The U.S. presidential election always reverberates across the global economy, but with Donald Trump projected to return to the White House, the implications for the oil markets—both in the U.S. and globally—are particularly profound. Trump’s policy positions, historical track record, and economic philosophy suggest significant shifts in energy production, regulation, trade, and foreign policy. The big question is: what does this mean for the global oil industry in 2025 and beyond?

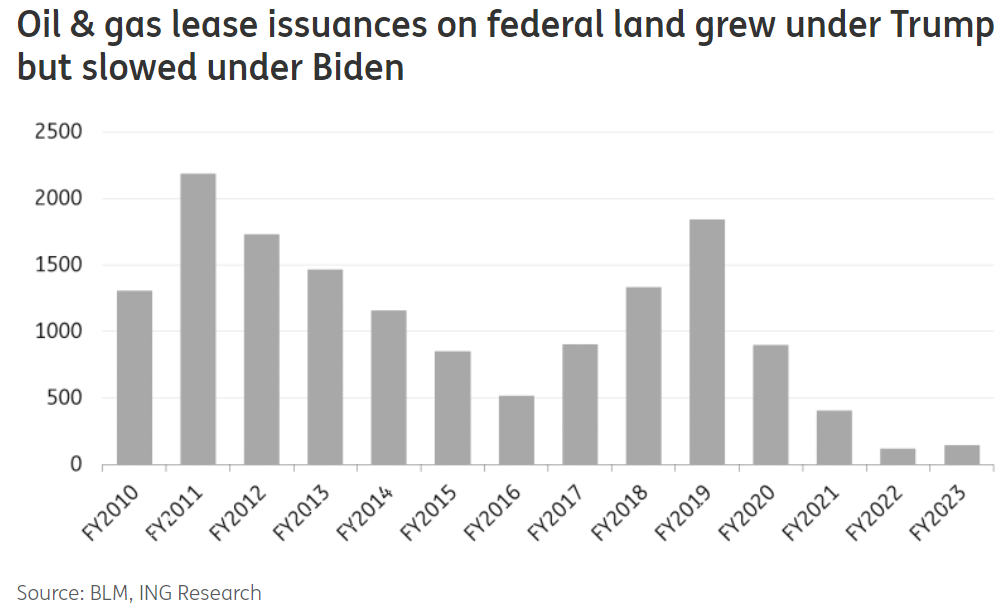

At the heart of Trump’s energy agenda is his infamous “drill, baby, drill” mantra. This echoes his first term, during which the U.S. became the world’s top petroleum producer, with record levels of crude oil output. Trump has pledged to double down on U.S. oil and gas drilling by removing regulatory hurdles and boosting federal leasing, particularly reversing many of the restrictions introduced under President Biden. Under Trump, over 4,000 new oil and gas leases were issued in just three years, compared to about 1,400 under Biden. This likely resurgence in federal land leasing could see onshore production from federal territories—which currently accounts for about 12% of U.S. oil output—increase significantly, though the full effects might take time to materialize.

Marc Ostwald, chief economist at ADM ISI, said that “I suspect the implications for oil and gas need to be differentiated. For oil & gas Trump is likely to push for more domestic production, and roll back regulation to allow drilling in ‘native’ conservation regions. As we know the world is more than well supplied with oil (at the current juncture), and oil demand is proving to be weaker than many (above all OPEC) had projected. To some extent physical oil markets are quite well prepared for this, given very low levels of inventories, but barring an unexpected pick up in demand, the overall implication is negative.”

