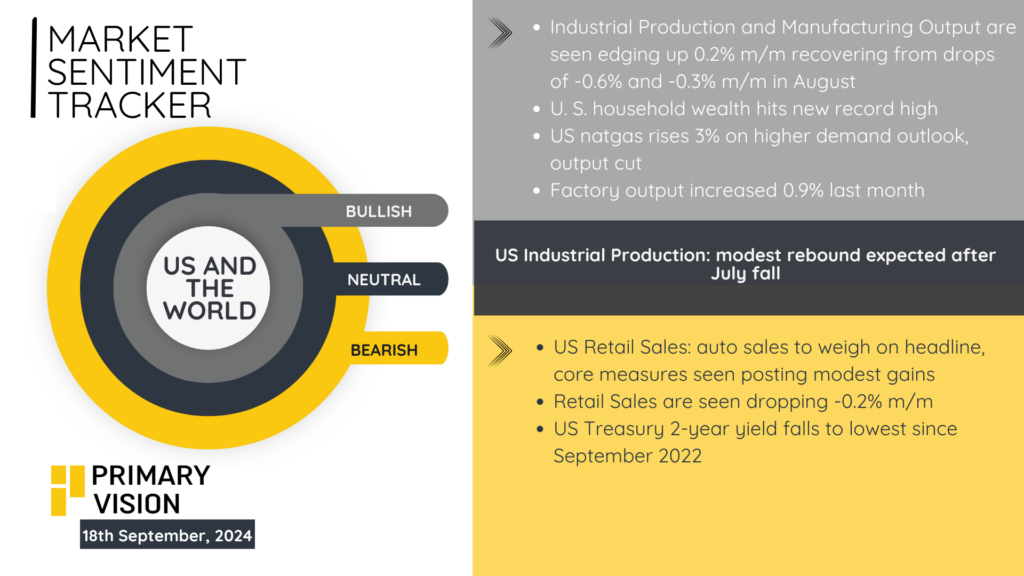

The latest economic data points to mixed signals for the U.S. and global economy. U.S. industrial production is expected to rebound with a modest 0.2% increase in September after a contraction of -0.6% and -0.3% in August. Factory output rose by 0.9% last month, showing signs of recovery.

Retail sales, however, are projected to decline by -0.2% m/m, with auto sales weighing heavily on the headline figure, although core measures are expected to post slight gains. Meanwhile, U.S. household wealth has hit a record high, adding a bullish tone to the market sentiment. Natural gas prices rose by 3% on higher demand and output cut expectations, supporting energy markets. On the bond side, the U.S. Treasury 2-year yield dropped to its lowest since September 2022, signaling increased uncertainty and possibly a flight to safer assets. Overall, the data reflects a cautious recovery but with underlying weaknesses in retail and auto sectors.

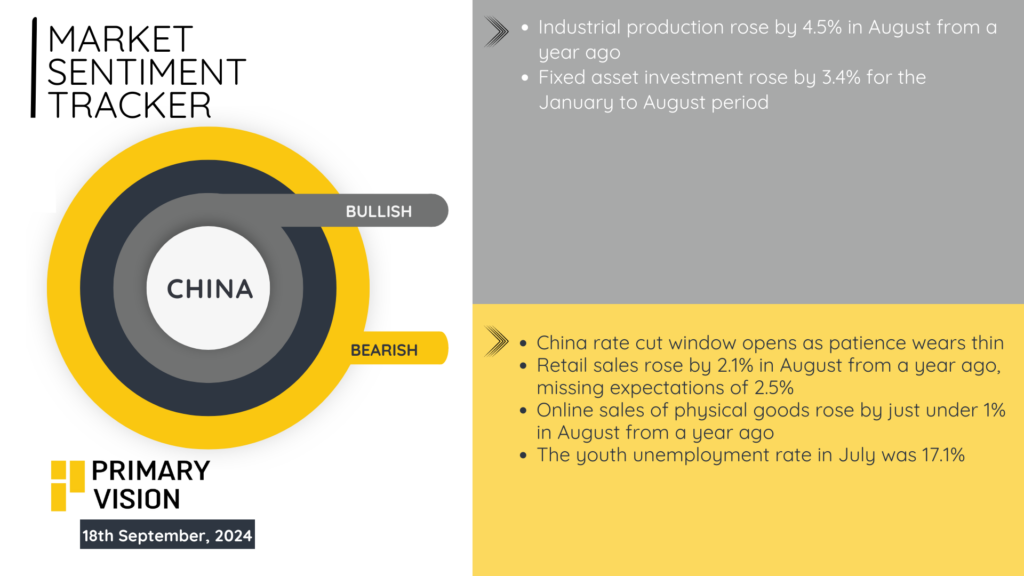

China’s economic data for August shows mixed signals, highlighting both growth and underlying challenges. Industrial production increased by 4.5% year-over-year, and fixed asset investment rose by 3.4% for the January-August period. Retail sales growth was weaker than anticipated, rising only 2.1% compared to expectations of 2.5%, reflecting tepid consumer demand. Online sales of physical goods grew by less than 1%, further underscoring subdued domestic spending. As China’s economic patience wears thin, discussions about rate cuts are intensifying, with many calling for more aggressive fiscal and monetary intervention. The country’s high youth unemployment rate, standing at 17.1% in July, remains a pressing issue, adding to the urgency for economic stimulus. With these factors in mind, China’s ability to sustain momentum without deeper reforms will be a focal point for global markets.

Inflation in the Eurozone dropped to 2.2% in August, marking its lowest level in three years, which brings some relief for consumers but raises concerns for growth. The HCOB Services PMI Business Activity Index saw a slight increase, reaching 51.0 in August from 50.2 in July, signaling modest expansion in the services sector. However, investment remains a key concern, with the EU needing an estimated annual investment increase of €750-€800 billion ($826-$882 billion) to boost its competitiveness. Meanwhile, London’s high-end property market is cooling down due to anticipated tax hits, and Intel’s decision to pause the construction of its chip manufacturing plant in Germany adds more caution to the region’s outlook. With the ECB having cut rates for the first time in five years in June, it remains to be seen how the monetary policy environment will support a sluggish recovery trajectory.

The US, China, and Eurozone economies are facing divergent pressures, but all are exhibiting signs of decelerating growth. In the US, resilient consumer sentiment and household wealth offer some support, but the sharp decline in manufacturing and weaker-than-expected job growth suggest underlying structural challenges, particularly as the Fed contemplates rate cuts. China’s economic trajectory remains fragile—despite a 4.5% rise in industrial production, weak domestic consumption, declining youth employment, and missed retail sales targets indicate persistent demand-side weakness. Moreover, China’s rate cut window, signaling potential policy exhaustion, raises concerns about the effectiveness of future monetary interventions. The Eurozone faces perhaps the sharpest headwinds: German industrial production fell sharply in July, with auto sector output reversing, and broader manufacturing data in contraction territory. Inflation cooling to 2.2% provides some relief, but investment gaps in core economies suggest deeper structural inefficiencies. Overall, stagnation and policy constraints dominate all three regions.