Key Projects In Q3

We have already discussed TechnipFMC’s (FTI) Q3 2024 financial performance in our recent article. This article will dive deeper into the industry and its current outlook. In Q3, FTI had an inbound order of $2.46 billion, which was 20% lower than a quarter earlier. In Subsea, FTI received Flexible Pipe and Subsea Production Systems awards from Petrobras. In BP’s Kaskida project in the Gulf of Mexico, it received a second iEPCI to utilize a 20K production system. Such 20K systems represent an important opportunity in the high-pressure-high-temperature reservoirs.

Outlook And Forecast

FTI’s backlog was $14.7 billion after Q3. In Subsea, it sees a diversified mix of opportunities utilizing its Subsea 2.0 and iEPCI technologies by the end of 2025. It is confident in achieving $30 billion in orders over the three-year period ending 2025, which can drive backlog in the medium term. Beyond 2025, the company’s strong FEED (FrontEnd Engineering and Design) pipeline for subsea developments can translate into strong FID in the latter half of the decade. Such a robust project pipeline in 2025, 2026, and beyond has increased its mid-term revenue visibility.

In Q4, however, FTI expects some headwinds. Its Subsea revenues can decline by “low-single-digits” sequentially. For FY2025, it increased its revenue and adjusted EBITDA margin guidance. Now, it expects to generate Subsea revenues of $8.3 billion-$8.7 billion and an adjusted EBITDA margin of 16.5% to 17%.

Now, it expects to generate Subsea revenues of $7.6 billion-$7.8 billion and an adjusted EBITDA margin of 18.5% to 20% in FY2025. The new adjusted Subsea EBITDA guidance (at the mid-point) represents more than 25% expansion. Continued execution and the management’s confidence in the market backdrop resulted in the upward forecast revision for FY2025. The company also increased its FY2024 adjusted EBITDA expectations to $1.37 billion.

