In a recent interview, ExxonMobil CEO Darren Woods expressed skepticism about President-elect Donald Trump’s ability to significantly boost U.S. energy production in the near term. Woods highlighted that U.S. crude oil production had already reached record levels, averaging 13.4 million barrels per day (bpd) as of August 2024. There are multiple factors that might hinder further boost in production. The global demand is the most important element as the world is expected to be oversupplied with oil. Secondly, pipeline capacity is another technical reality that cannot be ignored. Lastly, the refineries need an overhaul too as most were built to refine heavier grades as compared to the lighter grade that has witnessed a record increase in production.

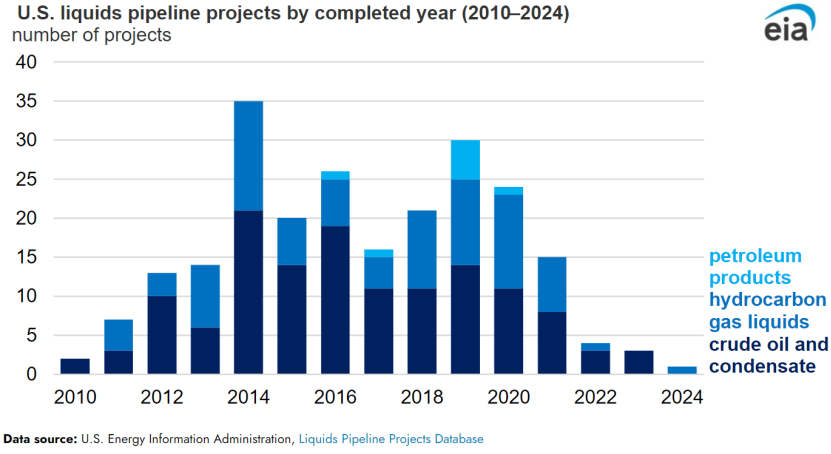

A critical factor limiting immediate increases in oil production is the current pipeline infrastructure. Even with favorable pricing and potential subsidies, the existing pipeline network is operating near full capacity, restricting the transportation of additional crude from production sites to refineries or export terminals. While new pipeline projects are under consideration, they require extensive time-frames for permitting, environmental assessments, and construction, delaying any short-term impact.

Source: Energy Information Administration

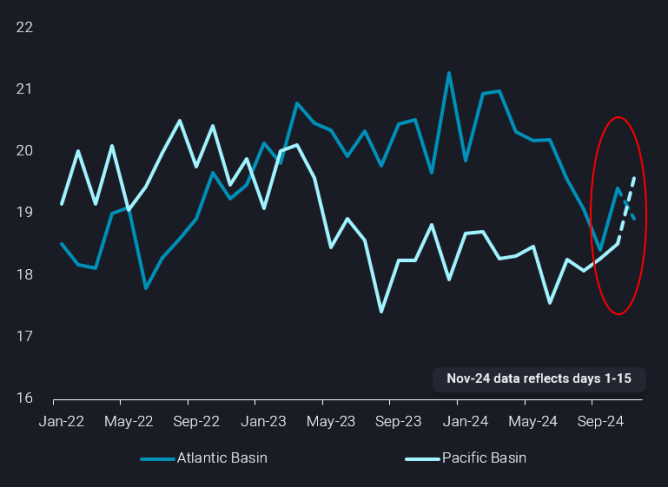

Also, U.S. refineries are primarily configured to process heavier crude grades, whereas the recent surge in production has been predominantly lighter crude. This mismatch necessitates exporting the excess light crude, but global markets are currently oversupplied. European demand remains subdued, and Asian markets are increasingly sourcing cheaper alternatives, especially as Saudi Arabia is expected to reduce its Official Selling Prices.

Source: Vortexa – Global crude/condensate exports split by loading basin, excluding Iran, Venezuela (mbd)

While immediate expansion of production faces significant hurdles, the incoming administration could implement strategic measures to influence the energy sector’s trajectory:

- Accelerating the approval process for new pipeline projects could alleviate future bottlenecks. For example, revisiting the Keystone XL pipeline project, which was canceled in 2021, is reportedly on Trump’s agenda. However, this initiative faces challenges, including the need to renegotiate with stakeholders and address environmental concerns.

- Opening new areas, such as the Gulf of Mexico, for exploration could increase future reserves. However, this approach faces legal, regulatory, and environmental hurdles that would delay any immediate impact. Trump can also expedite the time to get a drilling permit. During Biden administration, the average time to complete a permit was 258 days as compared to 172 days during Trump.

