PUMP To Deploy More Electric Fracs: In Q3, PUMP had three electric hydraulic fracturing spreads (FORCE) operating. It plans to add two more in the short term. It also plans to order and deploy more electric assets to solidify its position in the Permian. The company recorded significant impairment charges related to its Tier II diesel-only fracs, validating its decision to transition towards next-generation gas-burning equipment. It plans to keep its active frac spread count unchanged at 14 in Q4. Read more about this in our recent article here.

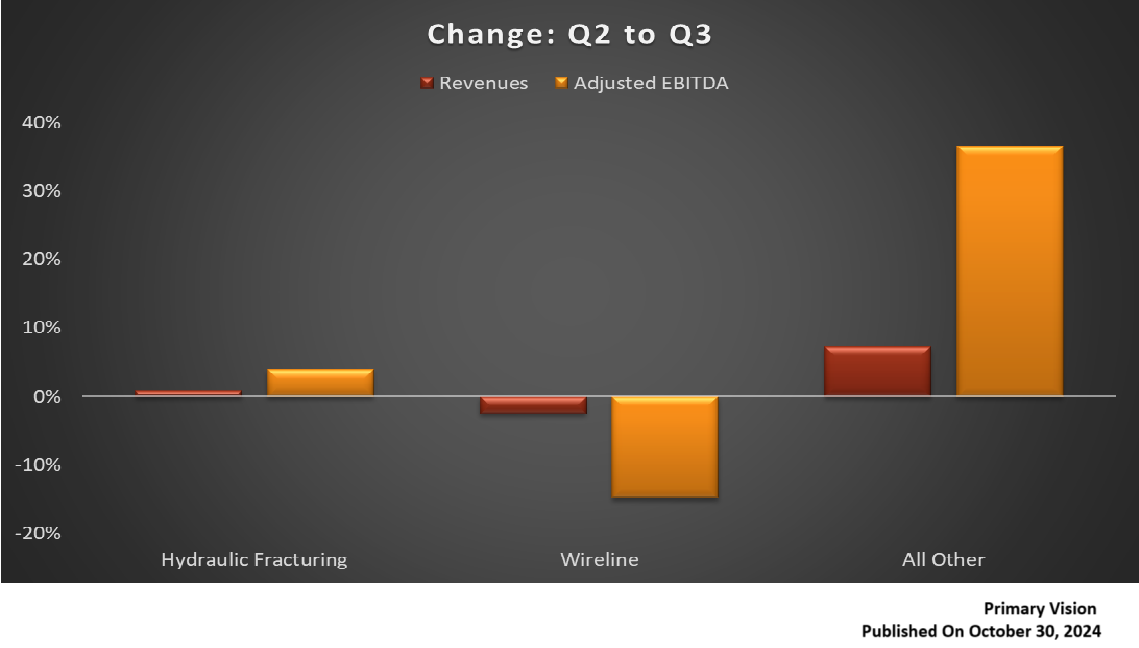

Key Metrics Were Steady In Q3: Quarter-over-quarter, PUMP’s revenues from the Hydraulic Fracturing segment increased marginally, by 1%, in Q3 2024, while its adjusted EBITDA increased by 4%. Its revenues and adjusted EBITDA from the Wireline segment decreased by 3% and 15%, respectively. Improved utilization and cost management pushed revenues and EBITDA higher in Q3. However, unfavorable weather delays largely mitigated these positive factors. During Q3, it recorded impairment charges of ~$189 million related to its Tier II diesel-only hydraulic fracturing equipment.

Cash Flows And Repurchase: PUMP’s cash flow from operations decreased significantly (by 30%) in 9M 2024 compared to 9M 2023. Its free cash flow, however, turned positive as capex fell even more sharply during this period. The company’s debt-to-equity remained unchanged at 0.05x as of September 30, 2024. It repurchased and retired 1.3 million shares in Q3. It reduced its planned FY2024 capex to $150 million-$175 million, down from prior guidance of $175 million-$200 million.

Thanks for reading the PUMP Take Three, designed to give you three critical takeaways from PUMP’s earnings report. Soon, we will present a second update on PUMP earnings, highlighting its current strategy, news, and notes we extracted from our deeper dive.

Premium/Monthly

————————————————————————————————————-