Key Q3 Metrics

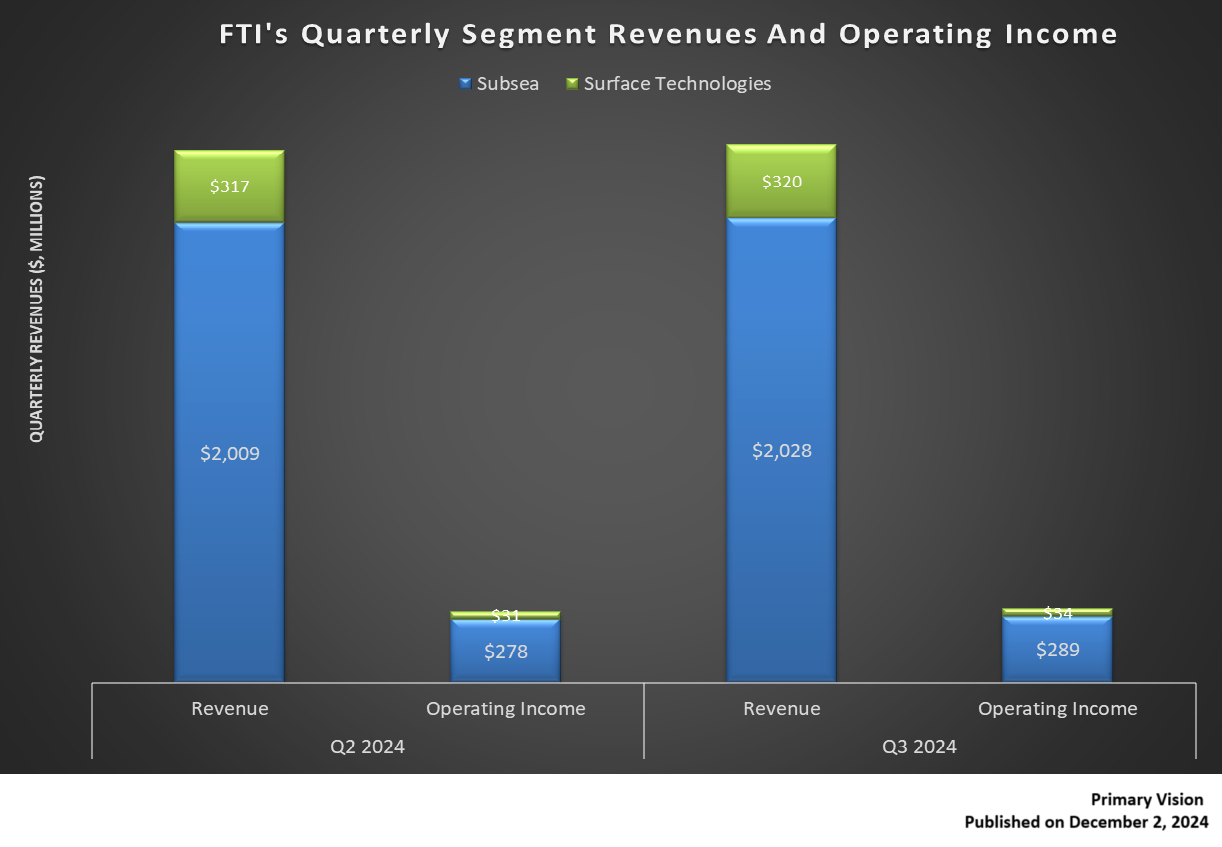

Quarter-over-quarter, revenues in the company’s Subsea operating segment rose slightly in Q3. The top line in the Surface Technologies segment increased by 1.3%. Operating income growth in the Subsea segment decelerated to 4% in Q3. Operating income in the Surface Technologies segment increased by 10%.

FTI’s cash flow from operations strengthened enormously in 9M 2024 from a negative cash flow a year ago. As a result, its FCF also turned significantly positive. During Q3, it increased share repurchase authorization by $1 billion. Year-to-date, it has distributed $395 million to shareholders. It now has nearly $1.2 billion of remaining authorization following the increase in share repurchase authorization.

Relative Valuation

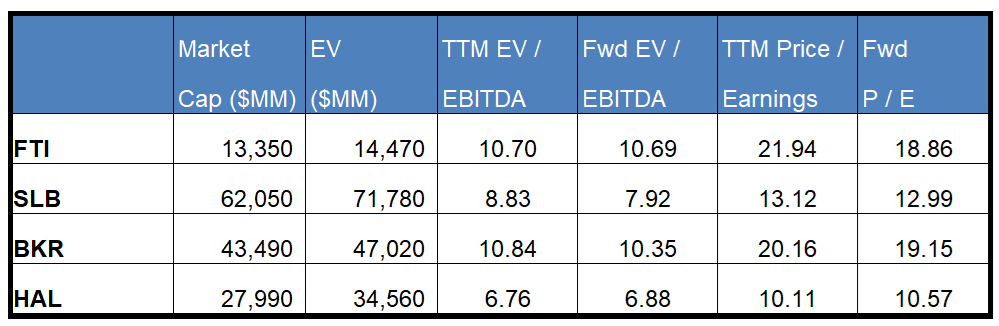

FTI is currently trading at an EV-to-adjusted EBITDA multiple of 10.7x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is nearly unchanged. The current multiple is higher than its five-year average EV/EBITDA multiple of 8.3x.

FTI’s forward EV-to-EBITDA multiple versus the adjusted current EV/EBITDA is nearly unchanged compared to fall in the multiple for its peers because the company’s EBITDA is expected to remain unchanged versus a rise in EBITDA for its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is higher than its peers’ (SLB, BKR, and HAL) average. So, the stock is relatively overvalued compared to its peers.

Final Commentary

In Q3, FTI’s subsea order book shrank, reflecting lower sales of wellhead equipment in North America. However, the company has a diversified operational base as it increasingly promotes Subsea 2.0 equipment and iEPCI projects. It expects a strong FEED pipeline for subsea developments to translate into strong FID. Such a robust project pipeline lends visibility beyond 2025 and 2026. So, the company revised its FY2025 forecast due to % in FY2025. The new adjusted Subsea EBITDA guidance (at the mid-point) represents of more than 25% expansion. The continued execution and the management’s confidence in the market backdrop will propel it upward.

A rise in EBITDA translated into higher cash flows in 9M 2024. This gave FTI’s management the confidence to increase share repurchase authorization by $1 billion. The stock is relatively overvalued compared to its peers at this level.

Premium/Monthly

————————————————————————————————————-