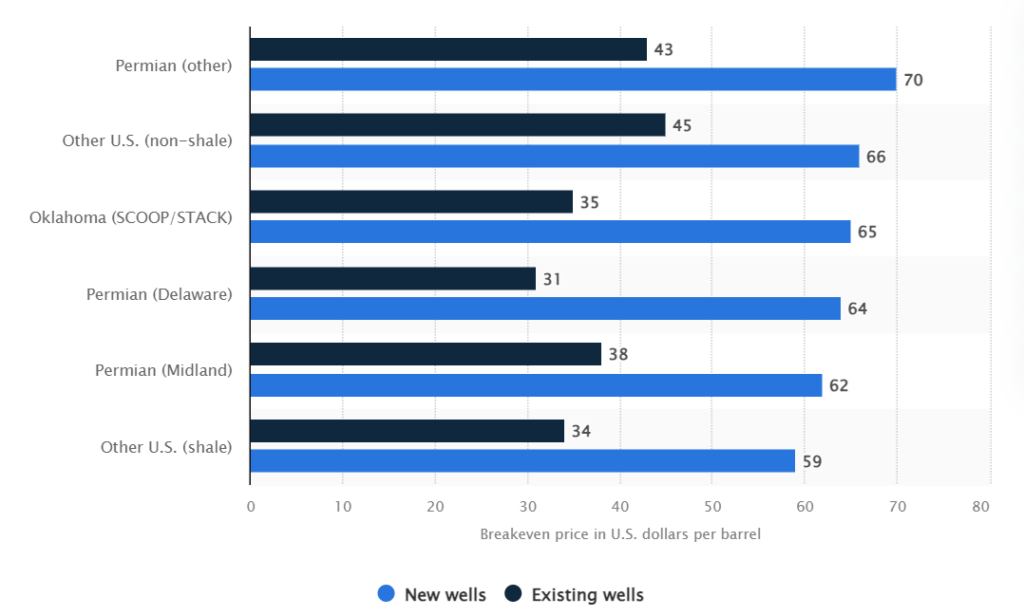

However, the economics of oil drilling remains a key consideration. According to recent Dallas Fed and Kansas Fed Energy Surveys, U.S. oil producers require a breakeven price of around $64 per barrel to drill profitably. With 2025 and 2026 oil futures trading at $70 and $67 per barrel, respectively, there’s enough incentive to encourage production growth, but it’s not a blank check. This cautious pricing outlook suggests that while Trump’s policies may create a favorable regulatory environment, production increases will largely depend on market conditions.

Source: Statista – Average WTI price needed for U.S. oil and gas producers to stay profitable by well status in selected U.S. oilfields as of 2024

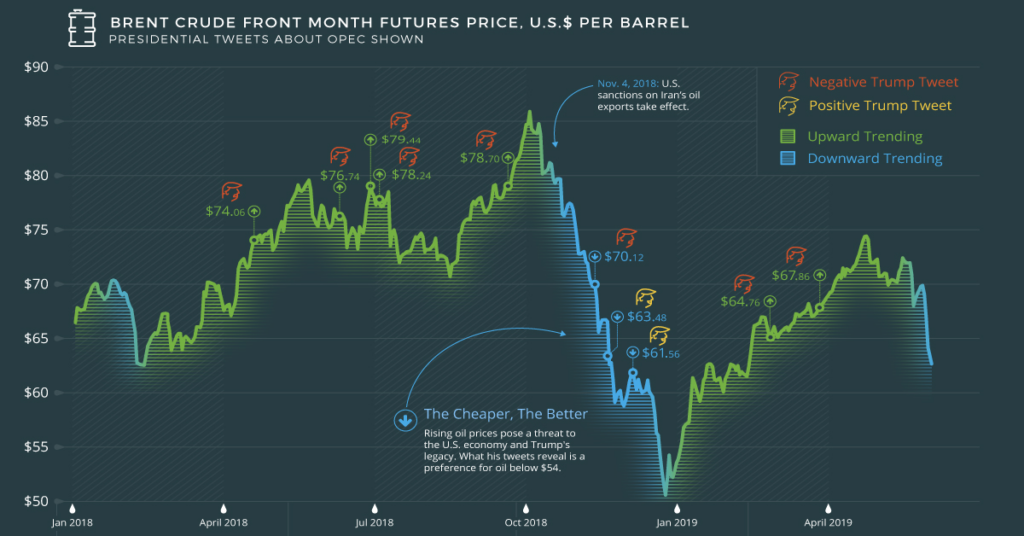

One major wildcard is Trump’s stance on Iran. His first term saw the reimposition of harsh sanctions on Iranian oil exports, slashing global supplies by over a million barrels per day. Under President Biden, these sanctions have been loosely enforced, allowing Iran to significantly ramp up exports. A return to stricter enforcement under Trump could once again curtail Iranian supply, tightening global markets and pushing oil prices higher. Brent crude, currently forecast at $72 per barrel for 2025, could easily climb if a Trump administration reintroduces an aggressive Iran policy. This could, however, create a geopolitical tightrope for Trump, as higher oil prices would clash with his desire to keep domestic energy costs low for American consumers.

Another cornerstone of Trump’s energy vision involves natural gas and LNG (liquefied natural gas). Under Biden, LNG export approvals slowed amid concerns over environmental impacts and energy security. Trump is expected to hit the accelerator, greenlighting projects that could make the U.S. an even more dominant player in the global LNG market. This would bring relief to the Permian Basin, where insufficient pipeline infrastructure has been a persistent bottleneck. By streamlining permitting and approvals, Trump could encourage new investments in both oil and gas pipeline capacity, boosting U.S. production and alleviating regional constraints.

Marc Ostwald, further added, “for NatGas/LNG, the signals from the recent collapse in LNG freight rates suggests that any increase in supply may well be modest, simply because margins are becoming an ever bigger issue given supply is more than plentiful, and if Trump succeeds in his stated intention to reach a negotiated settlement between Russia and Ukraine, then there is the prospect of even more supply. A good deal also depends on how fast demand from India picks up. For the time being increasing Asian LNG demand has offset the lower than expected demand in Europe, the latter in no small part due to record levels of renewable production (obviously vulnerable to greater fluctuations in Winter due to intermittency and higher seasonal demand). I can see a situation where output drops due to margin pressures, and flips the S&D picture, above all if demand picks up, so there is potential for greater volatility, some of this may depend on how rapidly Chinese road freight moves from diesel to LNG fuelled vehicles, which has already had, and will continue to some impact. The picture for refined products is more complex, given decreasing refining capacity in Europe, and per se greater demand for imports. For the time being that is not a problem, given the European economic outlook is at best for marginal growth.”