- Encouraging Liquefied Natural Gas (LNG) projects and securing long-term offtake agreements with foreign buyers could bolster demand for U.S. energy exports. Nonetheless, these projects also require years to come online, offering limited short-term relief.

Trump is preparing a wide range of measures that will supposedly unlock new potential for the U.S. shale industry. This includes, but is not limited to, increased drilling off the coast and on federal lands. I believe the biggest hindrance to increased oil and gas production will come from finding the right pricing.

The global economy is still not looking strong enough to support an increase in demand. There are fears of an oversupply already with World Bank’s latest Commodity Outlook striking a bearish tone for 2025 and it expects an overhang of 1.2 mbpd of oil supply versus demand – which has happened only twice before: 1998 and during pandemic.

As such, we will have to wait and watch to track the future trajectory of U.S. oil production. Primary Vision has also done a short report on the U.S. shale outlook by investigating cashflows and future plans of major oilfield services. You can read it here. The story of U.S. shale is closely related to the global economy and vice-versa. There are many moving pieces. We haven’t talked about OPEC+ future plans yet – which forms another key strand of the global oil markets. Here is a free article on this topic that discusses the future of these production cuts in detail.

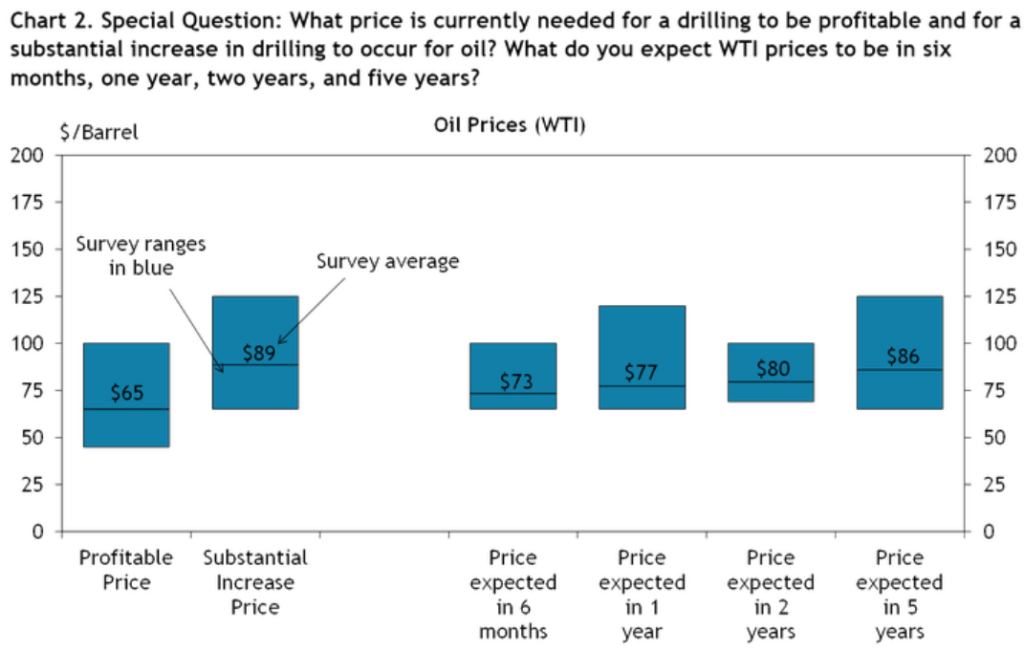

The current global oversupply and limited demand reduce the incentive to increase production in the near term. Adding more supply could further depress prices, adversely affecting producers and the broader industry. Look at Trump’s Treasury Secretary pick, Scott Bessent, who wants 3-3-3 plan – 3% increase in GDP, cutting budget deficit to 3%, and increasing oil production by 3%. It can be seen that the oil companies are now focused on consolidated cash flows over excessive production. Also, the average price for shale producers to be profitable is $65 and $89 to increase drilling. The prices right now are nowhere to the later levels.

While policies aimed at infrastructure development and regulatory easing are beneficial for long-term growth, their immediate impacts are constrained by existing market and logistical realities. While the incoming administration may pursue policies to support the energy sector, the combination of infrastructure limitations, market dynamics, and regulatory processes suggests that any significant increase in U.S. oil production will be a gradual process, unfolding over the coming years.