International Business Strategies

We have already discussed Halliburton’s (HAL) Q3 2024 financial performance in our recent article. The management expects revenue from its international business to grow by “low- to mid-single digits” compared to a 4% year-over-year growth in Q3. Growth can accelerate due to the robust performance in cementing, completion tools, and drilling fluids. For Halliburton, the iCruise and iStar directional drilling and logging tools, LOGIX automation and remote operation platform, and ultra-deep drilling tools contributed to its superior performance internationally. Its Sperry Drilling business also made noteworthy contributions. Currently, offshore operations account for 50% of its revenue outside of North America onshore.

The company’s international artificial lift business can also outgrow the market on the back of its technology portfolio. During Q3, it introduced TrueSync hybrid motor. While it was initially deployed in North America, it expects strong international demand from Latin America and the Middle East as drilling scales in these regions. Its views on internationally unconventional energy market growth are particularly bullish. During Q3, it received a multiyear unconventional drilling services contract in the Middle East. It also started up an unconventional hydraulic fracturing spread in that region. In 2025, the management expects operations in the unconventional shales, artificial lift, and intervention activities to grow fast internationally.

Frac Outlook

In the Completion business, 90% of its fracturing spreads are committed for work in 2025. Its completion technologies include the Zeus platform, electric pumping units, Octiv Auto Frac, and Sensori subsurface measurement. One of its latest technology solutions is Octiv, a key component of the ZEUS platform. Octiv delivers an automation solution called AutoFrac in large multi-well pads. It autonomises frac job from the ramp up at the start to the ramp down at the end.

During Q3, it signed contracts for two new e-frac spreads and also secured extensions on several existing fleets. E-spreads and its integration with the Zeus platform can exceed 50% of its active spreads in 2025. It has deployed Auto Frac on 20% of its e-fleets and expects to expand to 50% in the next two months. The Zeus’ platform, Sensori fracture diagnostics, and an automated real-time environment can allow for higher levels of efficiency and improved recovery.

In another impressive performance, HAL’s drilling services business in North America grew by 20% year-over-year despite a 5% rig count fall. The management expects the growth to continue in 2025. Its iCruise rotary steerable tool and LOGIX drilling automation platform enabled growth in its commercial models – rental, sales, and full service.

Segment Forecast

In Q4, the management expects the C&P division revenue to decline by 1%-3%, while operating margins can decrease by 75-125 basis points. The Drilling and Evaluation division expects revenue to increase by 0%-2% and margins by 0-50 basis points in Q4.

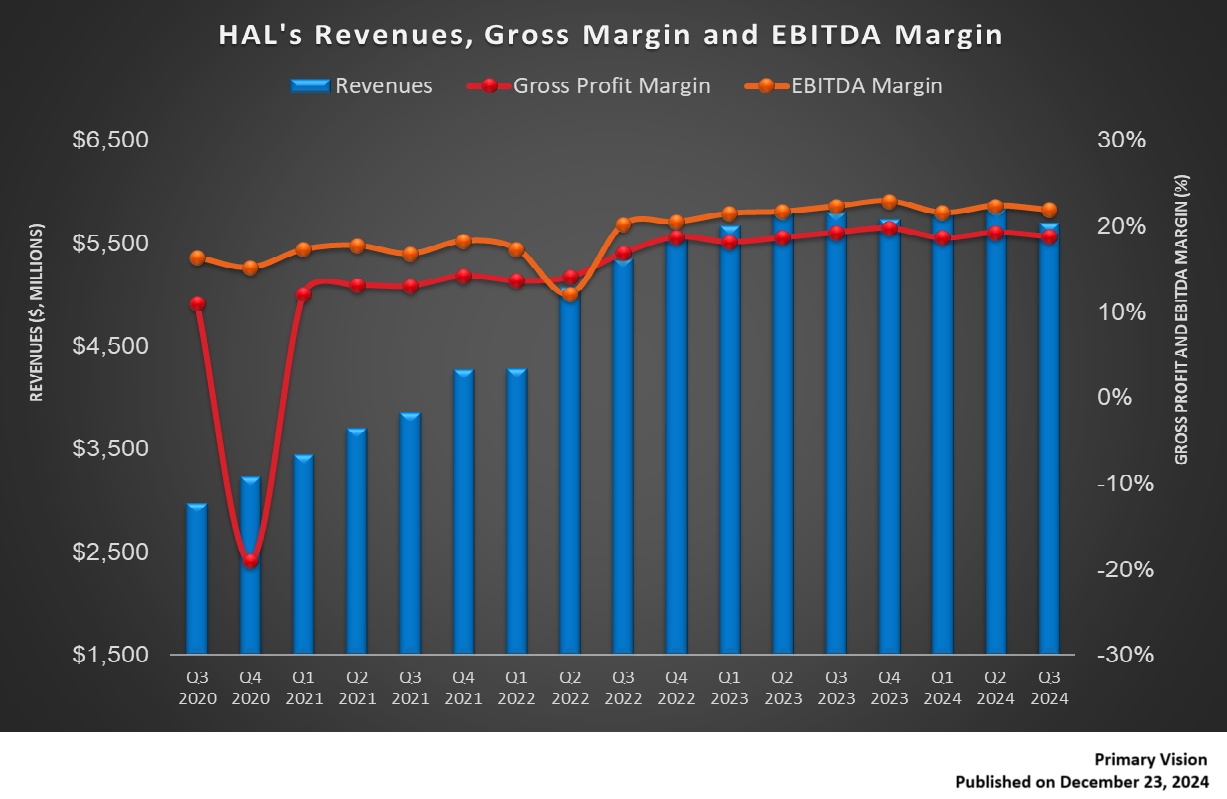

Key Q3 Metrics

Quarter-over-quarter, the revenues in the company’s Completion and Production operating segment decreased by 3% in Q3. The top line in the Drilling and Evaluation segment decreased by 1.4%.

HAL’s cash flow from operations strengthened (17% up) in 9M2024 compared to a year ago. In FY2024, it expects FCF to increase by ~10% compared to FY2023. Debt-to-equity (0.74x) also showed improvement from FY2023. During Q3, it repurchased shares worth $200 million to improve shareholder returns.

Relative Valuation

Halliburton is currently trading at an EV/EBITDA multiple of 5.8x. Based on sell-side analysts’ EBITDA estimates, the forward EV/EBITDA multiple is slightly higher. The current multiple is lower than its five-year average EV/EBITDA multiple of 11.1x.

HAL’s forward EV/EBITDA multiple increase versus the adjusted EV/EBITDA is in contrast to a decline in the multiple for its peers because the company’s EBITDA is expected to fall versus a rise in EBITDA for its peers in the next four quarters. This typically results in a lower EV/EBITDA multiple than peers. The stock’s EV/EBITDA multiple is lower than its peers’ (SLB, BKR, and FTI) average of 9.2x. So, the stock is reasonably valued versus its peers.

Final Commentary

HAL has recently introduced a slew of products and technologies, including the iCruise and iStar directional drilling and logging tools, LOGIX automation and remote operation platform, and ultra-deep drilling tools. Its international business should benefit from higher demand for cementing, completion tools, and drilling fluids. As drilling scales in Latin America and the Middle East in unconventional wells, the company frac spread deployment, artificial lift, and intervention activities can accelerate.

During Q3, it signed contracts for two new e-frac spreads as the Zeus platform strengthened. The share of e-spreads in HAL’s portfolio is set to increase in 2025. Its FCF can increase by ~10% in FY2024, allowing for higher shareholder returns through share repurchase. The stock is reasonably valued versus its peers at this level.

Premium/Monthly

————————————————————————————————————-