But as Trump shifts focus to fossil fuels, trade tensions loom as a potential disruptor. His well-documented preference for tariffs and “America First” policies could strain relationships with key trading partners like China, which has historically been a significant buyer of U.S. crude and LNG. During his first term, retaliatory tariffs imposed by China on U.S. LNG led to a complete cessation of exports to the country, forcing producers to find alternative markets. While Europe has since emerged as a major buyer, particularly following the Russia-Ukraine war, a potential trade war could complicate the U.S.’s ability to compete in global energy markets.

Domestically, Trump’s policies could reinvigorate offshore drilling, particularly in the Gulf of Mexico. Offshore production, which accounts for 26% of U.S. oil output, remains a critical part of the energy landscape, but its growth has been hampered by the Biden administration’s focus on onshore shale. A Trump presidency could see increased leasing and investment in offshore projects, particularly for ultra-deep-water drilling. However, the offshore sector faces challenges, including a tight market for advanced drill ships and lingering skepticism about the long-term profitability of offshore ventures compared to onshore shale.

Interestingly, Trump’s return to office could also affect renewable energy development. While his rhetoric has often been dismissive of wind and solar power, there’s a practical side to his policymaking. Analysts suggest that offshore wind projects, especially along the U.S. East Coast, might still see support, albeit with a diminished emphasis compared to Biden’s aggressive climate agenda. This dual focus on both offshore oil and offshore wind could position the U.S. as a versatile energy player, though it would dilute the country’s leadership in renewable technologies compared to regions like Europe and Asia, which are advancing rapidly in green energy investments.

The global implications of Trump’s energy policies are equally significant. A stronger U.S. dollar, buoyed by expectations of higher inflation and interest rates under Trump, could dampen oil demand in emerging markets, where currencies would weaken against the greenback. Historically, a robust dollar has exerted downward pressure on global oil prices by making crude more expensive for non-dollar economies. Additionally, Trump’s potential withdrawal of support for multilateral climate agreements could weaken global momentum on emissions reductions, shifting the balance of energy investments back towards hydrocarbons.

The outlook for global demand is another critical factor. Recent data from the International Energy Agency and OPEC highlight the growing impact of electric vehicles (EVs) on oil consumption, particularly in China and Europe. Even with Trump’s focus on fossil fuels, the accelerating global shift towards EVs and renewables suggests that oil demand growth may moderate over the next decade. This trend could cap the upside for U.S. oil producers, even as Trump pushes for expanded drilling.

At the same time, Trump’s proposed regulatory changes could give American producers an edge over international competitors. His track record suggests an inclination toward reducing barriers to oil and gas development—such as royalty adjustments, expedited permitting, and a more lenient stance on methane fees. These measures could bolster the cost-efficiency of U.S. operations and incentivize greater investment in domestic production. However, such deregulatory moves aren’t without their challenges. Historical precedents, like the controversy surrounding the Keystone XL pipeline, illustrate how regulatory shortcuts can invite lengthy legal disputes. Striking the right balance between encouraging development and adhering to environmental and procedural standards will be critical if these policies are to deliver sustainable benefits to the industry.

Gaurav Sharma, Energy Market Analyst and commentator, who keenly follows global energy market shared with me that “in the near-term, especially 2025, you will see an uptick in US crude production party because of Trump’s pro-oil credentials and partly down to OPEC+ decisions that have caused various price upticks at several points this year allowing American producers to hedge and protect their revenue on a 12-18 months out basis. for the medium-term, expect a rollback of Biden’s curbs. e.g. on exploration on Federal lands by a Trump White House. The industry will welcome a Trump presidency but that does not necessarily change a challenging price environment, especially for demand for US light sweet crude globally.”

A Trump presidency would usher in further conflicting factors for the oil markets. On one hand, his policies could boost U.S. production, strengthen energy exports, and reduce regulatory burdens. On the other, trade tensions, geopolitical risks, and global shifts towards cleaner energy could limit the effectiveness of his fossil fuel-focused agenda. The key question is whether Trump’s approach can navigate these competing dynamics without exacerbating volatility or alienating key trading partners. For the global oil markets, the next four years under Trump could be a delicate balancing act. His policies will likely provide short-term gains for U.S. producers but could risk long-term sustainability if they fail to address the broader trends reshaping the energy landscape. As we move into 2025, the interplay between Trump’s vision, market realities, and global energy transitions will define the trajectory of the oil industry for years to come.